An Analysis of Momentum Behaviour in a Long-Term

A recent paper takes a look on a long-term behaviour of momentum portfolios. Related to all equity momentum strategies, mainly to:

#14 – Momentum Effect in Stocks

Authors: Ali, Daniel, Hirshleifer

Title: One Brief Shining Moment(um): Past Momentum Performance and Momentum Reversals

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2956493

Abstract:

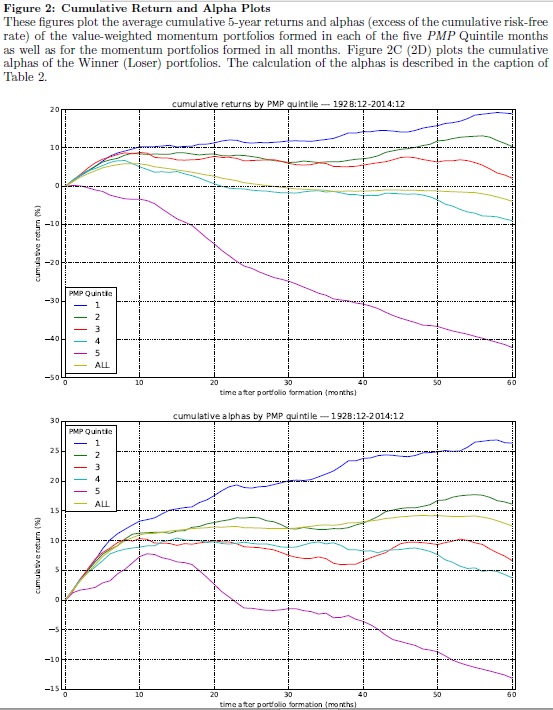

Motivated by behavioral theories, we test whether recent past performance of the momentum strategy (Past Momentum Performance–PMP) negatively predicts the performance of stale momentum portfolios. Following periods of top-quintile PMP, momentum portfolios exhibit strong reversals 2-5 years after formation, whereas, following periods of bottom-quintile PMP, stale momentum portfolios earn positive returns. The difference in cumulative five-year Fama-French alphas for momentum portfolios formed in high- and low-PMP months is 40%. A value-weighted trading strategy based on this effect generates an alpha of 0.40% per month (t = 3.74). These patterns are confirmed in international data. These findings present a puzzle for existing theories of momentum.

Notable quotations from the academic research paper:

"A set of studies propose behavioral hypotheses to explain the momentum anomaly. An implication of some of these models is that the momentum phenomenon is a result of delayed overreaction to certain information shocks. This implies that a suffi�ciently `stale' momentum portfolio, where `stale' refers to a momentum portfolio formed at a lag of twelve months or more, will on average earn negative abnormal returns.

However, to our knowledge, no study has yet examined the conditional variation in the performance of stale momentum strategies, i.e., the performance of momentum portfolios in years 2-5 post-formation. One interesting possibility, motivated by the idea that investors chase past style performance, is that strong recent past performance of the momentum style will cause investors to overvalue new momentum portfolios, resulting in poor subsequent long-run performance of these portfolios. In this paper, we explore this issue by testing whether long horizon performance of momentum portfolios is negatively related to the performance of the momentum strategy in the recent past.

In particular, we examine the relation of stale momentum returns to a measure of the recent performance of the momentum strategy, which we call Past Momentum Performance or PMP. PMP is simply the return of a standard (12,2) momentum strategy over the preceding 2 years (24 months). Our basic fi�nding is that momentum portfolios formed in high PMP months (months when PMP is in the top 20% of all months in our sample) generate strongly negative returns and alphas 2-5 years after formation. Strikingly, momentum portfolios formed in low PMP months continue to (weakly) outperform in post-formation years 2-5. Thus, the momentum reversal documented by Jegadeesh and Titman (2001) is strongly state dependent.

We explore a set of behavioral hypotheses for the strong dependence of stale momentum performance on PMP. One of our hypotheses is based upon style chasing.

A basic hypothesis is that the performance of the momentum style will tend to continue in the short run, so that after the momentum strategy has done well, it tends to do well again. The style chasing approach suggests that following high returns on the momentum style, owing to return extrapolation, naive investors switch into this style, meaning that they buy winners and sell losers heavily. This trading pressure reinforces the strong performance of the momentum strategy, and will temporarily cause better-than-usual momentum performance after the conditioning date if such return chasers arrive gradually.

This e�ffect is driven by overreaction in the components of the momentum portfolio. In consequence, the returns on the momentum portfolio will eventually reverse. So after high PMP, there are on average negative returns to a stale momentum strategy of buying �firms that were winners at least a year ago and selling �firms that were losers at least a year ago.

In contrast, after low PMP, investors switch out of the momentum style. Heavy selling of winners and buying of losers induces underreaction in winner and loser returns. So after low PMP, this hypothesis implies eventual positive returns to a stale momentum strategy. Putting these two cases together, we expect reversal of momentum to be stronger as PMP increases.

Motivated by these ideas, we examine the relationship between PMP and the performance of stale momentum portfolios and fi�nd a number of novel e�ffects. We fi�rst show that over the full CRSP sample, there is on average very little tendency of momentum to reverse after controlling for the value eff�ect. This fi�nding is in contrast to that of Jegadeesh and Titman (2001) who �find, in a shorter sample, that equal-weighted momentum portfolios exhibit strong reversals even after controlling for the value e�ffect.

Then, turning to our main result, we fi�nd a strong relationship between PMP and long-run reversal of momentum – reversal is greater after high PMP. Speci�fically, we rank the months in our sample into quintiles based on PMP and examine the performance of momentum portfolios formed in each category of month (i.e., for months in each PMP quintile) during the �five years after formation. Stale momentum performance declines strongly and monotonically with PMP. In Quintile 1, instead of reversal, momentum portfolios exhibit weak continuation in post-formation years 2-5. In sharp contrast, momentum portfolios formed in Quintile 5 months lose 42% of their value over the next fi�ve years. We call this strong reversal of momentum after high PMP the PMP eff�ect.

"

"

Are you looking for more strategies to read about? Check http://quantpedia.com/Screener

Do you want to see performance of trading systems we described? Check http://quantpedia.com/Chart/Performance

Do you want to know more about us? Check http://quantpedia.com/Home/About

Share onLinkedInTwitterFacebookRefer to a friend