A Turn of the Month Strategy in Asset Allocation

A new research paper related mainly to:

#41 – Turn of the Month in Equity Indexes

Authors: McGroarty, Platanakis, Sakkas, Urquhart

Title: A Seasonality Factor in Asset Allocation

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3266285

Abstract:

Motivated by the seasonality found in equity returns, we create a Turn-of-the-Month (ToM) allocation strategy in the U.S. equity market and investigate its value in asset allocation. By using a wide variety of portfolio construction techniques in an attempt to address the impact of estimation risk in the input parameters, we show significant out-of-sample benefits from investing in the ToM factor along with a traditional stock-bond portfolio. The out-of-sample benefits remain significant after taking into account transaction costs and by using different rolling estimation windows indicating that a market timing strategy based on the ToM offers substantial benefits to investors when determining the allocation of assets.

Notable quotations from the academic research paper:

"Seasonality is a well-known characteristic of financial markets with much empirical literature noting various types of seasonality in stock returns. Simple seasonality-driven investment strategies have attracted significant interest from academics and investors over the last forty years.

Amongst the calendar effects, the turn-of-the-month (ToM hereafter) has been acknowledged as one of the strongest and persistent seasonality found in stock returns. The ToM effect is the tendency of the stock market returns to display particularly high returns on the last trading day of the month and the first three trading days of the next month.

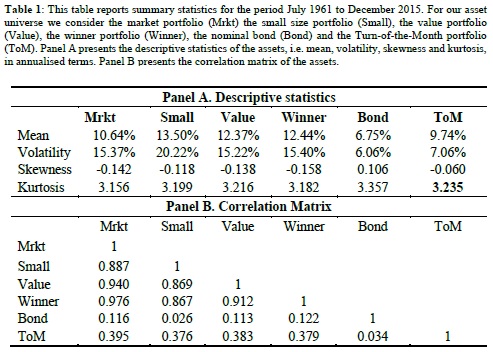

This study contributes to the literature on calendar anomalies in several dimensions. We examine the out-of-sample portfolio benefits resulting from adding the ToM portfolio to (i) a traditional equity-bond mix, (ii) a market portfolio, (iii) a portfolio which consists of the market portfolio, the small size portfolio and the value portfolio, and (iv) a portfolio, which consists of the market, the small size, the value portfolio and the winner portfolio.

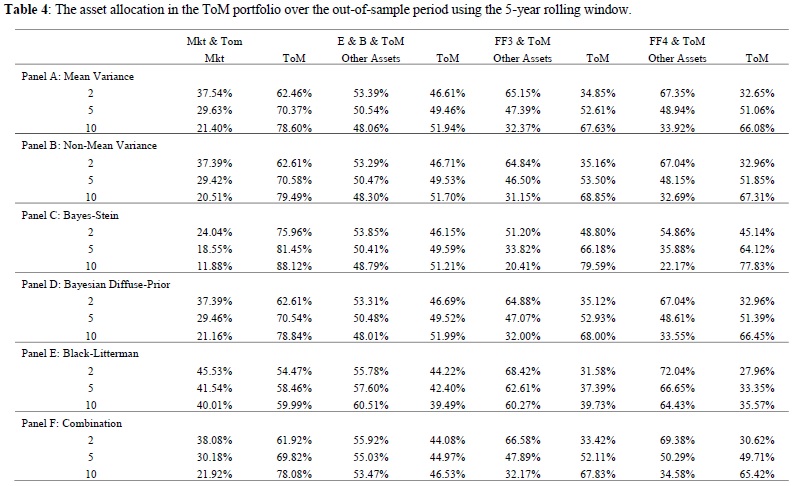

We employ a wide variety of sophisticated and popular asset allocation techniques to provide robustness to our results. Specifically, we employ the mean-variance (Markowitz) portfolio optimization, portfolio optimization with higher moments, Bayes-Stein shrinkage, Bayesian diffuse-prior portfolio, Black-Litterman and another portfolio construction method that combines individual portfolio techniques, to ensure that our results are not just a peculiar artefact on one particular asset allocation technique. Finally, we assess the ToM for low, medium and high-risk averse investors, as its effectiveness in the portfolio might depend on the investor’s level of risk aversion.

Our empirical evidence suggests that the ToM portfolio adds value when included in different portfolios. Our results hold for different levels of risk aversion, portfolio techniques and estimation windows. Finally, our results are not eliminated by the including realistic transaction cost estimates, indicating that the creation and implementation of a ToM factor should be of great interest and potential value to investors.

"

"

Are you looking for more strategies to read about? Check http://quantpedia.com/Screener

Do you want to see an overview of our database of trading strategies? Check https://quantpedia.com/Chart

Do you want to know how we are searching new strategies? Check https://quantpedia.com/Home/How

Do you want to know more about us? Check http://quantpedia.com/Home/About

Follow us on:

Facebook: https://www.facebook.com/quantpedia/

Twitter: https://twitter.com/quantpedia

Share onLinkedInTwitterFacebookRefer to a friend