Does High Market Liquidity Cause Vanishing Equity Anomaly Returns ?

Short answer? – Probably no … A new academic research paper �concludes that "the recent worldwide regime of increased liquidity, apart from some exceptions, is not accompanied by robustly significant decreases of anomalous returns in the US and the majority of other markets." Research paper related mainly to:

#14 – Momentum Effect in Stocks

#25 – Size Premium

#26 – Value (Book-to-Market) Anomaly

#77 – Beta Factor in Stocks

Authors: Auer, Rottmann

Title: Have Capital Market Anomalies Worldwide Attenuated in the Recent Era of High Liquidity and Trading Activity?

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3275377

Abstract:

We revisit and extend the study by Chordia et al. (2014) which documents that, in recent years, increased liquidity has significantly decreased exploitable returns of capital market anomalies in the US. Using a novel international dataset of arbitrage portfolio returns for four well-known anomalies (size, value, momentum and beta) in 21 developed stock markets and more advanced statistical methodology (quantile regressions, Markov regime-switching models, panel estimation procedures), we arrive at two important findings. First, the US evidence in the above study is not fully robust. Second, while markets worldwide are characterised by positive trends in liquidity, there is no persuasive time-series and cross-sectional evidence for a negative link between anomalies in market returns and liquidity. Thus, this proxy of arbitrage activity does not appear to be a key factor in explaining the dynamics of anomalous returns.

Notable quotations from the academic research paper:

"Recent years have been characterised by unprecedented changes in trading technology and transaction costs. A lot of authors document signi�ficant advances in algorithmic trading and increased utilisation of online brokerage accounts and observe drastic declines in, for example, standardised aggregate costs of trading for NYSE, NASDAQ and AMEX stocks of on average 97% from 146 basis points in 1980 to 11 basis points in 2006. Standard measures of liquidity have increased substantially because this new market environment of reduced trading frictions stimulates trading activity. For example, they present evidence that:

(i) the average monthly share turnover on the NYSE rose from about 5% in 1993 to about 26% in 2008 (and the average daily number of transactions increased about ninetyfold in the same period), whereas it was almost unchanged in the decades before,

(ii) mainly institutional trading volume accounts for this increase and

(iii) increased volume is associated with higher market quality (i.e., closer conformity to random walk behaviour).

Motivated by these observations, several studies have analysed whether increased liquidity has triggered greater anomaly-based arbitrage and thus attenuated capital market anomalies. In their conclusion, Chordia et al. (2014, p. 57) argue that "return predictability would diminish to a greater extent in countries that have experienced greater enhancements in trading technologies and larger increases in trading activity and liquidity" and that this "hypothesis awaits rigorous testing in an international context". This is where we step into the picture. We extend the hedge portfolio evidence of Chordia et al. (2014) to an international setting.

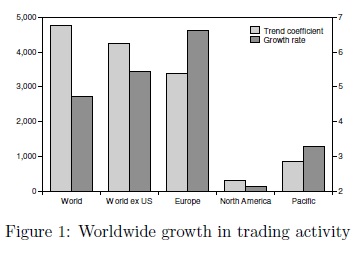

Figure 1, reporting trends and growth rates for the number of traded shares in di�fferent regions of the world, shows positive tendencies worldwide and that there are indeed di�fferences in the timely development of trading activity. For example, trading activity appears to have increased more significantly in European markets than in the US. Thus, we would not only expect to �find evidence on vanishing anomaly returns in other markets as well but also that the magnitudes of the changes in anomaly returns are quite di�fferent across individual markets.

Using a novel dataset containing arbitrage portfolio returns for the four well-known anomalies of size, value, momentum and beta for a wide range of developed stock markets, we start our analysis by testing whether these anomalies still exist and whether the corresponding arbitrage portfolio returns exhibit trending behaviour. We also investigate trends in market liquidity in a more detailed fashion than in our previous illustration.

Using a novel dataset covering three decades, we �find that the recent worldwide regime of increased liquidity, apart from some exceptions, is not accompanied by robustly signifi�cant decreases of anomalous returns in the US and the majority of other markets. We cannot establish a persistent negative link between arbitrage portfolio returns and share turnover in both the time-series and the cross-sectional dimension. These results suggest that aggregate liquidity may be a measure too coarse for our purposes or that liquidity in general may not be the key driver of the dynamics of international anomaly portfolios."

Are you looking for more strategies to read about? Check http://quantpedia.com/Screener

Do you want to see an overview of our database of trading strategies? Check https://quantpedia.com/Chart

Do you want to know how we are searching new strategies? Check https://quantpedia.com/Home/How

Do you want to know more about us? Check http://quantpedia.com/Home/About

Follow us on:

Facebook: https://www.facebook.com/quantpedia/

Twitter: https://twitter.com/quantpedia

Share onLinkedInTwitterFacebookRefer to a friend