Price Overreactions in the Cryptocurrency Market

Once again, is cryptocurrency market efficient? Or can we find simple trading strategies based on price overreactions? :

Authors: Caporale, Plastun

Title: Price Overreactions in the Cryptocurrency Market

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3088472

Abstract:

This paper examines price overreactions in the case of the following cryptocurrencies: BitCoin, LiteCoin, Ripple and Dash. A number of parametric (t-test, ANOVA, regression analysis with dummy variables) and non-parametric (Mann–Whitney U test) tests confirm the presence of price patterns after overreactions: the next-day price changes in both directions are bigger than after “normal” days. A trading robot approach is then used to establish whether these statistical anomalies can be exploited to generate profits. The results suggest that a strategy based on counter-movements after overreactions is not profitable, whilst one based on inertia appears to be profitable but produces outcomes not statistically different from the random ones. Therefore the overreactions detected in the cryptocurrency market do not give rise to exploitable profit opportunities (possibly because of transaction costs) and cannot be seen as evidence against the Efficient Market Hypothesis (EMH).

Notable quotations from the academic research paper:

“Despite a significant number of studies on market overreactions none of them has focused on the cryptocurrency market, which is the most volatile among financial markets: the average daily price amplitude in this market is more than 10 times higher than in FOREX, 7 times higher than in stock market and more than 5 times higher than in the commodity markets. This feature (combined with the fact that it is a very young market) makes it particularly interesting to examine for possible overreactions.

This paper provides new evidence on the overreaction anomaly in the cryptocurrency market by testing the following two hypotheses: after one-day abnormal price movements (overreactions), on the next day abnormal price (i) counter-movements or (ii) momentum movements are observed. For this purpose, a number of statistical tests (both parametric and non-parametric) are carried out. A trading robot approach is then used to investigate whether any detected anomalies generate exploitable profit opportunities. The analysis is carried out for four different cryptocurrencies (BitCoin, LiteCoin, Ripple and Dash).

Empirical Results: analysis confirms the presence of a statistical anomaly in price dynamics in the cryptocurrency market after overreaction days price changes in both directions (in the direction of overreaction and counter movement) are bigger than after normal days.

Next we test whether these anomalies can be exploited to make abnormal profits by using a trading robot approach and considering 2 trading strategies. Strategy 1 is based on the standard overreaction anomaly: there are abnormal counter-reactions after the overreaction day. The trading algorithm in this case is specified as follows: the cryptocurrency is sold (bought) on the open price of the day after the overreaction if an abnormal price increase

(decrease) has occurred. The open position is closed at the end of the day when it was opened. Strategy 2 is based on the momentum effect, the so-called “inertia anomaly”: there are abnormal price movements in the direction of the overreaction on the following day. The trading algorithm is specified as follows: after the overreaction day the cryptocurrency is sold (bought) on the open price of the day after the overreaction if an abnormal price decrease (increase) has occurred. Again, an open position is closed at the end of the day when it was opened.

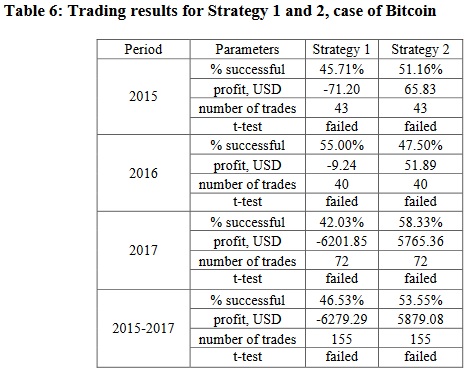

BitCoin prices are used for the analysis (data availability motivated this choice) for the years 2015, 2016, 2017 in turn and then for the whole period 2015-2017.

As can be seen, the results of Strategy 1 are rather stable and in general imply a lack of exploitable profit opportunities from trading based on counter-movements after overreactions in the cryptocurrency market. This applies to all periods. The t-test statistics indicate that the results are not significantly different from the random ones (see Appendix F for details); indirect evidence for this is also provided by the number of profitable trades, which is close to 50%. By contrast, Strategy 2 generates profits in each individual year as well as the full sample, but the results are not significantly different from the random ones (as implied by the t-test statistics). The number of profitable trades is close to 50%. Overall, trading based on the “inertia” anomaly cannot be considered profitable.”

Are you looking for more strategies to read about? Check http://quantpedia.com/Screener

Do you want to see performance of trading systems we described? Check http://quantpedia.com/Chart/Performance

Do you want to know more about us? Check http://quantpedia.com/Home/About

Share onLinkedInTwitterFacebookRefer to a friend