There Exist Two Different Accruals Anomalies

A new financial research paper related to:

#38 – Accrual Anomaly

Authors: Detzel, Schaberl, Strauss

Title: There are Two Very Different Accruals Anomalies

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3069688

Abstract:

We document that several well known asset-pricing implications of accruals differ for investment and non-investment-related components. Exposure to an investment-accruals factor explains the cross-section of returns better than the accruals themselves, and this factor’s returns are negatively predicted by sentiment. The opposite results hold for non-investment accruals. Further tests show cash profitability only subsumes long-term non-investment accruals in the cross-section of returns and economy-wide investment accruals negatively predict stock-market returns while other accruals do not. These results challenge existing accruals-anomaly theories and help resolve mixed evidence by showing that the anomaly is two separate phenomena: a risk-based investment accruals premium and a mispricing of non-investment accruals.

Notable quotations from the academic research paper:

"To measure current-period performance with earnings, accountants add accruals to free cash flow that adjust for long-term investment expenditures and di�fferences in timing between the earning and receipt of cash flows. The evidence in this paper shows that the asset-pricing implications of investment and non-investment components are fundamentally di�fferent. These �findings challenge existing theories of the accruals anomaly and demonstrate that there are not one, but two, accruals anomalies to explain: a risk-based premium for accruals that capture real investment, and a short-lived mispricing of accruals that capture transitory adjustments to profi�tability.

Characteristics-vs-covariances tests show that an investment-accruals factor better explains the cross-section of returns than the investment accruals themselves. This result is evidence against earnings �fixation and profitability-related mispricing explanations of the investment-accruals premium, which do not predict a factor structure of returns. In contrast, the opposite pattern holds for non-investment accruals, consistent with mispricing in the form of a violation of the law of one price. These results are corroborated by evidence that investment accruals predict the cross-section of returns for more than two years (consistent with persistent risk) while non-investment accruals only predict returns for one to eight months (consistent with short-lived mispricing).

While the investment-accruals premium is explained by a risk factor and is therefore not an arbitrage opportunity, the underlying factor is at least partially driven by sentiment as opposed to entirely rational demand. The negative investment-accruals premium is most signifi�cant in times of high sentiment, which is consistent with �firms responding to sentiment-induced overvaluation with high levels of real investment. In contrast, the negative non-investment-accruals premium is signifi�cant only when sentiment is in its bottom quartile. This �finding challenges existing mispricing explanations of accruals that do not predict that overvaluation of high-accruals fi�rms should be

concentrated in low-sentiment periods. Moreover, the profi�tability of non-investment accruals in low-sentiment times challenges the theory that anomaly returns should increase with sentiment because of the relative di�fficulty in arbitraging over-valuation.

Following Lewellen and Resutek (2016), we decompose total accruals into three components: working-capital accruals (�WC), long-term investment accruals (IA), and long-term non-investment or "nontransaction" accruals (NTA). The IA component includes items such as new PP&E that represent expenditures in real investment. The �WC and NTA include items such as accounts payable and receivable as well as depreciation that do not represent new long-term investment expenditures, but only transitory accounting adjustments to cash flows. Hence we refer to �WC and NTA collectively as "non-investment accruals".

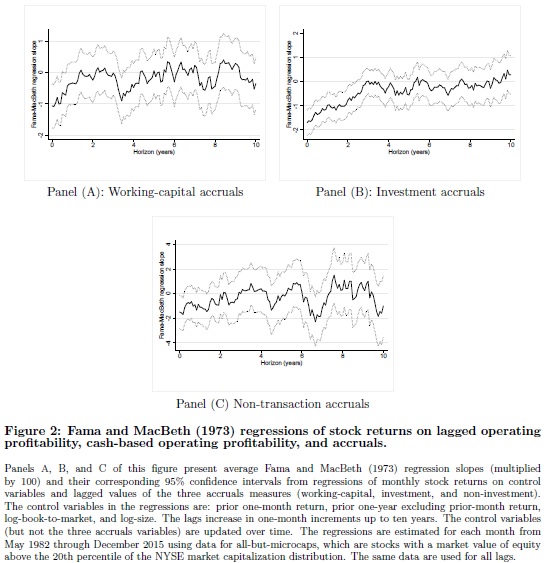

The Fama-Macbeth framework can provide additional evidence of risk versus mispricing. Ball et al. (2016) argue that risk should be more persistent than mispricing and investigate whether longer lags of OA and COP continue to predict returns in Fama-Macbeth regressions. Based on the same motivation, Figure 2 presents Fama-Macbeth regression slopes and their corresponding 95% confi�dence intervals from regressions of monthly stock returns on control variables and lagged values of the three accruals measures (�WC, IA, and NTA). Figure 2 demonstrates NTA and �WC have the least persistent predictive power for returns. In contrast, IA is a more persistent predictor of

returns and remains signifi�cant for up to 28 additional months. Overall, the evidence from Figure 2 is consistent with the IA premium arising from risk, whereas �WC and NTA premia appear to be consistent with mispricing that is arbitraged away after several months.

"

Are you looking for more strategies to read about? Check http://quantpedia.com/Screener

Do you want to see performance of trading systems we described? Check http://quantpedia.com/Chart/Performance

Do you want to know more about us? Check http://quantpedia.com/Home/About

Follow us on:

Facebook: https://www.facebook.com/quantpedia/

Twitter: https://twitter.com/quantpedia

Share onLinkedInTwitterFacebookRefer to a friend