We’ve already analyzed tens of thousands of financial research papers and identified more than 700 attractive trading systems together with hundreds of related academic papers.

Browse Strategies- Unlocked Screener & 300+ Advanced Charts

- 700+ uncommon trading strategy ideas

- New strategies on a bi-weekly basis

- 2000+ links to academic research papers

- 500+ out-of-sample backtests

- Design multi-factor multi-asset portfolios

Upgrade subscription

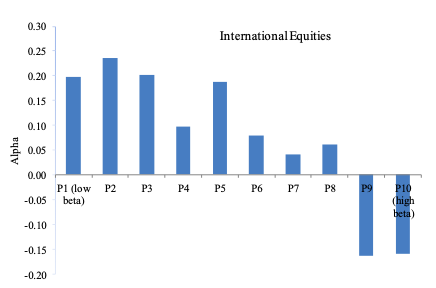

Some investors are prohibited from using leverage, and other investors’ leverage is limited by margin requirements. Therefore, they over-weigh risky assets instead of using leverage, which makes these assets more expensive. High-beta and risky assets should, therefore, deliver lower risk-adjusted returns than low-beta assets. Investors could exploit this inefficiency by using ETFs (or futures) by “betting against beta”, i.e., by going long on a portfolio of low-beta countries (leveraged to a beta of 1) and short on a portfolio of high-beta countries (de-leveraged to a beta of 1). Research also shows this effect isn’t limited to country equity indices and stocks but also works well in other asset classes (even between asset classes).

Fundamental reason

The reason for the anomaly functionality was already stated in the short description – a lot of the investors are prohibited from using leverage, and their only way to achieve higher returns is to buy more risky stocks, which is the main cause for their overvaluation. Investors not facing these constraints could earn above-average returns by exploiting this phenomenon.

- Unlocked Screener & 300+ Advanced Charts

- 700+ uncommon trading strategy ideas

- New strategies on a bi-weekly basis

- 2000+ links to academic research papers

- 500+ out-of-sample backtests

- Design multi-factor multi-asset portfolios

Backtest period from source paper

1980-2009

Confidence in anomaly's validity

Strong

Indicative Performance

6.8%

Notes to Confidence in Anomaly's Validity

Notes to Indicative Performance

per annum, annualized monthly return (geometrically) of 0.55% (from table VIII – return for long short portfolio)

Period of Rebalancing

Monthly

Estimated Volatility

13.08%

Notes to Period of Rebalancing

Notes to Estimated Volatility

Number of Traded Instruments

13

Notes to Number of Traded Instruments

data from source paper from table 2, it is up to investor how many countries he/she would like to use

Notes to Maximum drawdown

Complexity Evaluation

Simple strategy

Notes to Complexity Evaluation

Financial instruments

ETFs, futures

Simple trading strategy

The investment universe consists of all country ETFs. The beta for each country is calculated with respect to the MSCI US Equity Index using a 1-year rolling window. ETFs are then ranked in ascending order based on their estimated beta. The ranked ETFs are assigned to one of two portfolios: low beta and high beta. Securities are weighted by the ranked betas, and the portfolios are rebalanced every calendar month. Both portfolios are rescaled to have a beta of one at portfolio formation. The “Betting-Against-Beta” is the zero-cost zero-beta portfolio that is long on the low-beta portfolio and that shorts the high-beta portfolio. There are a lot of simple modifications (like going long on the bottom beta decile and short on the top beta decile), which could probably improve the strategy’s performance.

Hedge for stocks during bear markets

Partially - Low beta stocks and countries are usually safer during turmoil, and Beta Factor in Country Equity Indexes in a long-short variant can be used as a portfolio hedge against equity risk. However, caution should be used as the popularity of betting-against-beta investing could move valuation (measured by common valuation ratios like P/E, P/B, P/CF, etc.) of low beta countries into excessive-high (compared to neutral market valuation). This popularity of betting-against-beta factor investing and the high valuation of low beta countries can be then detrimental to their performance during market stress.

Out-of-sample strategy's implementation/validation in QuantConnect's framework

(chart+statistics+code)