We’ve already analyzed tens of thousands of financial research papers and identified more than 700 attractive trading systems together with hundreds of related academic papers.

Browse Strategies- Unlocked Screener & 300+ Advanced Charts

- 700+ uncommon trading strategy ideas

- New strategies on a bi-weekly basis

- 2000+ links to academic research papers

- 500+ out-of-sample backtests

- Design multi-factor multi-asset portfolios

Upgrade subscription

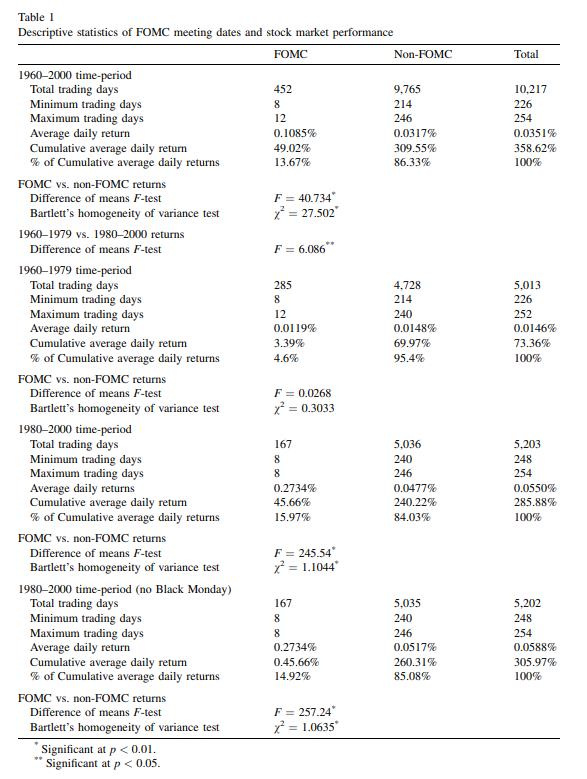

One market wisdom says – „Don’t fight the FED“, and academic research agrees with it. Academic studies show that the S&P 500 index average daily returns during Federal Open Market Committee meetings since 1980 (since FED started to be less secretive and more open about its plans and actions) are outstanding – more than five times greater than returns during other average days on the market. It means that more than 16% of average yearly returns for the equity index is realized during very few days.

Therefore it handsomely pays to be long during these few days. A simple market timing strategy that exploits this anomaly could be created. As it is only a few days in a year, this strategy could be easily leveraged to obtain higher returns.

Fundamental reason

FOMC meetings are mostly positive for the stock market. The FED’s purpose is to address banking panics, maintain the stability of the financial system, contain systemic risk in financial markets, and strengthen economic growth. Therefore it is highly unlikely that FOMC meetings’ conclusions would be highly negative for stocks. This is the main cause of a positive drift.

- Unlocked Screener & 300+ Advanced Charts

- 700+ uncommon trading strategy ideas

- New strategies on a bi-weekly basis

- 2000+ links to academic research papers

- 500+ out-of-sample backtests

- Design multi-factor multi-asset portfolios

Backtest period from source paper

1980-2000

Confidence in anomaly's validity

Strong

Indicative Performance

6.19%

Notes to Confidence in Anomaly's Validity

Notes to Indicative Performance

per annum, return calculated for investor which is long stocks (average daily return 0.2734% – table 1) during FOMC meeting and invested in cash for remaining days (4% return on cash is expected)

Period of Rebalancing

Daily

Notes to Period of Rebalancing

Notes to Estimated Volatility

Number of Traded Instruments

1

Notes to Number of Traded Instruments

Notes to Maximum drawdown

Complexity Evaluation

Simple strategy

Notes to Complexity Evaluation

Financial instruments

CFDs, ETFs, funds, futures

Simple trading strategy

The investor is invested in stocks during FOMC meetings (going long S&P 500 ETF, fund, future, or CFD on a close one day before the meeting and closing position on close after the meeting). Otherwise, he is invested in cash during the remaining days. The strategy has very low exposure to the stock market (8 days during the average year); therefore, it can be very easily leveraged to gain very significant returns.

Hedge for stocks during bear markets

No - The strategy is timing equity market but invests long-only into equity market factor (even that only for a short period of time); therefore is not suitable as a hedge/diversification during market/economic crises.

Out-of-sample strategy's implementation/validation in QuantConnect's framework

(chart+statistics+code)