We’ve already analyzed tens of thousands of financial research papers and identified more than 700 attractive trading systems together with hundreds of related academic papers.

Browse Strategies- Unlocked Screener & 300+ Advanced Charts

- 700+ uncommon trading strategy ideas

- New strategies on a bi-weekly basis

- 2000+ links to academic research papers

- 500+ out-of-sample backtests

- Design multi-factor multi-asset portfolios

Upgrade subscription

A conventional carry trade strategy (systematically selling low-yield currencies against high-yield currencies) is probably the most widely known strategy in the currency market. Recent academic research shows that currency yield (calculated via a forward discount/premium) is useful not only for a cross-sectional analysis but also for individual currencies.

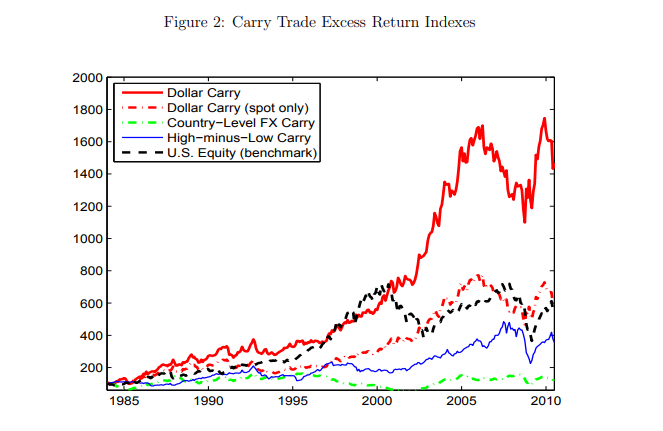

The research paper shows how it is easily possible to time the US dollar against a basket of currencies based on the average forward premium difference. This strategy is called the dollar carry trade, and it is very loosely correlated with conventional carry trade returns. Therefore, this strategy makes a nice add-on to other FX strategies.

Fundamental reason

Academic research shows that the dollar carries trade captures the US-specific compensation for bearing the US as well as global risk, while the global carry trade captures the compensation for global risk exposure, which is common to all countries. The average forward discount of the dollar against a basket of developed country currencies is a strong predictor of excess returns. US investors expect to be compensated more for bearing that risk during recessions when US interest rates are low. This risk premium could be called the dollar risk premium. By implementing the dollar carry trade, he pockets this dollar risk premium when the US risk price is high.

- Unlocked Screener & 300+ Advanced Charts

- 700+ uncommon trading strategy ideas

- New strategies on a bi-weekly basis

- 2000+ links to academic research papers

- 500+ out-of-sample backtests

- Design multi-factor multi-asset portfolios

Backtest period from source paper

1983-2009

Confidence in anomaly's validity

Strong

Indicative Performance

5.6%

Notes to Confidence in Anomaly's Validity

Notes to Indicative Performance

per annum, data from table 1 Panel A, return could be easily leveraged and strategy could deliver higher returns and match a risk with a traditional carry trade strategy or an equity market

Period of Rebalancing

Monthly

Estimated Volatility

8.53%

Notes to Period of Rebalancing

Notes to Estimated Volatility

per annum, data from table 1 Panel A

Number of Traded Instruments

10

Notes to Number of Traded Instruments

it depends on investor’s need for diversification (10-20)

Notes to Maximum drawdown

Complexity Evaluation

Simple strategy

Notes to Complexity Evaluation

Financial instruments

CFDs, forwards, futures, swaps

Simple trading strategy

The investment universe consists of currencies from developed countries (the Euro area, Australia, Canada, Denmark, Japan, New Zealand, Norway, Sweden, Switzerland, and the United Kingdom). The average forward discount (AFD) is calculated for this basket of currencies (each currency has an equal weight). The average 3-month rate could be used instead of the AFD in the calculation. The AFD is then compared to the 3-month US Treasury rate. The investor goes long on the US dollar and goes short on the basket of currencies if the 3-month US Treasury rate is higher than the AFD. The investor goes short on the US dollar and long on the basket of currencies if the 3-month US Treasury rate is lower than the AFD. The portfolio is rebalanced monthly.

Hedge for stocks during bear markets

Not known - Source and related research papers don’t offer insight into the correlation structure of trading strategy to equity market risk; therefore, we do not know if this strategy can be used as a hedge/diversification during the time of market crisis. Currency strategies often have a negative correlation to equities; therefore proposed strategy can be negatively correlated too, but a rigorous backtest is needed to asses if this is the case …

Out-of-sample strategy's implementation/validation in QuantConnect's framework

(chart+statistics+code)