Let’s find out:

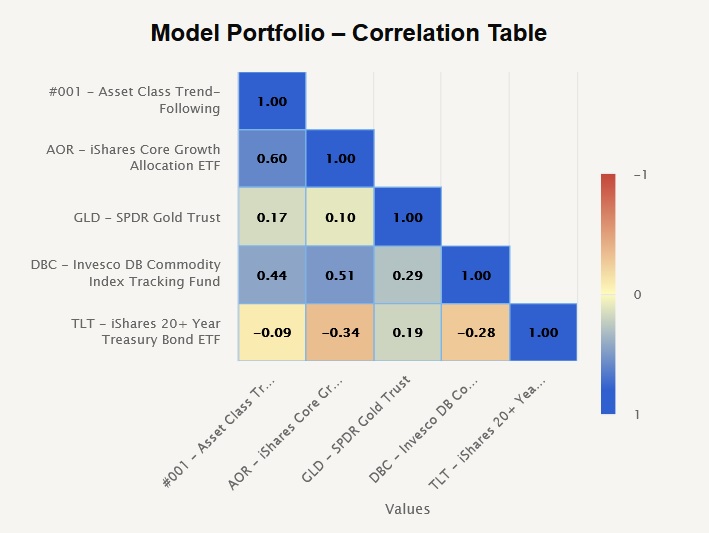

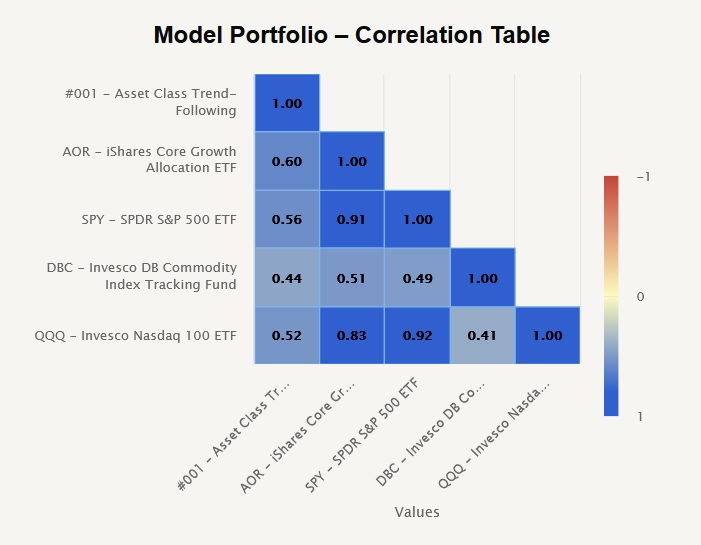

1. The Correlation Analysis report is designed to assess what’s the average correlation among the individual components of our model portfolio. We can first review the correlation table to see the components that are most and which are the least correlated to others.

More diversified portfolio

Less diversified portfolio

2. But what’s too high and what’s low enough number? It really depends on the goal of the portfolio. For example, a multi-asset multi-strategy model portfolio would have more components with low correlation than a model portfolio built from strategies that are trading the same asset. But as a rule of thumb, the lower numbers we have in the table, the more diversified our portfolio is.

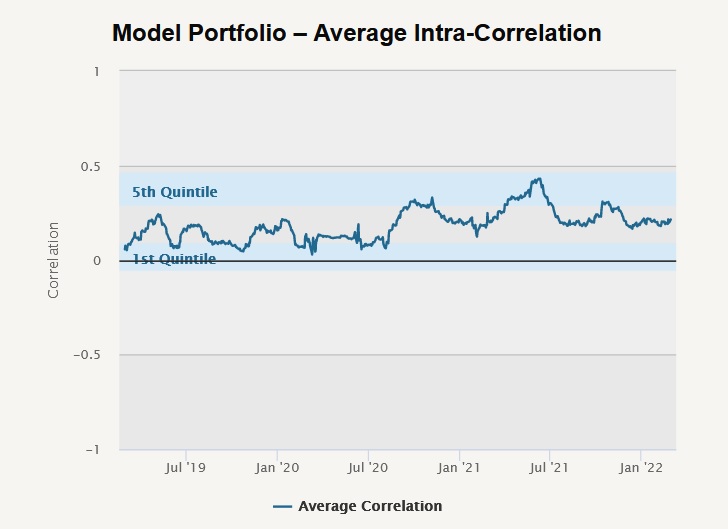

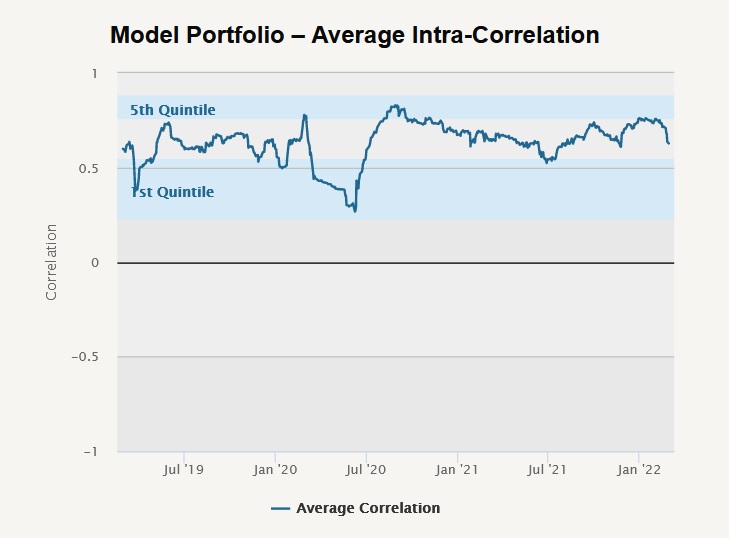

3. The second chart in the Correlation report shows the average correlation among portfolio components over time. Again, the lower number we can achieve, the better.

More diversified portfolio

Less diversified portfolio

4. But it’s also important to observe also correlation spikes. Correlation is often not stable, and spikes during crisis periods are not uncommon.

5. It can signal us to add into our portfolio a strategy/asset that’s less correlated, especially during those crisis periods (see, for example, Crisis Analysis and Crisis Hedge reports).

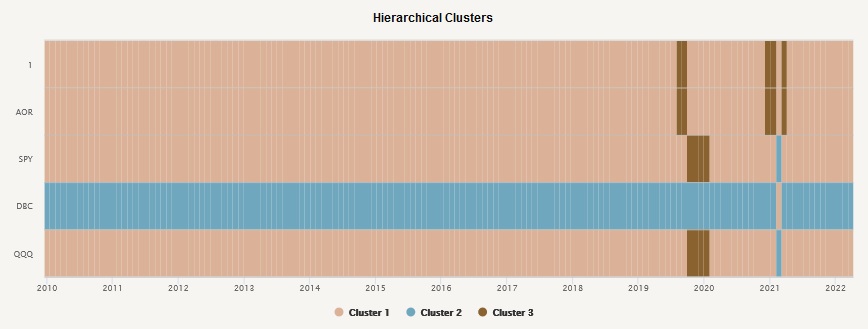

6. But the correlation is not the only measure that we can use to assess diversification. We can also measure clustering inside the model portfolio.

More diversified portfolio

Less diversified portfolio

7. Our Clustering report shows which assets behaved similarly in the past – aka. they were in the same clusters. A diversified portfolio has more different clusters, so individual components do not behave in unison.

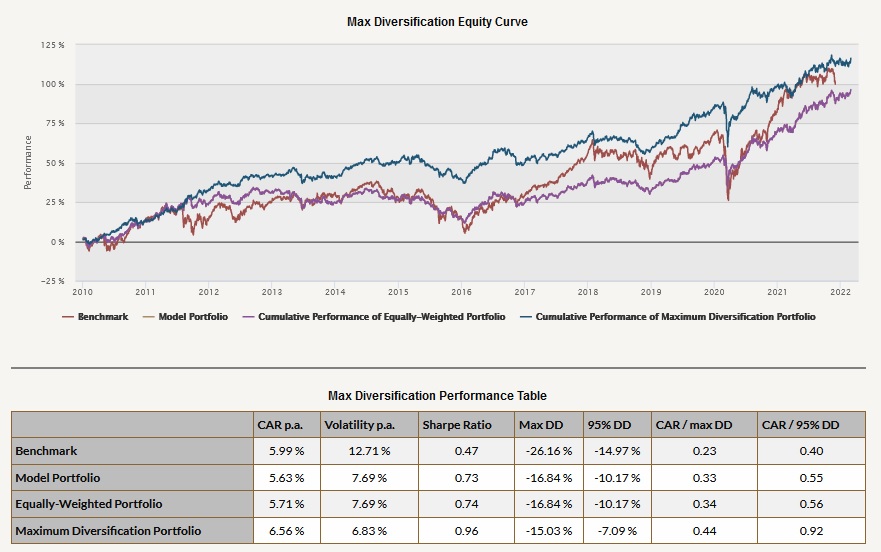

8. How can we obtain a more diversified portfolio if we do not want to add more individual components (assets or strategies) into our model portfolio? We can increase the relative weight of those assets/strategies that have the lowest average correlation. How?

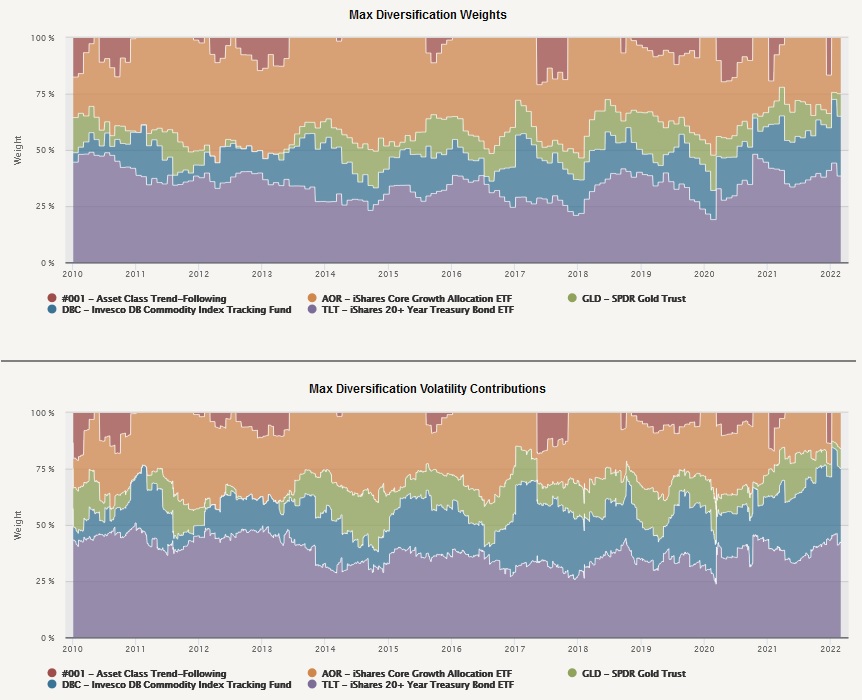

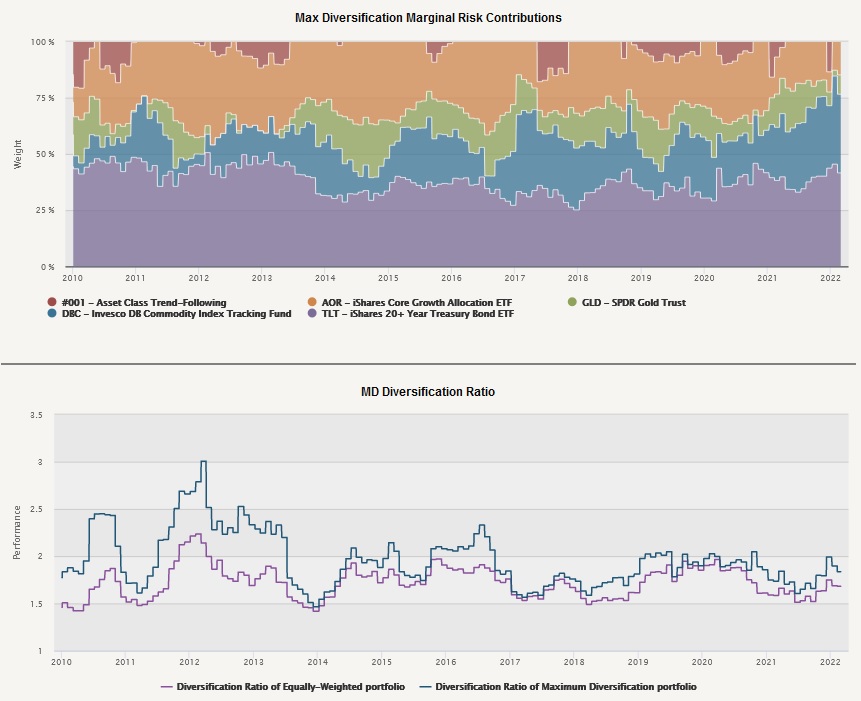

9. Our intro article into risk parity methodologies offers multiple ways to build diversified portfolios efficiently. One of the methods is Maximum Diversification Risk Parity, which builds the maximally diversified portfolios based on assets’ past volatilities and correlations. You may use Quantpedia Pro Portfolio Risk Parity reports to quickly test different weightings of individual components of your model portfolio.