We’ve already analyzed tens of thousands of financial research papers and identified more than 700 attractive trading systems together with hundreds of related academic papers.

Browse Strategies- Unlocked Screener & 300+ Advanced Charts

- 700+ uncommon trading strategy ideas

- New strategies on a bi-weekly basis

- 2000+ links to academic research papers

- 500+ out-of-sample backtests

- Design multi-factor multi-asset portfolios

Upgrade subscription

The Efficient Market Theory has been challenged by the finding that relatively simple anomalies can be utilized to construct trading strategies, that are found to generate statistically significant higher returns than those of the market portfolio. There is also a second possibility where the Market efficiency is also challenged if some simple investment strategy generates a comparable return to that of the market but at a systematically lower level of risk. Well known strategies that challenge efficiency are Momentum, Size, and Value, but a large amount of research has been made about volatility effect in stocks.

Low-risk stocks exhibit significantly higher risk-adjusted returns than the market portfolio, while high-risk stocks significantly underperform on a risk-adjusted basis. Authors Clarke, de Silva, and Thorley have found that minimum variance portfolios, based on the 1000 largest U.S. stocks over the years 1968-2005, achieve a volatility reduction of about 25% while delivering comparable or even higher average returns than the benchmark market portfolio. This paper has found that portfolios, which consist of stocks with the lowest historical volatility, are associated with Sharpe ratio improvements, that are even larger than those in the aforementioned minimum variance portfolios. Baker, Bradley, and Wurgler in their work: Benchmarks as Limits to Arbitrage: Understanding the Low Volatility Anomaly, have proved that over the past 41 years, high volatility and high beta stocks have substantially underperformed low volatility and low beta stocks in U.S. markets. Clearly, there is a lot of evidence that the low-volatility effect is an anomaly that works and should be utilized in an investing strategy. Concentrating on long-term volatility, the anomaly can be used by the investor to create decile portfolios that are based on a straightforward ranking of stocks on their historical return volatility. Afterward, the investor would simply long the decile with the stocks with the lowest volatility (moreover, he can short the decile of stocks with the highest volatility).

Going long on low-risk stocks and short on high-risk stocks produce a significant volatility spread. However, a long-short portfolio isn’t the only way to exploit this anomaly. A long-only strategy is much easier to implement than a long-short strategy. The investor could go long on low volatility stocks and enjoy the higher Sharpe ratio rather than standard equity indices.

Fundamental reason

Firstly, to take full advantage of the attractive absolute returns of low-risk stocks, there is a need for leverage. However, in practice, either many investors are not allowed, or they are unwilling to apply leverage, especially the leverage needed for exploiting the volatility effect. This results in the fact that the opportunity, which is presented by low-risk stocks, cannot be easily arbitraged away. Secondly, the volatility effect could be the result of an inefficient and decentralized investment approach. The problem of benchmark driven investing is that asset managers have an incentive to tilt towards high beta or high volatility stocks. This is a relatively simple way for every asset manager to generate returns above the average if he assumes that the CAPM at least partially holds. This results in overpriced high-risk stocks, while low-risk stocks may become under-priced; this is particularly consistent with the return patterns which were documented in this paper.

The volatility effect may also be caused by behavioral biases among private investors. Private investors will overpay for risky stocks that are perceived to be similar to lottery tickets because they are in the search for high returns in an as short time as possible. Additionally, Li, Sullivan, and García-Feijóo in their paper, The Low-Volatility Anomaly: Market Evidence on Systematic Risk versus Mispricing, have found out that the anomaly returns associated low-volatility stocks can be attributed to market mispricing or compensation for higher systematic risk. Soe, in “The low-volatility effect: A comprehensive look“, claims that volatility-effect challenges the traditional equilibrium asset pricing theory that an asset’s expected return is directly proportional to its beta or systematic risk, or, in other words, higher-risk securities should be rewarded with higher expected returns while lower-risk assets receive lower expected returns. The evidence seems to be endless. Moreover, the volatility effect is similar in size compared to classic effects (momentum, size, and value) and remains significant after Fama-French adjustments and double sorts. Last but not least, concentrating on long-term, past three years, volatility implies a much lower portfolio turnover.

- Unlocked Screener & 300+ Advanced Charts

- 700+ uncommon trading strategy ideas

- New strategies on a bi-weekly basis

- 2000+ links to academic research papers

- 500+ out-of-sample backtests

- Design multi-factor multi-asset portfolios

Backtest period from source paper

1986-2006

Confidence in anomaly's validity

Strong

Indicative Performance

11.3%

Notes to Confidence in Anomaly's Validity

Notes to Indicative Performance

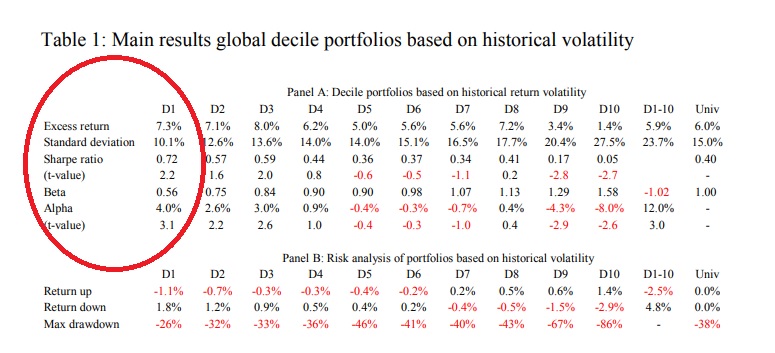

per annum, long-only portfolio results from table 1 for D1 portfolio (return over risk-free rate) plus estimated risk-free rate (4%)

Period of Rebalancing

Monthly

Estimated Volatility

10.1%

Notes to Period of Rebalancing

Notes to Estimated Volatility

results from table 1 for D1 portfolio,

Number of Traded Instruments

50

Notes to Number of Traded Instruments

depends on investment universe (50 for US S&P500)

Notes to Maximum drawdown

Complexity Evaluation

Complex strategy

Notes to Complexity Evaluation

Financial instruments

stocks

Simple trading strategy

The investment universe consists of global large-cap stocks (or US large-cap stocks). At the end of each month, the investor constructs equally weighted decile portfolios by ranking the stocks on the past three-year volatility of weekly returns. The investor goes long stocks in the top decile (stocks with the lowest volatility).

Hedge for stocks during bear markets

Partially - Low volatility stocks (low-risk stocks) are usually safer during turmoil and Low Volatility Effect in a long-short variant (not long-only, but long-short, where the investor holds the lowest volatility decile od stocks and shorts the highest volatility decile of stocks) can be used as a portfolio hedge against equity risk. However, caution should be used as the popularity of low volatility investing could move valuation (measured by common valuation ratios like P/E, P/B, P/CF, etc.) of low volatility stocks into excessive-high (compared to neutral market valuation). This popularity of low volatility factor investing and high valuation of low volatility stocks can be then detrimental to their performance during market stress.

Out-of-sample strategy's implementation/validation in QuantConnect's framework

(chart+statistics+code)