![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

Don’t know exactly how to use our tools? Read our Quantpedia Answers series, which will give you a manual and responses to the most frequently asked questions through brief and clear instructions.

How much can my Portfolio Lose?

Historical and also future potential losses of your portfolio are very easy to analyze in Quantpedia Pro.

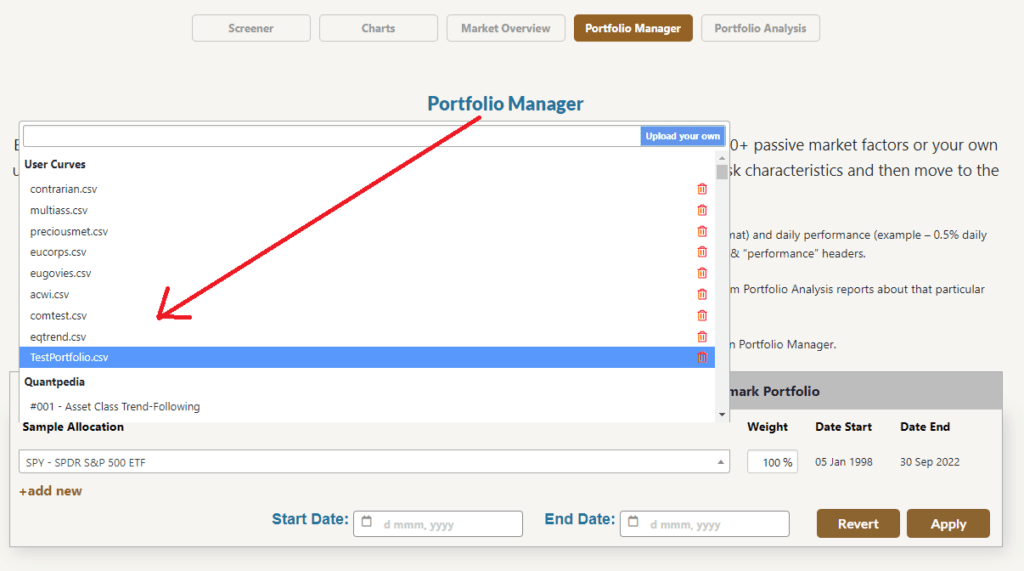

1. Choose your own Portfolio in Portfolio Manager:

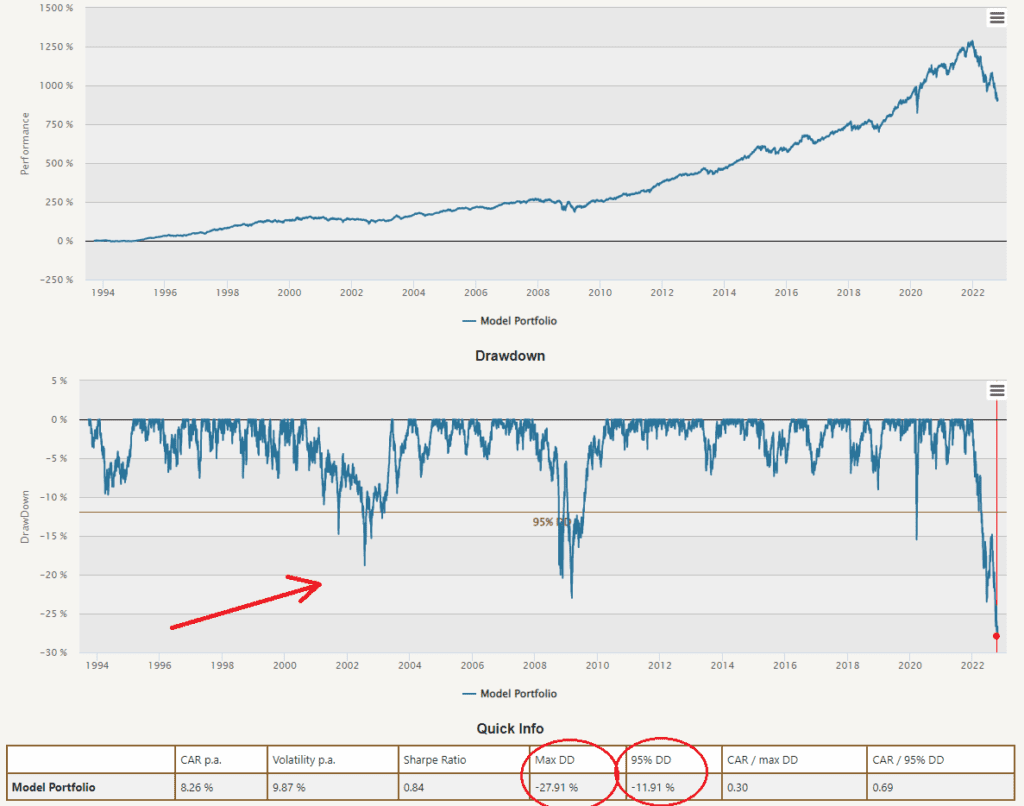

Historical Drawdowns

2. You can easily observe historical losses of your portfolio directly in Quantpedia Pro’s Portfolio Manager and also in a Basic Overview of your portfolio:

- Drawdown chart

- Maximum drawdown / loss value

- 95th percentile of the drawdown

Value at Risk

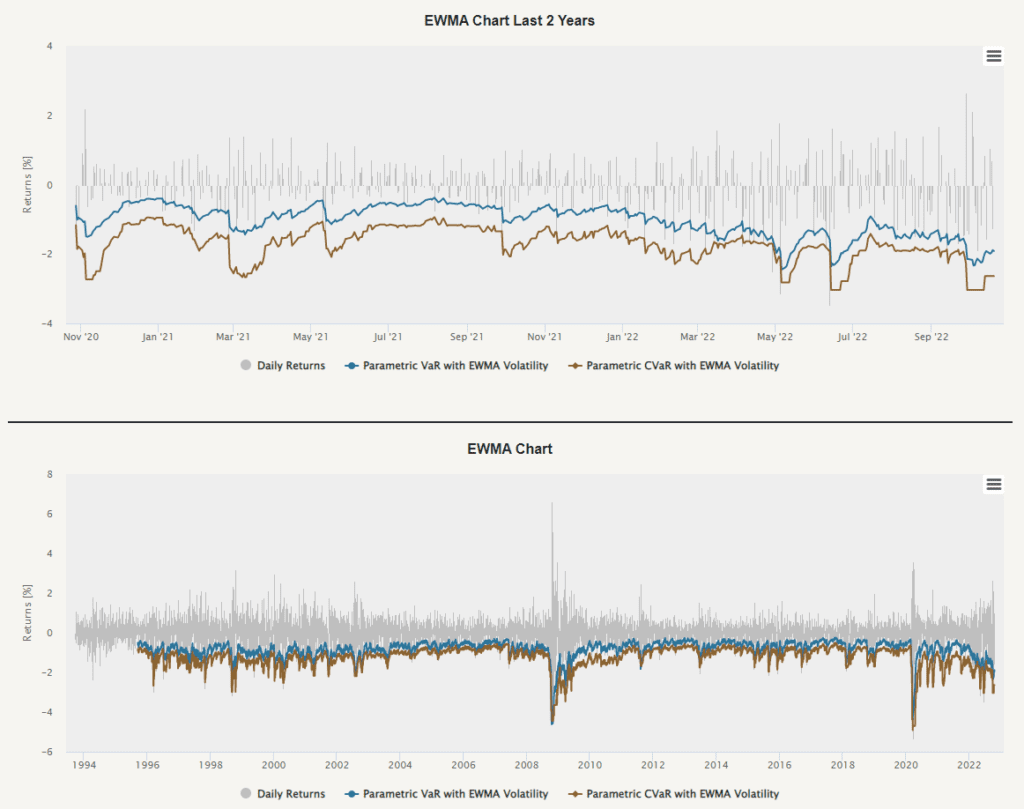

3. One of the most popular measures of historical and also future potential losses is Value at Risk, or VaR. In Quantpedia Pro’s Value at Risk report, you can easily observe the 3 of the most popular VaR methods applied to your portfolio rolling in time. Just choose Value at Risk report:

- Historical Value at Risk

- Parametric Value at Risk

- Exponentially weighted (EWMA) Value at Risk

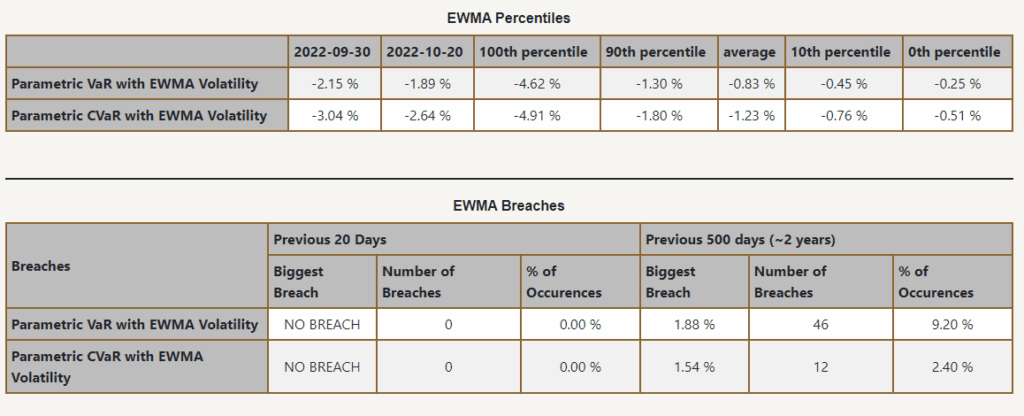

And not only that! Quantpedia Pro offers much more, you can also analyze:

- Conditional value at Risk (CVaR), for 3 different methods

- Historical Distribution of Value at Risk and CVaR

- Frequency of breaches of VaR/CVaR calculated in real-time

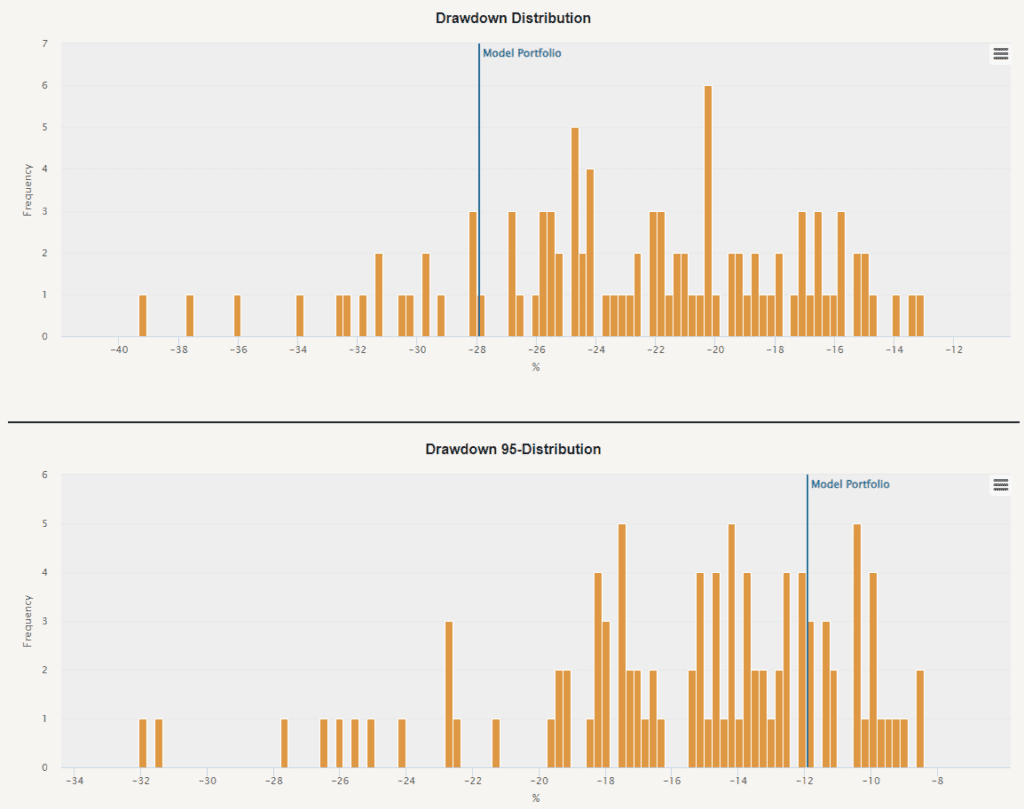

Monte Carlo Simulations

4. Last but not least, you can even perform famous Monte Carlo Simulations for your portfolio in a matter of seconds thanks to Quantpedia Pro! Just choose Monte Carlo report:

Then you can easily analyze potential losses of your portfolio, for example:

- Probability of a specific loss

- Drawdown distribution in various hypothetical scenarios

- The biggest potential loss of your portfolio

- Distribution of “typical” (95th percentile) drawdowns