![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

Don’t know exactly how to use our tools? Read our Quantpedia Answers series, which will give you a manual and responses to the most frequently asked questions through brief and clear instructions.

How should I Weigh my Investments?

So you have a portfolio with several different assets or strategies. But how to weight them correctly? What allocation method to choose? Should you weigh your investments equally, or based on volatility, or in some different way?

Luckily, thanks to Quantpedia Pro, you can check and analyze numerous Portfolio Allocation methods in a matter of seconds:

- Equal / Custom Fixed weights

- Various Risk Parity weighing methods

- Markowitz / Mean Variance weights

- Various CPPI / capital protection weighing methods

- Clustering-based weighing

- Tactical / Dynamic weights

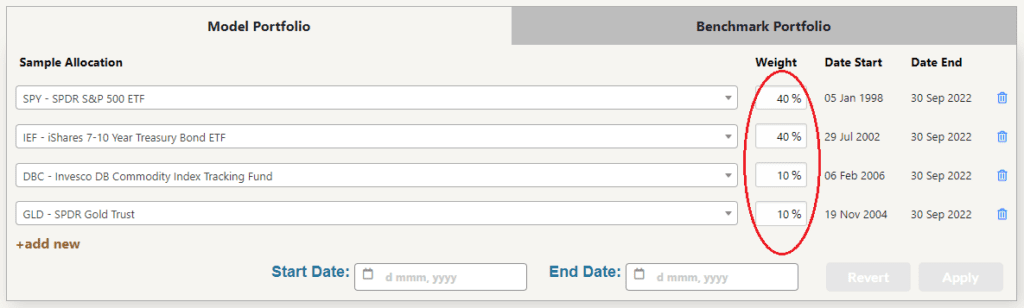

1. Choose your assets and/or strategies for your weighing analysis in the Portfolio Manager:

Equal Weight

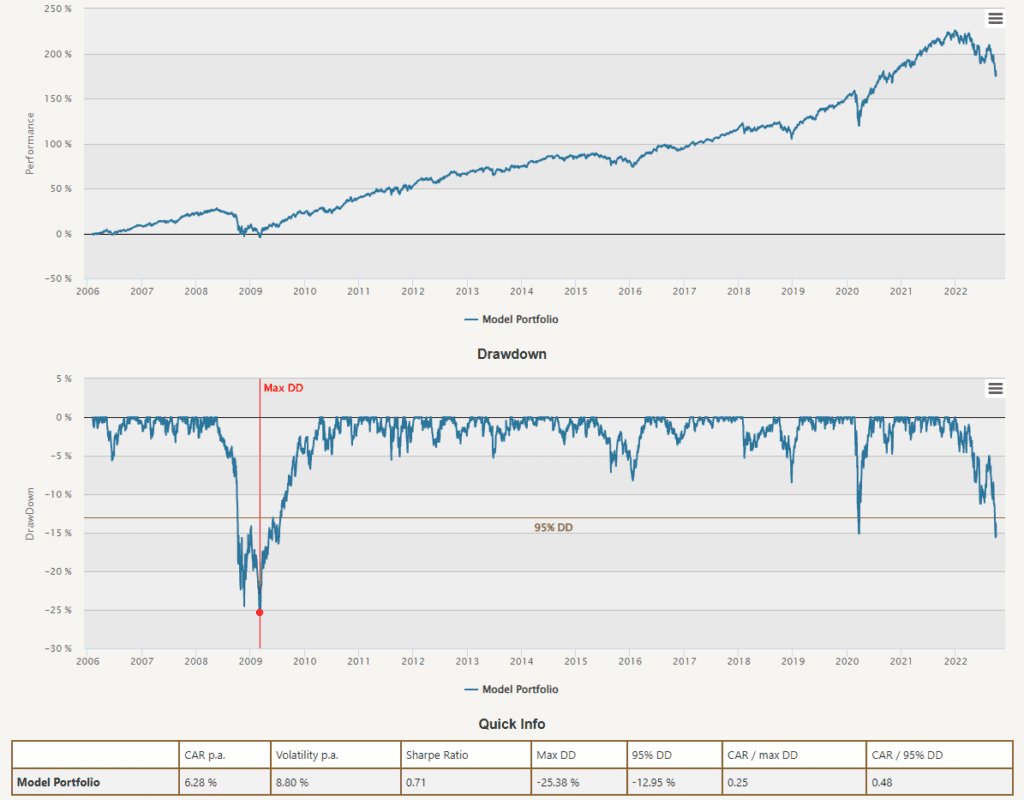

2. You can analyze performance and risk of your Custom Fixed Weights (rebalanced daily) or just simple Equal Weights in both Quantpedia Pro’s Portfolio Manager and also in a Basic Overview report of your portfolio:

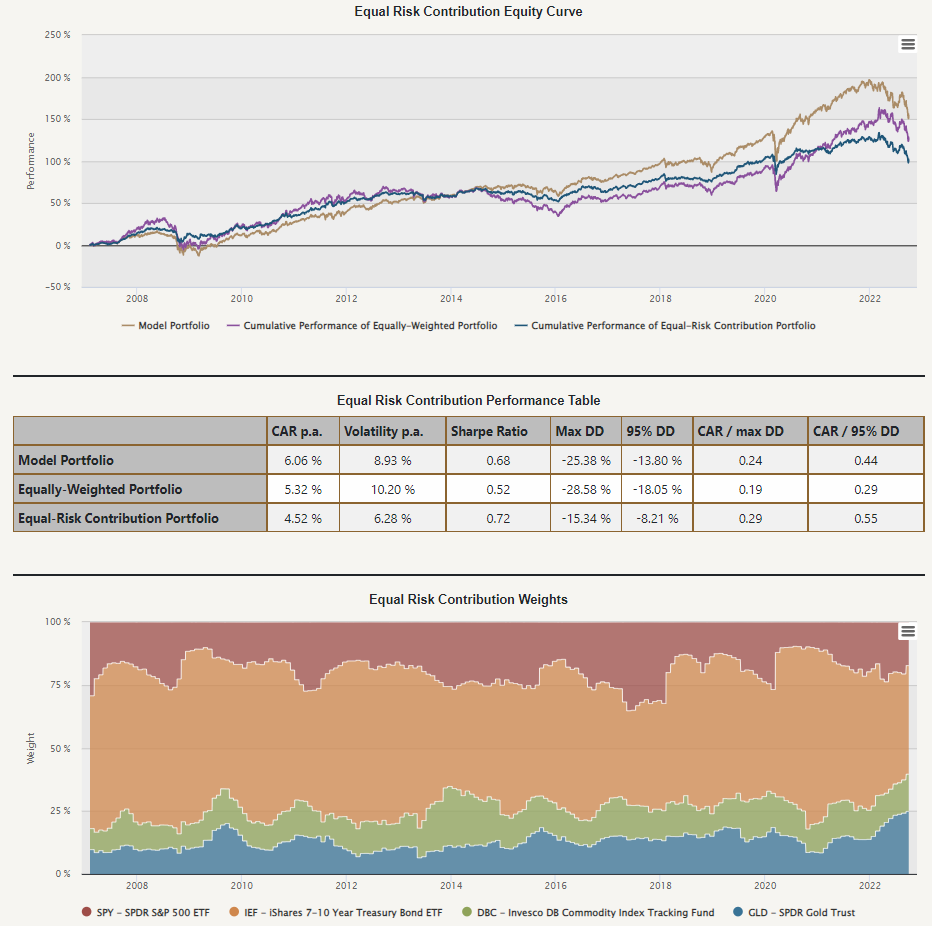

Risk Parity methods

3. Quantpedia Pro subscribers can quickly analyze several different Risk Parity portfolio allocation methods applied to their portfolios, by selecting the respective Portfolio Analysis tool:

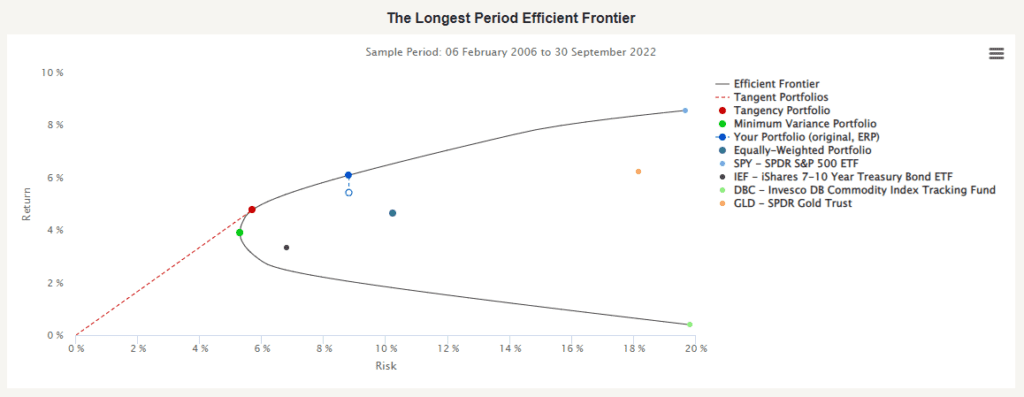

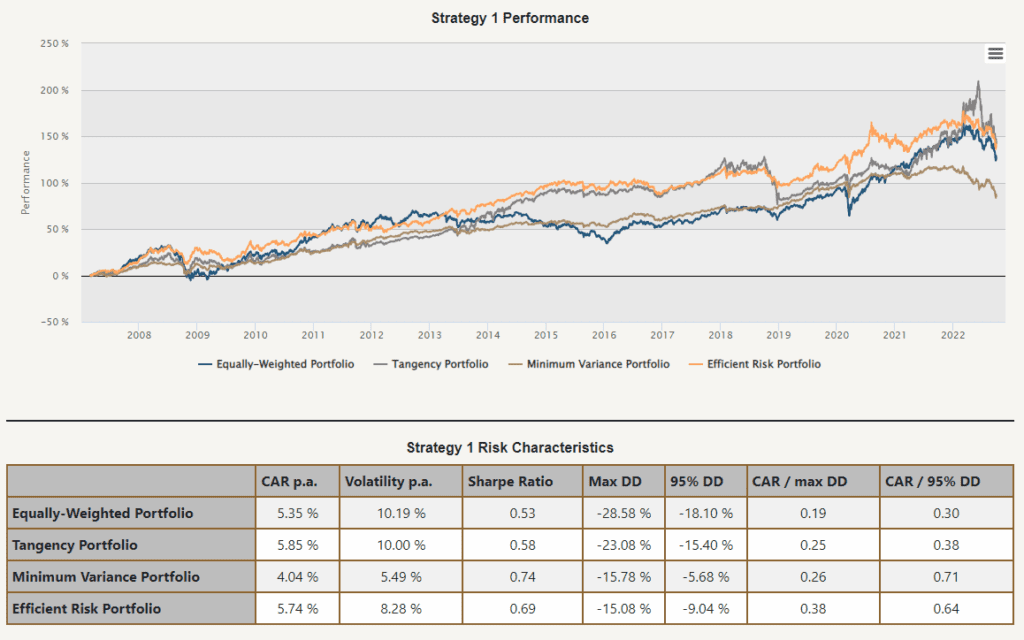

Mean Variance weights

4. You can also easily apply various Harry Markowitz’s mean-variance weighing schemes to your portfolio in Quantpedia Pro, by selecting a Markowitz Portfolio Report:

You can actually even test tactical systematic strategies based on dynamic Markowitz allocation in Quantpedia Pro:

CPPI methods

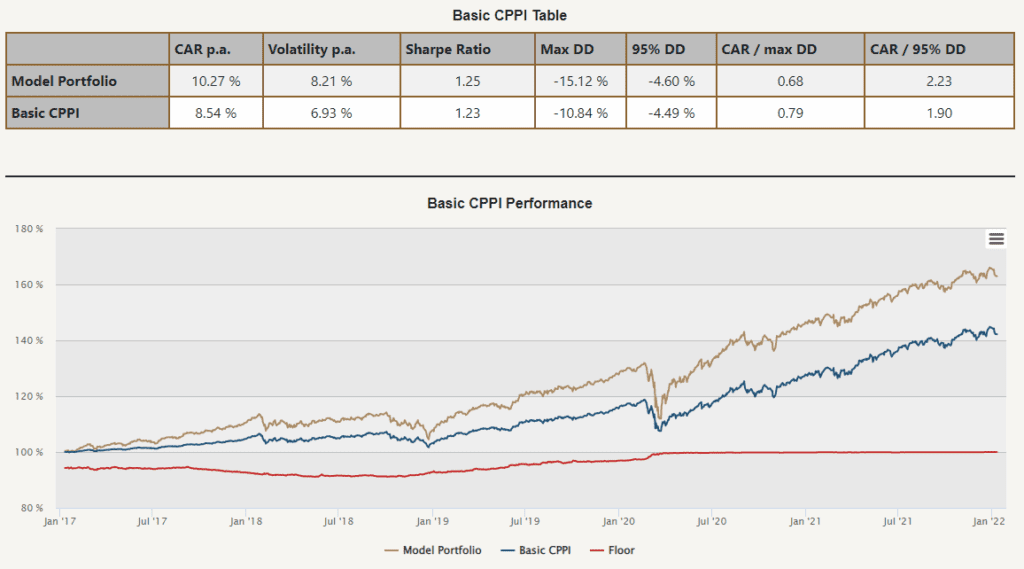

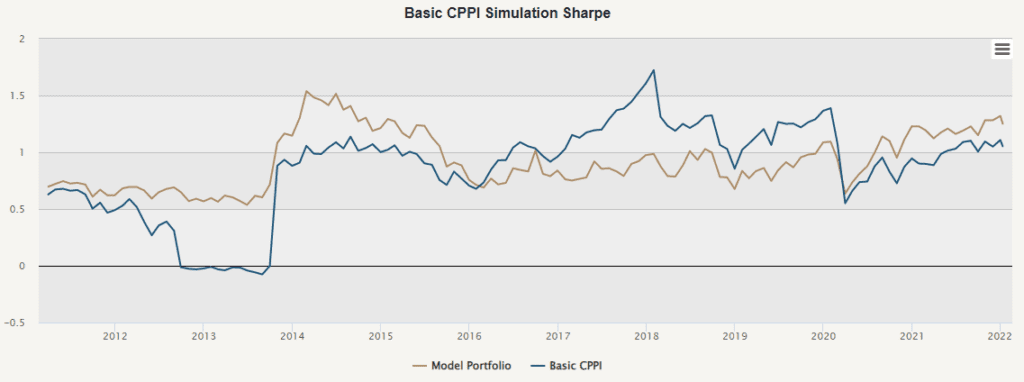

5. Do you want to protect the starting capital of your portfolio? Then you might be interested in a dynamic protection strategy called Constant Proportion Portfolio Insurance (or CPPI). Just select Quantpedia Pro’s CPPI report to see how it works on your portfolio:

Tactical weights

6. Finally, if you think about tactically increasing/decreasing weights of your assets or your portfolio as such, Quantpedia Pro offers several reports to test many such strategies: