A new financial research paper has been published and is related to:

Authors: Liu

Title: Asset Pricing Anomalies and the Low-Risk Puzzle

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3258015

Abstract:

The original observation in Black, Jensen and Scholes (1972) that the security market line is too flat – the beta anomaly – is a driving force behind a number of well-documented cross-sectional asset pricing puzzles. I document that returns to a broad set of anomaly portfolios are negatively correlated with the contemporaneous market excess return. I show that this negative covariance implicitly embeds the beta anomaly in these cross-sectional return puzzles. Taking into account the exposure to the beta anomaly either attenuates or eliminates the economic and statistical significance of the risk-adjusted returns to a large set of asset pricing anomalies.

Notable quotations from the academic research paper:

"Defying both theory and intuition, low beta assets have consistently outperformed high beta assets, both over time and across various asset markets. This observation has come to be known as the beta anomaly. In this paper, I present evidence that the beta anomaly is embedded in a broad set of cross-sectional asset pricing puzzles.

I document that anomaly portfolio returns share a striking and peculiar pattern: returns are positive and peak in market downfalls, but are negative when the market rises. I verify that this negative covariance is empirically equivalent to the long portfolios holding stocks with lower betas relative to the short portfolios. Mitigating the exposure to the beta anomaly either attenuates or eliminates the economic and statistical signi ficance of the risk-adjusted returns to numerous cross-sectional anomalies.

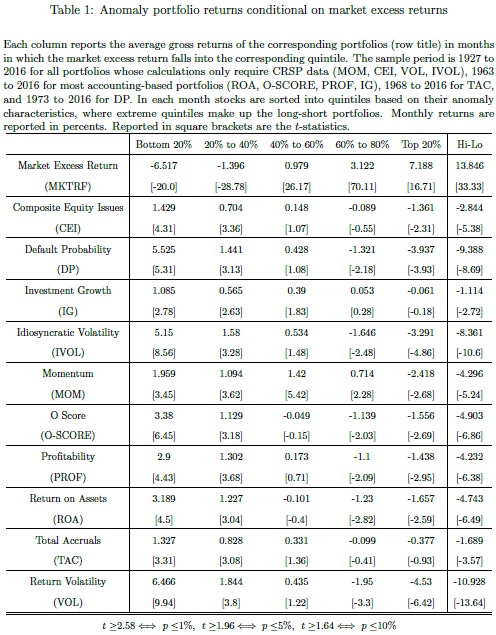

This paper analyzes a set of ten asset pricing puzzles representative of di fferent types of cross-sectional return predictors documented in the literature. The sample includes anomalies that are operation-based (total accruals, return on assets, pro fitability, investment growth), return-based (momentum), risk-based (O-score, default probability, return volatility, idiosyncratic volatility), as well as issuance-related (composite equity issues). It is remarkable that portfolios formed on such a wide range of characteristics all have returns that are negatively correlated with the market.

The observed negative covariance has two immediate implications. First, to the extent that these anomaly portfolios hold "quality" stocks (profi table, high past return, mature, low probability of failure, etc.), the fact that they pay off in bad states of the world is consistent with flight to quality in market downturns. The negative covariance between "quality" stocks and the market points to the beta anomaly as an explanation for why "quality" stocks have high average returns. Second, the shared negative covariance with the market is suggestive of the data mining concern in the empirical asset pricing literature – the search for cross-sectional return predictability has led to di fferent dimensions to slice the data, many of which somehow implicitly take advantage of the beta anomaly.

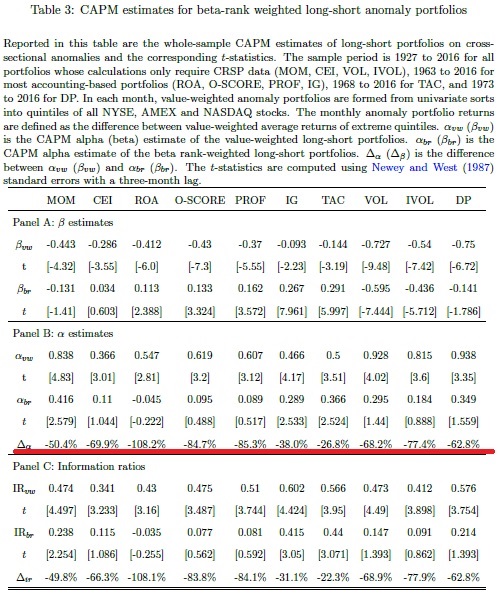

To show that the beta anomaly subsumes the risk-adjusted returns of the cross-sectional anomalies, I mitigate the long-short portfolios' exposure to the beta anomaly in two complementary ways.

First, I consider an alternative weighting scheme when aggregating returns to the portfolio level: I weight stocks in long legs using the ascending decile ranking of their pre-formation betas, and weight stocks in short legs using the descending decile beta rankings. This way of constructing portfolios keeps the original portfolio constituents while putting more weight on high beta stocks in the long leg, and more weight on low beta stocks in the short leg, relative to value-weighted portfolios.

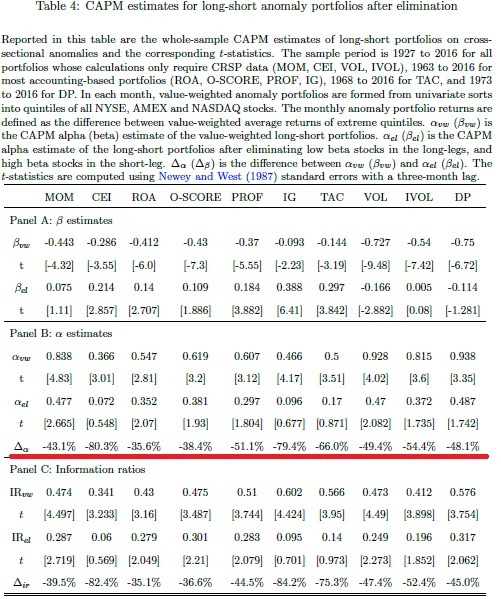

The second approach complements the first by keeping the value-weighting scheme from the original portfolio construction, but removing stocks with low betas in the long leg, and stocks with high betas in the short leg.

Together these two approaches allow me to separate the e ffect of beta exposure from the e ect of the anomaly characteristics on the long-short portfolios' alphas. Both modifi ed portfolio construction methods reduce or remove the exposure to the beta anomaly, and lead to reduced CAPM alphas for the anomaly trading strategies. In terms of economic magnitude, the reduction in trading profi tability ranges from 27% up to a reversed sign."

Are you looking for more strategies to read about? Check http://quantpedia.com/Screener

Do you want to see performance of trading systems we described? Check http://quantpedia.com/Chart/Performance

Do you want to know more about us? Check http://quantpedia.com/Home/About

Follow us on:

Facebook: https://www.facebook.com/quantpedia/

Twitter: https://twitter.com/quantpedia

Share onLinkedInTwitterFacebookRefer to a friend