A related paper has been added to:

#118 – Time Series Momentum Effect

Authors: Ferreira, Silva, Yen

Title: Information ratio analysis of momentum strategies

Link: http://arxiv.org/abs/1402.3030

Abstract:

In the past 20 years, momentum or trend following strategies have become an established part of the investor toolbox. We introduce a new way of analyzing momentum strategies by looking at the information ratio (IR, average return divided by standard deviation). We calculate the theoretical IR of a momentum strategy, and show that if momentum is mainly due to the positive autocorrelation in returns, IR as a function of the portfolio formation period (look-back) is very different from momentum due to the drift (average return). The IR shows that for look-back periods of a few months, the investor is more likely to tap into autocorrelation. However, for look-back periods closer to 1 year, the investor is more likely to tap into the drift. We compare the historical data to the theoretical IR by constructing stationary periods. The empirical study finds that there are periods/regimes where the autocorrelation is more important than the drift in explaining the IR (particularly pre-1975) and others where the drift is more important (mostly after 1975). We conclude our study by applying our momentum strategy to 100 plus years of the Dow-Jones Industrial Average. We report damped oscillations on the IR for look-back periods of several years and model such oscilations as a reversal to the mean growth rate.

Notable quotations from the academic research paper:

"Similar to Moskowitz, Ooi and Pedersen, we focus on the momentum of individual assets. We study the technical rule (moving average of past returns) for one asset, therefore avoiding the portfolio effect that is important for cross-section momentum. This work adds to the paper of [ Moskowitz, T. J., Ooi, Y. H., Pedersen, L. H.. Time series momentum.] by looking at the information ratio of the time series momentum strategy. Our work also contributes to the literature of linking momentum to cycles/regimes. However, contrary to the previous studies, we do not associate economical episodes to the regimes. Our approach is to divide and transform the data in a way such that the final asset returns are as close as possible to stationary. We believe that our work is new in this respect.

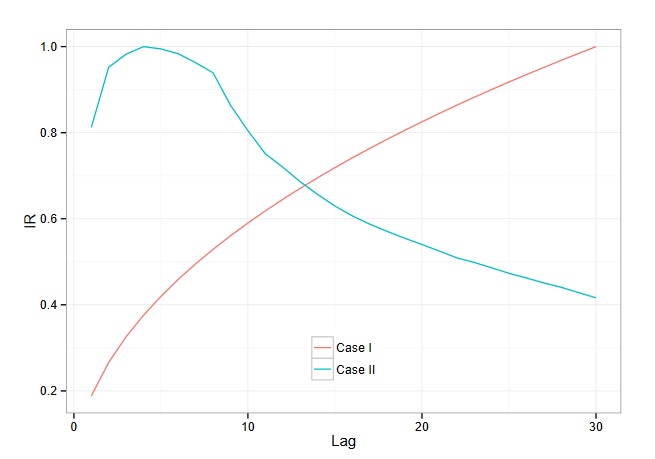

We study momentum by looking at the risk adjusted performance measured by the information ratio (IR) as a function of the look-back lag used to construct the portfolio. Our main new contribution from a mathematical point of view, is to present in close form the risk associated with the momentum strategy. Previous works calculate the same expression for the average return as given here, however they do not calculate the standard deviation of the strategy. Furthermore, we analyze the stability of the results across time as non-stationary effects become important in explaining the results. We find that both autocorrelation and mean drift of the random process are important in the final performance of the strategy. In particular, for look-back periods up to 4 months, the most important effect is the autocorrelation; and for look-back periods larger than 4 months to 1 year, the drift. However, in contrast with previous studies, we find that the mean drift is the most important factor after 1975.

In case I, all the autocorrelations are zero, performance comes from the drift. In case II all performance comes from autocorrelation. Lag is in weeks.

"

"

Are you looking for more strategies to read about? Check http://quantpedia.com/Screener

Do you want to see performance of trading systems we described? Check http://quantpedia.com/Chart/Performance

Do you want to know more about us? Check http://quantpedia.com/Home/About

Share onLinkedInTwitterFacebookRefer to a friend