An Analysis of PIMCO’s Bill Gross’ Alpha

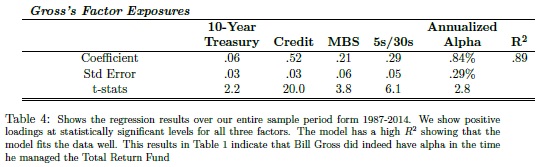

Bill Gross is probably the most known fixed income fund manager. A new academic paper sheds more light on his track record and sources of his stellar performance … Authors: Dewey, Brown Title: Bill Gross’ Alpha: The King Versus the Oracle Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3345604 Abstract: We set out to investigate whether ”Bond King” Bill Gross demonstrated alpha (excess average return after adjusting for market exposures) over his career, in the spirit of earlier papers asking the same question of ”Oracle of Omaha,” Warren Buffett. The journey turned out to be more interesting than the destination. We do find, contrary to previous research, that Gross demonstrated alpha at conventional levels of statistical significance. But we also find that result depends less on the historical record than on whether we take the perspective of academics interested in market efficiency, investors picking a fund or someone (say a potential employer) asking whether a manager has skill or is throwing darts to pick positions. These are often thought to be overlapping or even identical questions. That’s not completely unreasonable in equity markets, but in fixed income these are distinct. We also find quantitative differences, mainly that fixed-income securities have much higher correlations with each other than equities, make alpha 4.5 times as hard to measure for Gross than Buffett. We don’t think our results will have much practical effect on attitudes toward Gross as an investor, but we hope they will advance understanding of what alpha means and appropriate ways to estimate it. Notable quotations from the academic research paper: “Superstar bond portfolio manager Bill Gross announced his retirement last week. From 1987 to 2014, his PIMCO Total Return fund generated 1.33% per year of alpha versus the Barclays US Credit index, with a t-statistic of 3.76. For many years his fund was the largest bond fund in the world, and was generally considered to be the most successful. This track record inspired us to take a closer quantitative look along the lines of Frazzini, Kabiller and Pedersen’s Buffett’s Alpha (FKP). Gross, like Buffett, often publicly discussed what he perceives as the drivers of his returns. At the Morningstar Conference in 2014 and in a 2005 paper titled “Consistent Alpha Generation Through Structure” Gross highlighted three factors behind his returns: more credit risk than his benchmark, more 5-year and less 30-year exposure, and long mortgages and other securities with negative convexity. We present five main findings: 1. We con firm that those three factors, plus one for the general level of interest rates, explain 89% of the variance in Gross’ monthly return over the 27-year period. We further estimate that Gross outperformed a passive factor portfolio by 0.84% per year, which is significant at the 5% level. Gross’ compounded annual return over the period was 7.52%, versus 6.44% for the Barclay’s Aggregate US Index. So we find that most of his 1.08% annual outperformance of the index was alpha.

| What about Data? Look at Quantpedia’s Algo Trading Discounts. |

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend