High-yield bond ETFs represent a unique financial vehicle: they are highly liquid instruments that hold inherently illiquid securities, creating a fertile ground for predictable market behaviors. Our latest research uncovers an intriguing anomaly within these ETFs, similar to those observed in the stock market: overnight returns are systematically higher than intraday returns. This overnight anomaly in high-yield bonds is not only prevalent but also exhibits a distinct seasonal pattern, primarily from Monday’s close to Tuesday’s open and from Tuesday’s close to Wednesday’s open. Additionally, this anomaly displays a reversal characteristic, where overnight performance is typically more robust following a negative close-to-close performance in the preceding period. These findings reveal potential opportunities for trading strategies that leverage these consistent overnight return patterns, offering new insights into high-yield bond trading dynamics.

Introduction

We pay much attention to the stock market (or commodities & cryptocurrencies) and sometimes omit coverage of debt and bond markets. Unjustly. This is the time to make a little bit of payback; when rates may finally be about to go down again, this could be the right time to start looking at fixed-income markets again. However, we will not be concerned today with government debt; instead, we will look closely at corporate debt, amongst those riskiest.

High-yield bonds, often called junk bonds, are corporate debt securities that offer higher interest rates than investment-grade bonds due to their lower credit ratings. These bonds are typically issued by companies with higher debt ratios or those in capital-intensive industries, making them more susceptible to default risk. The higher yields serve as compensation for investors taking on this increased risk (higher volatility, interest rate, and liquidity risks). High-yield bonds are rated below BBB- by Standard & Poor’s and Fitch or below Baa3 by Moody’s, indicating a higher probability of default1.

iShares iBoxx $ High Yield Corporate Bond ETF (HYG) seeks to track the Markit iBoxx USD Liquid High Yield Index Benchmark Index with a sufficient 1,240 Holdings, primarily traded on the NYSE Arca Exchange. However, it’s a highly liquid ETF (exchange-traded fund) vehicle for illiquid assets since underlying HY (high yield) bonds sometimes have very low turnover and wide spreads, and so, that brings it specifics – interesting effects, especially during periods of financial stress. That brings us ideas that might be implemented for basic and advanced trading strategies, or at least employ better entries into new and existing from already held positions.

Conceptualization of Study

- First, we got the needed data: We compiled a list of high-yield bond ETFs, which serve as liquid vehicles for an illiquid asset class. HYG was ultimately chosen.

- Then, some tests for traditional anomalies were performed. They were selected because those anomalies are often observed in other asset classes and might be foresighted also in this territory.

- We compared performance over the daily and nightly sessions.

- We immediately thought and tested an end-of-day reversal strategy, where we purchase at the close if the previous day’s performance is negative.

- We tested daily seasonality impact on the HYG performance.

Overnight Effect

We downloaded iShares iBoxx $ High Yield Corporate Bond ETF (HYG) data from Yahoo Finance. We include samples from 2007-11-04 up until 2024-07-24.

Then, we adjusted closed and open prices; closed ones are readily available from YF, but opening prices needed adjustments (adjusted close prices are adjusted for splits and dividend and/or capital gain distributions; open needed the same).

Recently, Yahoo Finance discontinued free end-of-day data downloads. As a result, we recommend sourcing data from our preferred provider, EODHD.com – the sponsor of our blog. EODHD offers seamless access to +30 years of historical prices and fundamental data for stocks, ETFs, forex, and cryptocurrencies across 60+ exchanges, available via API or no-code add-ons for Excel and Google Sheets. As a special offer, our blog readers can enjoy an exclusive 30% discount on premium EODHD plans.

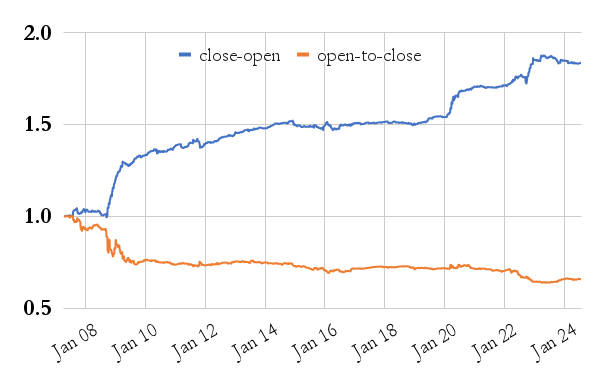

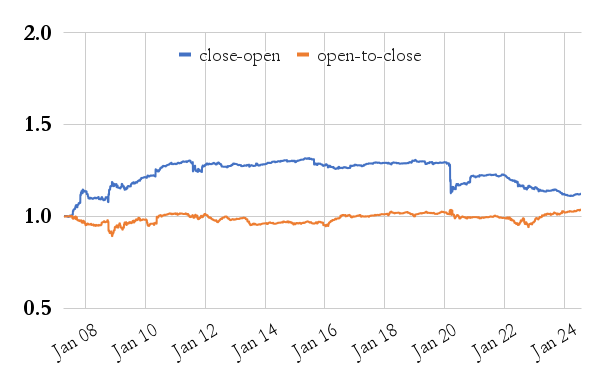

Then, it’s possible to test for an overnight anomaly; we compared close-to-open performance and open-to-close performance:

As we can see, HYG fares the best during the overnight sessions (from close to open), earning even higher returns than buy-and-hold. Conversely, daily sessions (from open to close) hurt and do not contribute towards the asset’s gains and appreciation at all. We can easily see the strength of the overnight effect in HYG in comparison to SPY (we investigated overnight and intraday effects last week in the Lunch Effect in the U.S. Stock Market Indices). While the overnight effect in stock market indexes is slowly losing its strength, quick analysis shows that in high-yield bonds, it is alive and well.

The next question is this: is there any way to decrease trading frequency and find a way to improve performance or return-to-risk ratios as well?

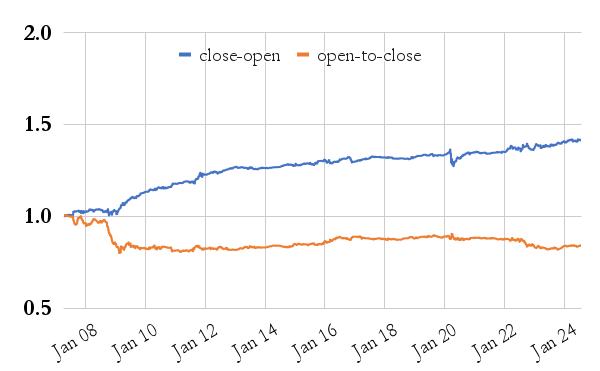

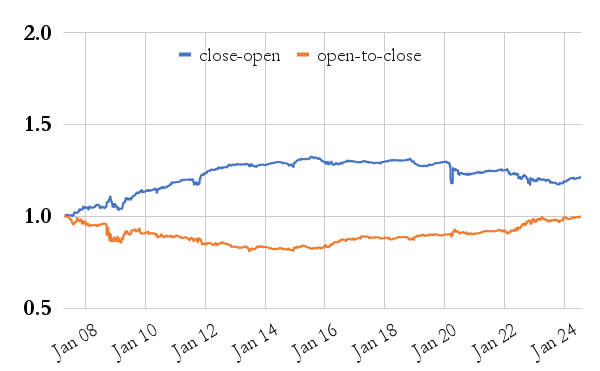

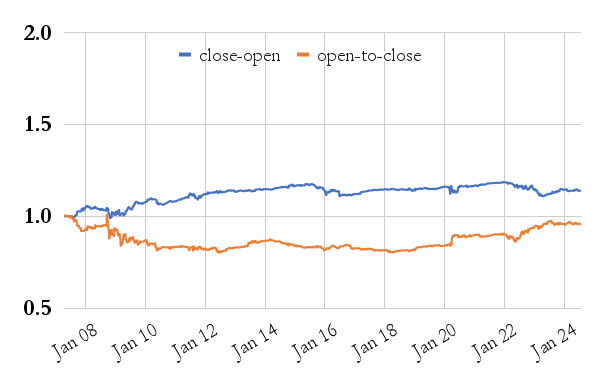

Our next try was to understand what’s the impact of the weekday on the anomaly’s performance. In the next series of charts, we will go and review the Overnight Effect on individual days – Monday (daily session: Monday from open to Monday to close; nightly session: from Monday Close to Tuesday open), and similarly Tuesday, Wednesday, Thursday, and Friday, and see how their overnight effect separately plays out:

Monday:

Tuesday:

Wednesday:

Thursday:

Friday:

This is the table of performance of nightly (overnight) sessions divided by individual (separate) days:

On Monday, the spread between daily and nightly sessions is most apparent, slowly dissipating towards the weekend when it is small compared to earlier days.

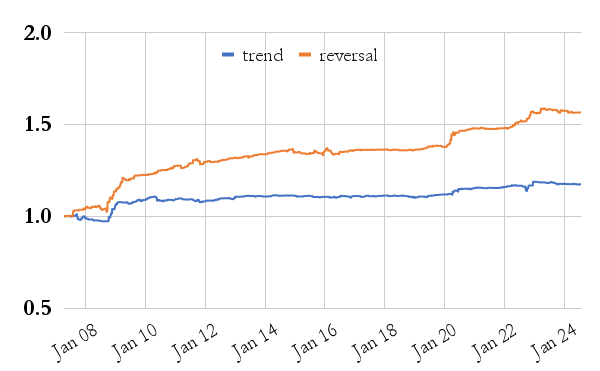

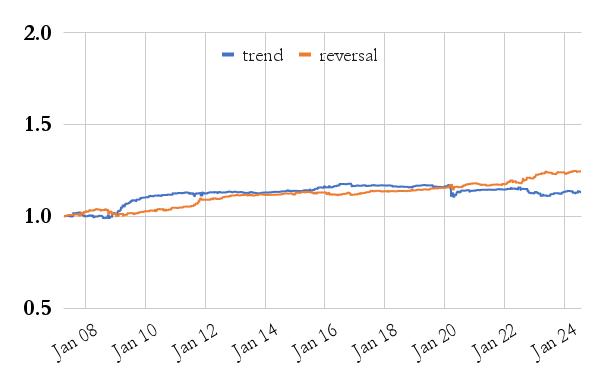

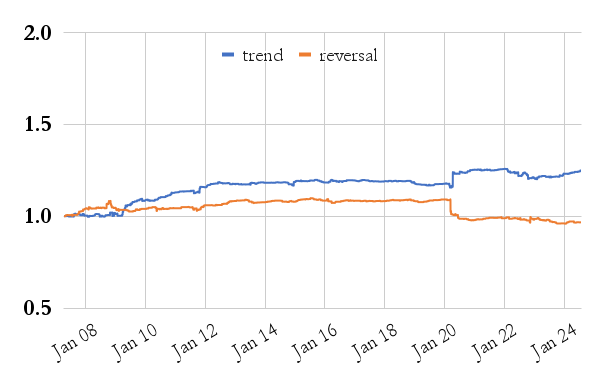

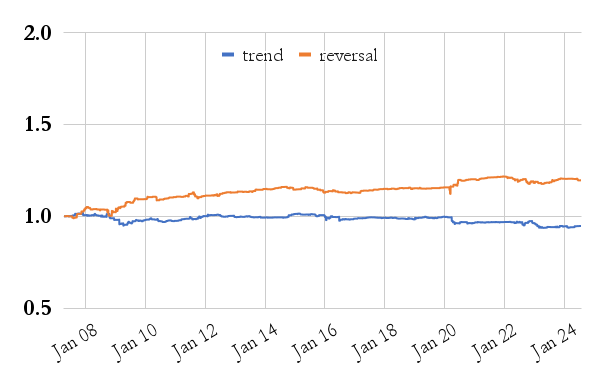

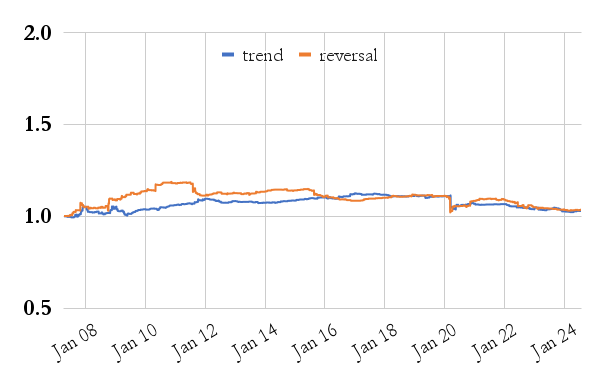

We guessed that this effect would be even amplified if we condition it on what happened the trading day before. So the last thing we tried is to compare trend vs. reversal; hence thus, what is the influence of the previous daily (close-to-close) session on the nightly (overnight) session; let us take a look at day-by-day results again, similarly to the previous series of charts:

Monday:

Tuesday:

Wednesday:

Thursday:

Friday:

The results are persistent and apparent. Most significant is the nightly reversal in the session from Monday’s close into Tuesday’s open if the close from Friday to Monday’s close was negative.

But wait, that’s a well-known anomaly in the stock market, too …

Yes, it’s the Turnaround Tuesday stock market indices trading strategy, which leverages the observed market anomaly, where price reversals frequently occur from the close of Monday’s trading session to the open of Tuesday’s session. This strategy capitalizes on mean reversion principles, particularly after a weak Monday, when the close is significantly lower than Friday’s.

So, at the end, we have the same pattern also in high-yield bonds. So, let us therefore look on its performance and return-to-risk ratios.

The advantage of not trading each nightly session in HYG ETF, but just the Turnaround Tuesdays is that strategy is giving us a better win-to-loss ratio, lower turnover, saves fees, and is freeing capital for other days when the other strategies have a better chance of profiting.

Conclusions

We are happy to accept our hypothesis that the high-yield market also offers interesting seasonal anomalies, especially numerous variations of the Overnight Effect. While this area of capital markets is slightly under-researched (if we compare it to the stock markets), we believe we contributed to finding some interesting similarities between stock and debt markets and that some anomalies tend to be universal and work well across asset classes.

Author: Cyril Dujava, Quant Analyst, Quantpedia

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend