Short Sellers: Informed Liquidity Suppliers

Short sellers often have a bad reputation, seen as market disruptors who profit from declining prices. Yet, they play a crucial role in making markets more efficient by identifying overvalued assets and correcting mispricings. A recent study uncovers another surprising aspect of their behavior: rather than just demanding liquidity, the most informed short sellers actually provide it. Using transaction-level data, the research shows that these traders supply liquidity, especially on news days and when trading on known anomalies, challenging the conventional view of short sellers as merely aggressive market participants.

For an ordinary person, investing has the prospect of buying steady and financially sound companies that tend to do well in the future, return their shareholders part of the profit, and thus benefit them in the long-term with compounding returns and whole society with the ethical allocation of capital for improving the world. With the advent of ETFs (exchange-traded funds), purchasing companies’ baskets grouped on various metrics based on typical signs and indicators such as regional or country location or identical or similar industry sectors is possible, which makes diversification even easier.

On the other hand, short-selling is a promising and lucrative endeavor that attracts risk-seeking traders, often inexperienced, who get burnt by not understanding the prospect of liquidity supply and demand mechanics. There are many scenarios and examples from the history of painful short squeezes (Volkswagen and GameStop) that made, at that moment, the right side profitable and wealthy, and, on the other side, limits-to-arbitrage scenarios where you, even if you wanted to either cover your short or buy wrongly valued asset, just could not because there were no shares to obtain. Bill Ackman shorting Herbalife, other activist investors, or a neverending myriad of Tesla shorters know their stories. However, there are also short-only hedge funds that specialize in, for example, deep delve into Phases I, II, and III of clinical trials and/or reasonably bet on not clearing FDA drug approval and can estimate failure rates to the extent that they can, based on an educated guess, take short positions on biotechs that are likely not to succeed in the long run.

Hard to argue that short-sellers are a vital part of free markets, which contribute to price discovery and the convergence process to accurate asset pricing valuations. Not surprisingly, such a feat, which includes unlimited losses (you eventually once need to cover your short positions), is warned against the ordinary investor, and informed trading performed by professional investors has an advantage at their feet.

Today, we confront common preconceptions about the short-selling with an interesting research paper that gives honoring nods toward short-sellers: Essentially, the abstract states that the most experienced short sellers act as liquidity providers rather than takers, which is a novel point that casts short sellers in a more favorable light. On the other hand, contributing to better price discovery by supplying better bid-ask spreads (posting and maintaining a lively order book, not aggressively hitting the market orders) helps ordinary investors establish or get out of their position at favorable prices than in other illiquid environments.

By distinguishing between liquidity-supplying and liquidity-demanding short sales, research paper challenges the conventional wisdom that only those demanding liquidity are informed. Liquidity-supplying short sellers are, in fact, better at predicting future stock returns, particularly over more extended holding periods. The study aligns with recent theoretical work that posits a dual role for informed traders, including liquidity provision to capitalize on long-lived information. The fact that the same short sellers supply liquidity and improve market efficiency adds to an already challenging task for regulators.

Stealthy Shorts: Informed Liquidity Supply paper shows that short sellers who trade in the direction of their information, which presumably affects prices, do so through liquidity-providing trades. The results, which show they are the same, add to the challenge faced by regulators who want to prevent adverse price movements while ensuring that markets are as liquid as possible, especially in times of crisis.

The paper begins the analysis by replicating a well-documented pattern in the cross-section of stock returns: stocks with a high short sale volume relative to their total trading volume underperform those with a low shot volume ratio). More importantly, authors uncover interesting heterogeneous patterns when decomposing this ratio into liquidity-supplying short volume ratio (LSS) and liquidity-demanding short volume ratio (LDS). Contrary to conventional wisdom, their portfolio analysis shows that only LSS negatively predicts future equity returns.

In particular, stocks in the highest LSS quintile underperform those in the lowest quintile by a risk-adjusted return of 38 basis points over a 21-day holding period. In contrast, the predictive power of LDS over the same holding period is much weaker at just 12 basis points, which is statistically indistinguishable from zero and driven entirely by the return on the day after portfolio formation. Cross-sectional regressions show that the return predictability associated with LSS is not subsumed when controlling for other well-known short-selling metrics and standard return predictors.

This suggests that liquidity-supplying short sales contain unique information about future stock returns. In additional tests, authors find that documented predictability is neither concentrated in stocks with specific characteristics nor driven by particular periods or samples of stocks, and it holds for various alternative holding periods. Final results indicate strong predictability of future returns from liquidity-supplying short sales. In contrast, such predictability is absent for liquidity-demanding short sales over holding periods longer than one day. Liquidity-supplying short sales may represent informed trading by short sellers with relatively long-lived information.

Authors: Amit Goyal, Adam V. Reed, Esad Smajlbegovic, and Amar Soebhag

Title: Stealthy Shorts: Informed Liquidity Supply

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4941397

Abstract:

Short sellers are widely known to be informed, which would typically suggest that they demand liquidity. We obtain comprehensive transaction-level data to decompose daily short volume into liquidity-demanding and liquidity-supplying components. Contrary to conventional wisdom, we show that the most informed short sellers are actually liquidity suppliers, not liquidity demanders. They are particularly informative about future returns on news days and trade on prominent cross-sectional return anomalies. Our analysis suggests that market making and opportunistic risk-bearing are unlikely to explain these findings. Instead, our results align with recent market microstructure theory, pointing to strategic liquidity provision by informed traders.

As always, we present several exciting figures and tables:

Notable quotations from the academic research paper:

“[Authors] shed further light on the nature of the return predictability and its link to the informational advantage inherent in liquidity-supplying short sales. First, we use a framework similar to that of Engelberg, Reed, and Ringgenberg (2012), and examine the predictive power of LSS for stock returns around firm-specific news release days. If the predictive ability of liquidity-supplying short sales stems from an informational advantage, then LSS should predict returns particularly on those days when news is released and information is incorporated into stock prices. Consistent with this hypothesis, we find that liquiditysupplying short sales are particularly informative about future returns on news days compared to non-news days. Additionally, as with our decomposition method, we demonstrate that this increased predictive power is present exclusively in the residual component of LSS, further supporting the notion that liquidity-supplying shorts are, on average, informed about company fundamentals.

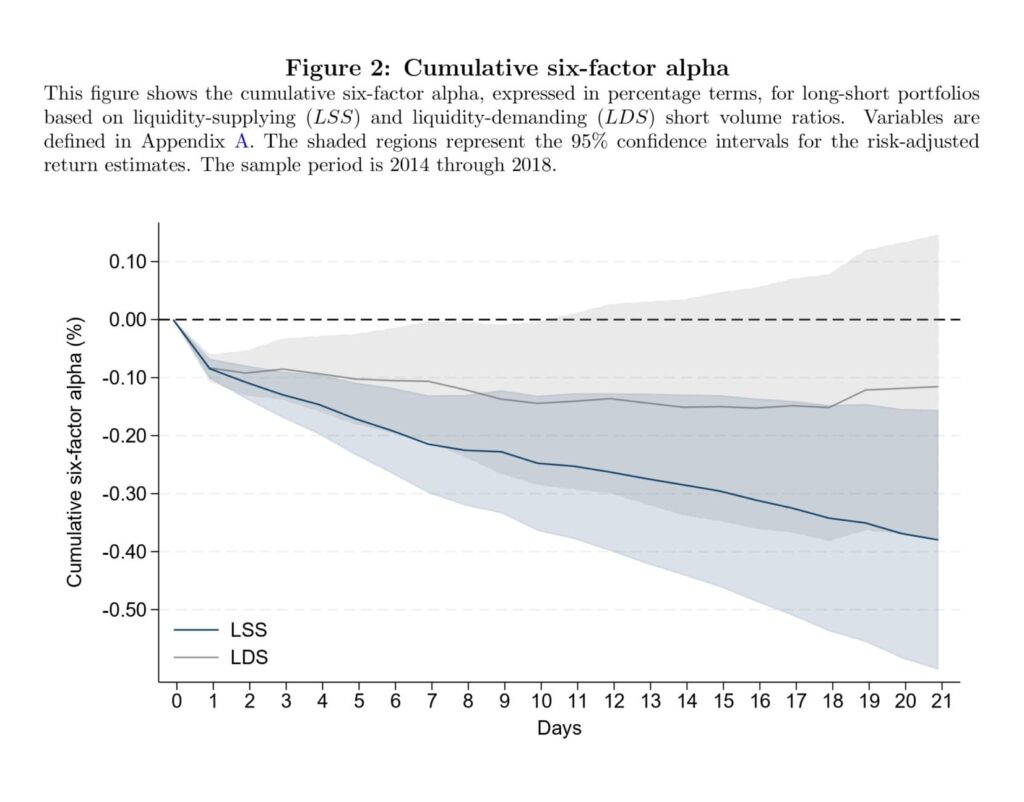

[Authors] report cumulative six-factor alphas for spread portfolios formed based on sorts of LSS or LDS for future horizons varying from 1 through 21 days in Figure 2. Consistent with prior literature (see, e.g., Boehmer, Jones, and Zhang, 2008 and Engelberg, Reed, and Ringgenberg, 2012), we find that both LSS and LDS significantly and negatively predict next day t return, with daily six-factor alphas of around 0.10%. Increasing the holding period, we find that the predictive power of LDS weakens, with no statistically significant predictability after seven days. In contrast, we find that LSS is a strong negative predictor of future equity returns across all holding periods ranging from 1 through 21 days. For a 21-day holding period, the spread portfolio based on LSS has a cumulative six-factor alpha of almost 0.40%. Thus, this figure documents a striking empirical pattern: liquidity-supplying shorts negatively predict future equity returns, whereas liquidity-demanding shorts do not, at least for horizons of longer than a week.

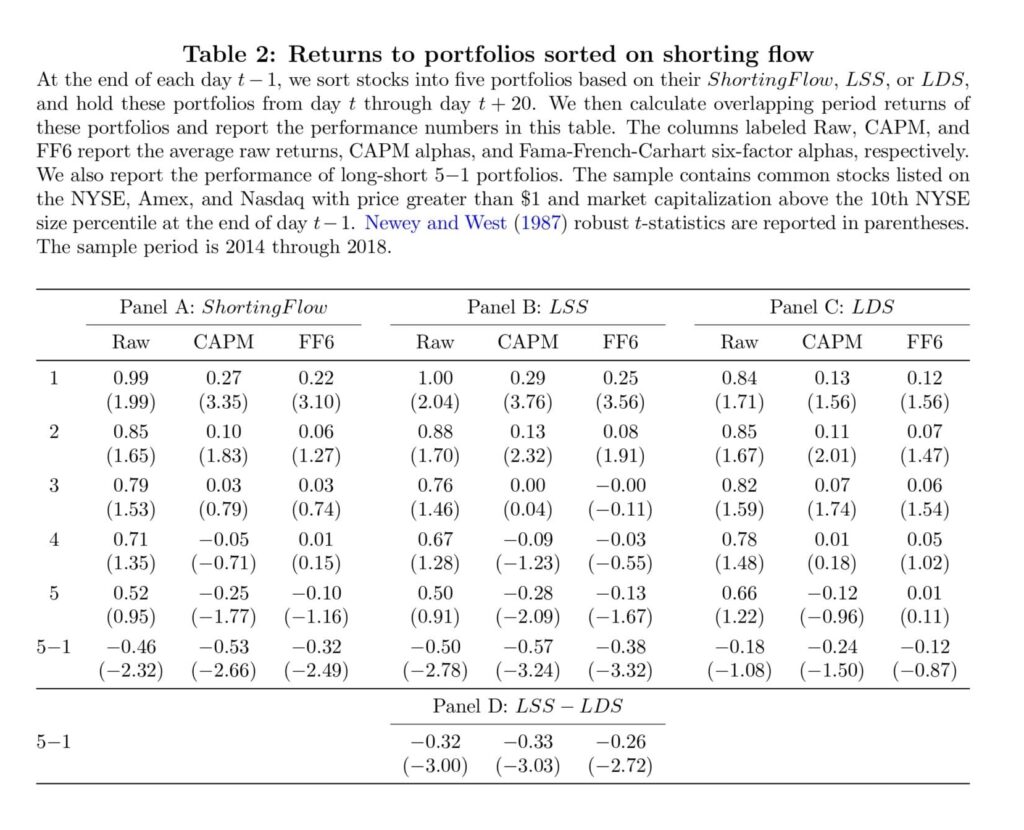

We present returns and alphas on quintile portfolios and the spread portfolio for a horizon of 21 days in Table 2. Panels A, B, and C sort on total ShortingF low, LSS, and LDS, respectively. Panel A shows that heavily shorted stocks underperform lightly shorted stocks. This finding is robust whether we look at raw returns or risk-adjusted returns and is statistically significant with t-statistics ranging from −2.32 to −2.66. Consistent with prior literature (see, e.g., Boehmer, Jones, and Zhang, 2008), we find that the performance difference between portfolios 1 and 5 is driven primarily by the outperformance of quintile 1 rather than by the underperformance of quintile 5.

[Authors] find that, with hardly any exceptions, the coefficient on LSS is negative and statistically significant while that on LDS is statistically insignificantly different from zero.13 The results are similar across two subsamples (rows (2) and (3)), for different filters on stocks (rows (4) through (6)) and for different horizons of future returns (rows (7) through (9)). Row (9) in particular shows that the predictability extends to 40 days. Thus our results are not driven by specific time periods, specific samples of stocks, or particular calculations of variables.

Overall, the results of this section show a strong predictability of future returns associated with liquidity-supplying short sales but the absence of such predictability associated with liquidity-demanding short sales. These results suggest that liquidity-supplying short sales may represent informed trading from investors with relatively long-lived information.

[R]esults [] indicate that the predictive power of short sales for the cross-section of equity returns stems from informed liquidity provision by short sellers. Moreover, the graphical representation of the return predictability for varying holding periods in Figure 2 suggests that these short sales trade on information that is slowly incorporated into stock prices.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend