A Few Tips for Volatility Trading

A new financial research paper related to volatility selling strategies:

Authors: Sepp

Title: Gaining the Alpha Advantage in Volatility Trading

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3032098

Abstract:

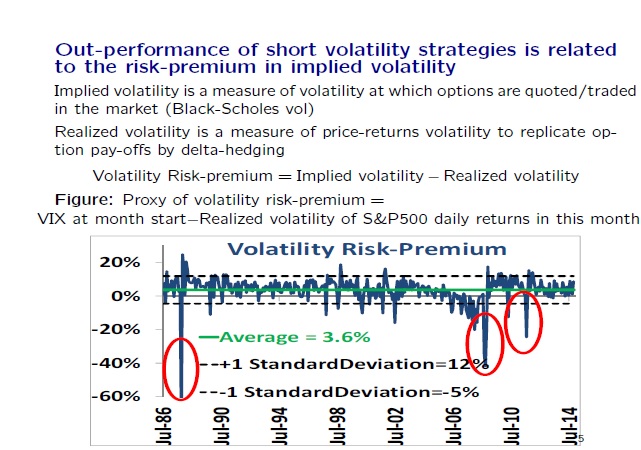

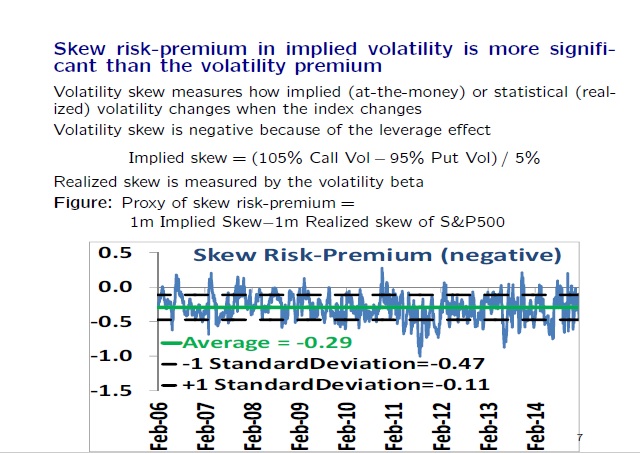

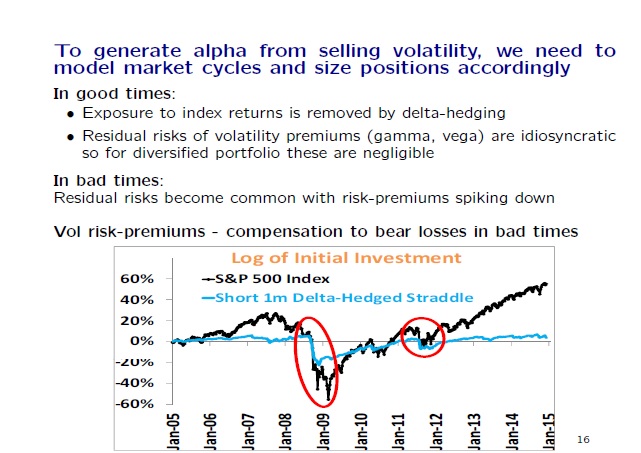

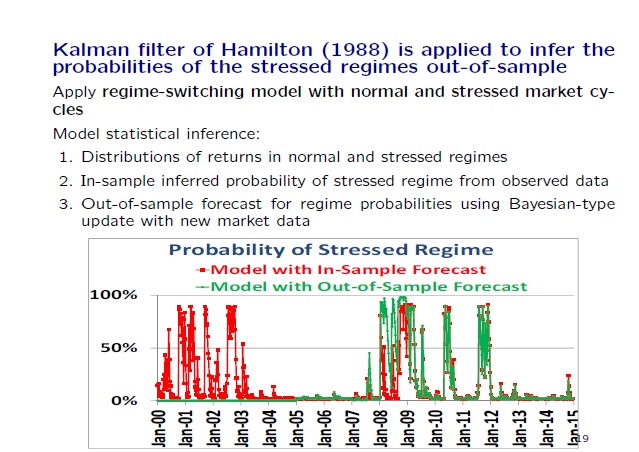

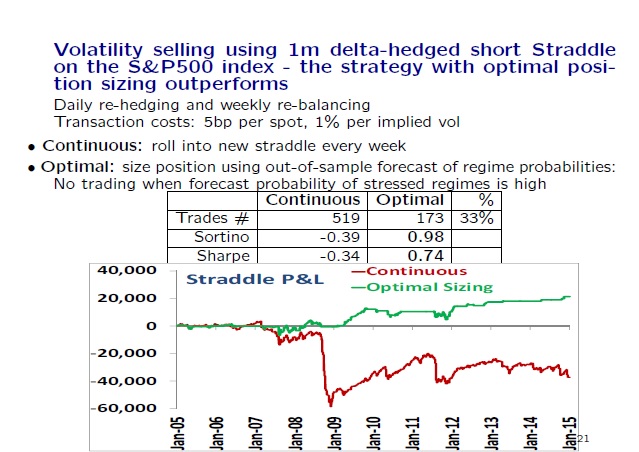

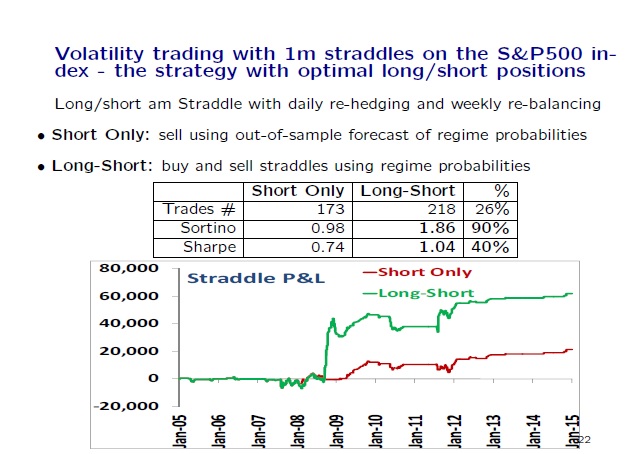

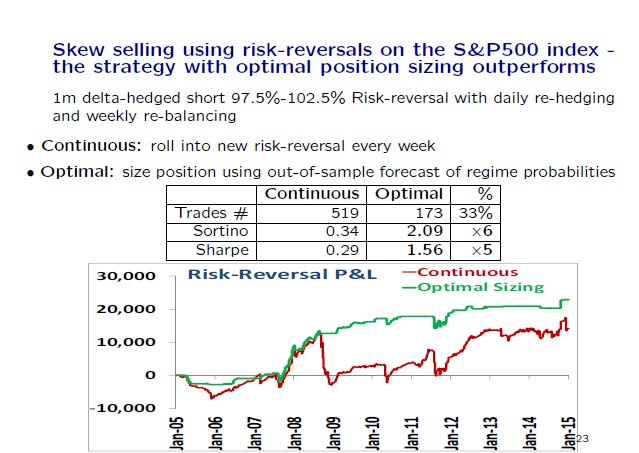

We present some empirical evidence for short volatility strategies and for the cyclical pattern of their P&L. The cyclical pattern of the short volatility strategies produces an alpha in good times but collapses to the beta in bad times. We introduce a factor model with risk-aversion to explain the risk-premium of short volatility strategies as a compensation to bear losses in bad market regimes. We then consider an econometric model for statistical inference of market regimes and for optimal position sizing. Finally, we illustrate model applications for generating alpha from volatility strategies.

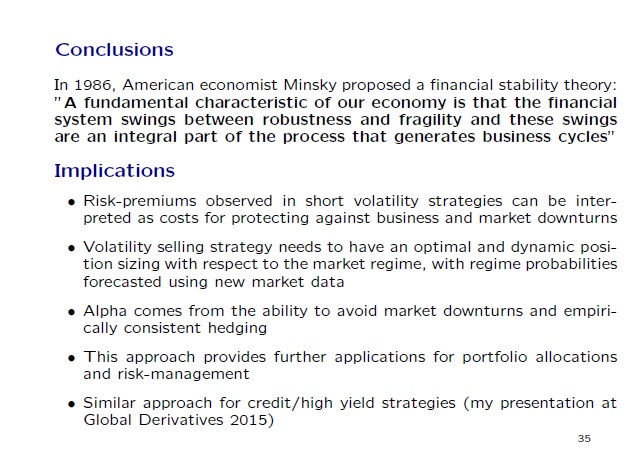

Notable presentation slides from the academic research paper:

"

"

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend