Understanding seasonality in financial markets requires recognizing how predictable return patterns can be influenced by investor behavior. One underexplored aspect of this is the impact of front-running—where traders anticipate seasonal trends and act early, shifting returns forward in time. We have already explored seasonality front-running in commodities, stock sectors, and crisis hedge portfolios. Our new research examines whether this phenomenon extends to country ETFs, an asset class where seasonality has been less studied. By applying a front-running strategy to a dataset of country ETFs, we identify opportunities to capitalize on seasonal effects before they fully materialize. Our findings indicate that pre-seasonality drift is strongest in commodities but remains present in country ETFs, offering a potential edge in portfolio construction. Ultimately, our study highlights how front-running seasonality can enhance ETF investing, providing an additional layer of market timing beyond traditional trend-following approaches.

Introduction

Seasonality is a well-documented phenomenon in financial markets, where certain assets exhibit recurring patterns in returns based on time-based factors such as months, quarters, or economic cycles. It commonly appears in commodity markets (Trader’s Guide to Front-Running Commodity Seasonality), stock sectors (Front-Running Seasonality in US Stock Sectors) or crisis hedge portfolios (Seasonality Patterns in the Crisis Hedge Portfolios).

Once tradable assets become available, they are subject to front running—investors anticipating seasonal trends begin accumulating positions before the expected seasonality manifests. This front running effect can create price drifts, shifting returns forward in time and potentially diminishing or reshaping the original seasonal pattern. While not all assets experience this effect, it is far from rare. Understanding these dynamics can help investors identify when and where seasonality is being priced in early, offering opportunities to capitalize on market inefficiencies.

In this study, we investigate whether this phenomenon extends to another segment of the market—market ETFs. We examine the behavior of these ETFs with a focus on seasonality and, following the approach of the previously mentioned studies, aim to construct a front-running strategy that effectively leverages seasonal patterns.

Data

In this analysis, our dataset consist of monthly data from 23 country ETFs, specifically: SPY – SPDR S&P 500 ETF Trust, EWU – iShares MSCI United Kingdom ETF, EWG – iShares MSCI Germany ETF, EWQ – iShares MSCI France ETF, EWI – iShares MSCI Italy ETF, EWD – iShares MSCI Sweden ETF, EWN – iShares MSCI Netherlands ETF, EWP – iShares MSCI Spain ETF, EWK – iShares MSCI Belgium ETF, EWL – iShares MSCI Switzerland ETF, EWC – iShares MSCI Canada ETF, EWJ – iShares MSCI Japan ETF, EWW – iShares MSCI Mexico ETF, EWM – iShares MSCI Malaysia ETF, EWA – iShares MSCI Australia ETF, EWS – iShares MSCI Singapore ETF, EWY – iShares MSCI South Korea ETF, EWT – iShares MSCI Taiwan ETF, EWZ – iShares MSCI Brazil ETF, EWH – iShares MSCI Hong Kong ETF, EZA – iShares MSCI South Africa ETF, FXI – iShares China Large-Cap ETF, and INDY – iShares India 50 ETF.

Most of these ETFs were launched in 1996, the second largest group in 2000; therefore, after the year 2000, we have historical data for nearly all ETFs. Only EZA, FXI, and INDY were introduced later, in 2003, 2004, and 2009, respectively. To maximize the length of our research period, we did not wait until 2009. Instead, we used the year 2000 as the starting point for our analysis, and the last 3 ETFs were included gradually after their inception. In other words, we tried to make a trade-off between data availability and the number of ETFs in the initial portfolio. The most recent data used was from February 2025.

Monthly performance data were utilized in all calculations. Basic performance characteristics in tables are presented as follows: the notation perf represents the annual return of the strategy, st dev stands for the annual standard deviation, max dd is the maximum drawdown, adusted Sharpe Ratio is calculated as the ratio of perf to st dev and adjusted Calmar Ratio as the ratio of perf to max dd.

Methodology

As mentioned in the first paragraph, this study focuses on seasonality, which we aim to leverage in creating a profitable strategy. Given the availability of tradable assets, we believe front-running is a suitable approach. The procedure is straightforward – if we are confident that an asset performs well in a specific month, buying it one month earlier, before most investors do, can be more effective, as their later purchases drive the price higher.

And now, we can move on to the strategy itself. At the end of each month, we applied a cross-sectional approach to seasonality, ranking the performance of all included ETFs based on their returns from the month T-11 (e.g., at the end of March, investments for April were ranked based on their performance in May of the previous year). This ranking was conducted relative to the other ETFs in the selection. Based on these rankings, we invested in a selected number of top-performing ETFs for the following month.

But how many ETFs should we include in our portfolio? We decided to rely on acquired knowledge, and for robustness purposes, we included all significant picks. Therefore, we tested multiple thresholds: vigintile (top 5%), decile (top 10%), quintile (top 20%), quartile (top 25%), tercile (top 33%), and half (50%). This means we applied the front-running strategy to the top 1 to 11 ranked investments.

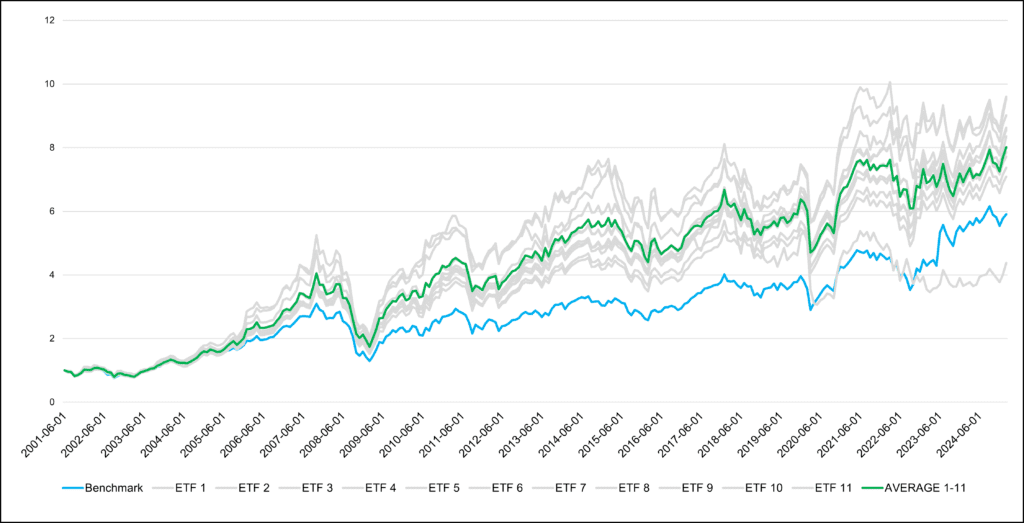

In the next step, we constructed a benchmark – an equally weighted average of all 23 ETFs. Additionally, we included an equally weighted average of the 11 front-running strategies, selecting the top 1 to 11 ETFs with the highest performance in the front-running months. Now, we are finally ready to assess the profitability of our strategy.

As we can see in the graph in Figure 1, for almost the entire period, nearly all front-running strategies and their average outperformed the benchmark. There is one exception: the front-running strategy, which selects only 1 ETF, which has experienced a significant downturn since 2019. All other strategies, and thus the average 1-11, easily outperformed the benchmark.

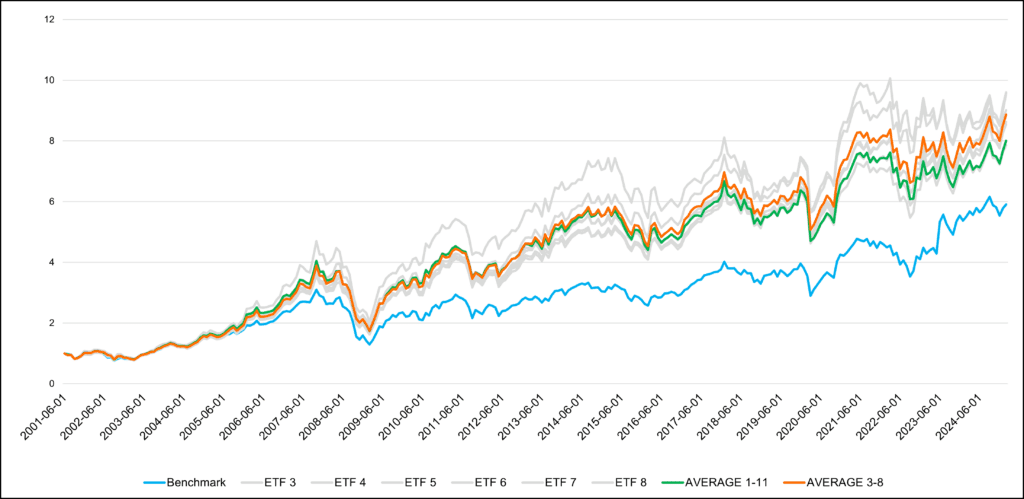

However, strategies placed in the middle of our tested sample achieved the most favorable results. It seems that it’s not a good idea to be too concentrated (picking just the 1 or 2 ETFs). It’s also not a good idea to be overly diversified (as the front-running signal is then too diluted among too many ETFs). The sweet spot is to pick between 3-8 ETFs (so the top quintile, quartile, or tercile of ETFs based on the front-running seasonality signal). So, in the next step, we retained only the strategies based on the top 3 to top 8 ETFs and averaged them out to build a final front-running strategy. Let’s assess whether we made the right decision.

As expected, the shortened selection easily outperformed not only the benchmark but also the broader average. Therefore, we recommend adopting the average of shortened selection as the final strategy, similar to our approach in the study Can Margin Debt Help Predict SPY’s Growth & Bear Markets?. We consider the slightly higher results of some strategies to have low credibility and to be unlikely to persist in the long run. Due to the mean reversion effect, we favor diversifying our bets across all strategies to maintain a more stable model. The final decision, of course, remains with the reader.

Conclusion

The strength of the pre-seasonality drift depends on the underlying assets. We observe that it is strongest in commodities, where we first identified it. While the effect is present in other asset classes, it is weaker due to the dominance of other fundamental factors. For example, in equities, the overall strong positive drift plays a major role, as stocks tend to rise on average, whereas commodities do not exhibit the same long-term upward trend. Despite this, we have found a way to enhance investment strategies in country ETFs by implementing an approach that evenly allocates capital across six front-running strategies, selecting 3 to 8 ETFs based on the front-running seasonality signal each month. This demonstrates that the front-running seasonality concept remains applicable beyond commodities.

Author: Sona Beluska, Junior Quant Analyst, Quantpedia

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend