How to Improve Commodity Momentum Using Intra-Market Correlation

Momentum is one of the most researched market anomalies, well-known and widely accepted in both public and academic sectors. Its concept is straightforward: buy an asset when its price rises and sell it when it falls. The goal is to take advantage of these trends to achieve better returns than a simple buy-and-hold strategy. Unfortunately, over the last decades, we have been observers of the diminishing returns of the momentum strategies in all asset classes. In this article, we will present an intra-market correlation filter that can help significantly improve commodity momentum performance and return this strategy once again into the spotlight.

While early momentum research primarily focused on stocks, similar patterns have been identified across various asset classes. For instance, our Quantpedia Screener lists a momentum strategy specifically for commodity futures. The strategy involves ranking the commodity futures by performance over the past 12 months and dividing them into quintiles. The top-performing quintile is bought, and the bottom-performing quintile is sold, with rebalancing taking place each month.

In Quantpedia’s research titled “What’s the Best Factor for High Inflation Periods?“, the momentum effect was found to be positive during periods of high inflation around World War II and the Oil Crisis of 1973. However, in recent years, the performance of momentum strategies has declined. Momentum has struggled to effectively distinguish between winners and losers in homogeneous investment universes, as thoroughly analyzed in the recent Quantpedia research paper titled “Robustness Testing of Country and Asset ETF Momentum Strategies”. The findings suggest that momentum strategies perform better in asset-based ETFs than in country-based ETFs due to the lower correlation between assets.

Building on these insights, this paper aims to address the recent decline in momentum efficacy by exploring how to implement momentum in homogeneous commodity ETFs, rather than commodity futures. First, we test a basic momentum strategy, which does not produce significant alpha. Next, we improve the basic strategy by using the ratio of short-term to long-term average correlations as a signal for when it is favorable to apply momentum strategies, yielding promising results. We propose a strategy based on this intra-market correlation filter.

Methodology and Data

For this analysis, we chose sector commodity ETFs due to their ease of use, length of data, accessibility, and no need for complex rolling procedures. The strategy focuses on four sector-specific commodity ETFs: DBA (agriculture), DBB (base metals), DBE (energy), and DBP (precious metals). These ETFs offer a longer backtesting period, starting from 2007, compared to individual commodity ETFs. Data were sourced from Yahoo Finance, using the adjusted close prices (adjusted for stock splits, dividend distributions, and other relevant events affecting stock’s value) for the selected ETFs. From the daily data, we calculated both daily and monthly performance.

Data source

Recently, Yahoo Finance discontinued free end-of-day data downloads. As a result, we recommend sourcing data from our preferred provider, EODHD.com – the sponsor of our blog. EODHD offers seamless access to +30 years of historical prices and fundamental data for stocks, ETFs, forex, and cryptocurrencies across 60+ exchanges, available via API or no-code add-ons for Excel and Google Sheets. As a special offer, our blog readers can enjoy an exclusive 30% discount on premium EODHD plans.

Step 1

The first step was to replicate a simple momentum strategy using the four ETFs (DBA, DBB, DBE, and DBP). Each month, we calculated the 1- to 12-month momentum for each ETF and ranked them based on their performance. This ranking provided the signals for which ETFs to go long and which to short. The strategy involved going long on the two best-performing ETFs and short on the two worst-performing ones mimicking the basic premise of momentum that winners will continue to outperform and losers will continue to underperform. The portfolio was equally weighted and rebalanced on a monthly basis.

Results of step 1

Table 1 simple momentum characteristics

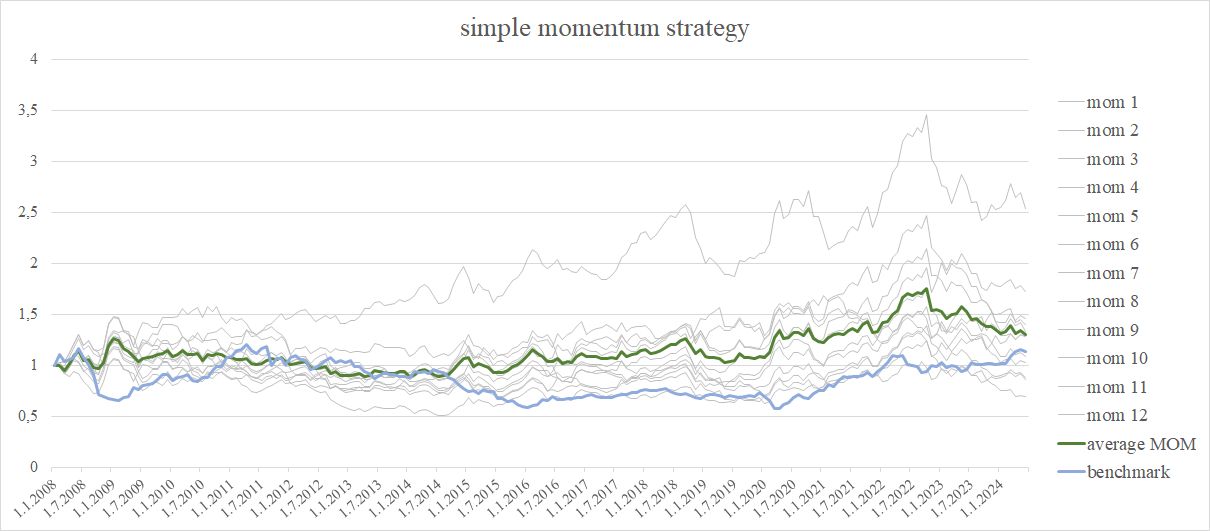

Figure 1 simple momentum strategy

As expected, the momentum strategy on commodities yielded poor performance. Table 1 shows that while it slightly outperforms the benchmark return, this comes at the cost of higher volatility. This outcome aligns with previous research, including research by Quantpedia. In homogeneous markets like commodities, where assets are highly correlated, momentum struggles to effectively differentiate between winners and losers, leading to disappointing performance.

One potential way to improve performance of momentum strategies in commodity ETFs is by turning to low-liquidity assets. In one of Quantpedia’s previous studies “How to Use Exotic Assets to Improve Your Trading Strategy”, the authors examined the illiquidity premium—the idea that expected returns increase with illiquidity—by running a set of momentum strategies using commodity futures contracts from two leading commodity indices, S&P GSCI and BCOM. The results showed that non-indexed, or exotic, low-liquidity assets outperformed indexed ones, offering higher returns with nearly the same risk as indexed commodity strategies.

Step 2

While turning to low-liquidity assets was one option, we decided to explore alternative ways to make momentum strategies work effectively in commodity ETFs. Our goal was to find a reliable predictor that could signal when it’s favorable to apply a momentum strategy and when it’s not. We soon discovered that the ratio of short-term to long-term correlation could serve as such a predictor.

The next step in our analysis involved calculating average short-term (measured over 20 days) and aveage long-term (measured over 250 days) correlations from the daily performance of the four ETFs. If the average short-term correlation exceeds the average long-term correlation between ETFs, it indicates that commodities are trending in one direction, allowing momentum strategies to more effectively distinguish between winners and losers. Deploying momentum under these conditions can therefore be more profitable. In summary, correlation filter enables us to apply the momentum strategy selectively, using it only when market conditions are favorable.

Results of step 2

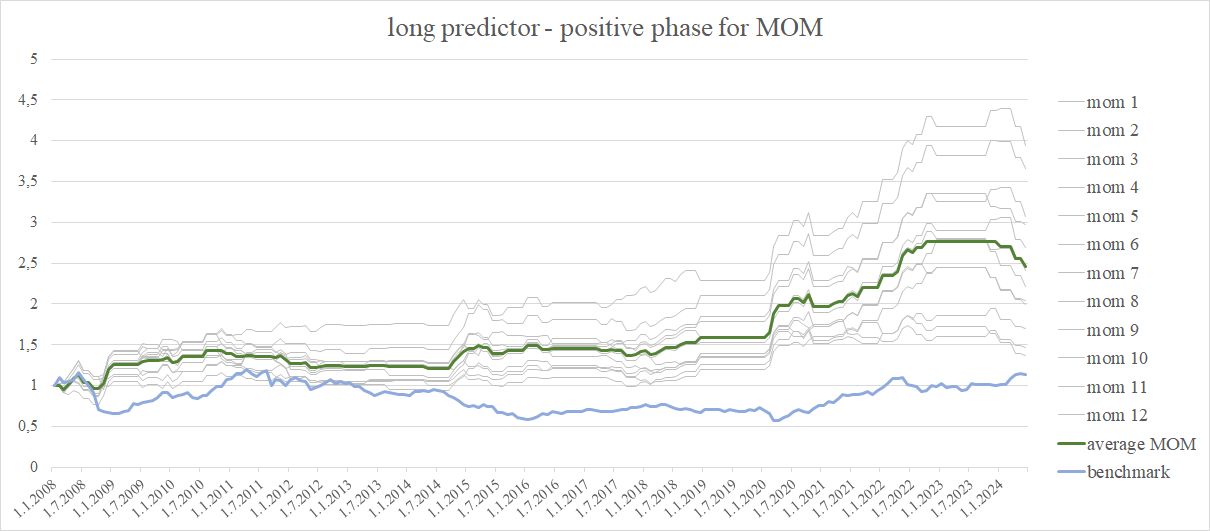

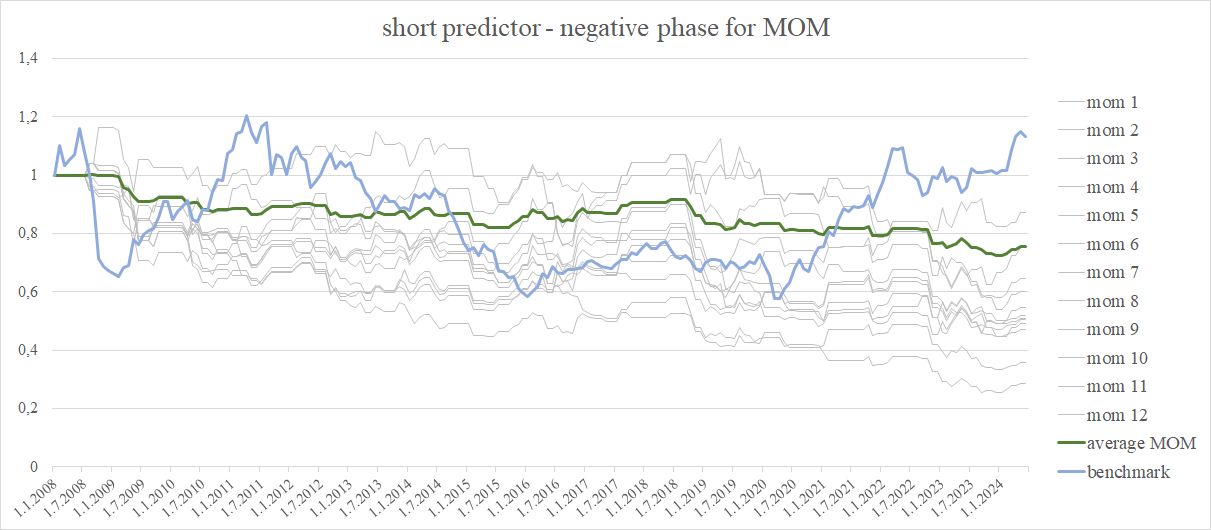

As shown in Table 2, the correlation predictor leads to more pleasing outcomes compared to the basic momentum strategy. It outperforms the momentum strategy across all performance metrics, including annual returns, volatility, maximum drawdown, Sharpe ratio, and Calmar ratio. The correlation filter appears to be quite robust. Regardless of the momentum ranking period (1-12 months), the filter reliably identifies when it is appropriate to trade the momentum strategy (figure & table 2) and when it is more suitable to trade the reversal effect as the momentum strategy consistently yields negative results (figure & table 3).

Table 2 long predictor characteristics

Figure 2 long predictor

Table 3 short predictor characteristics

Figure 3 short predictor

Step 3

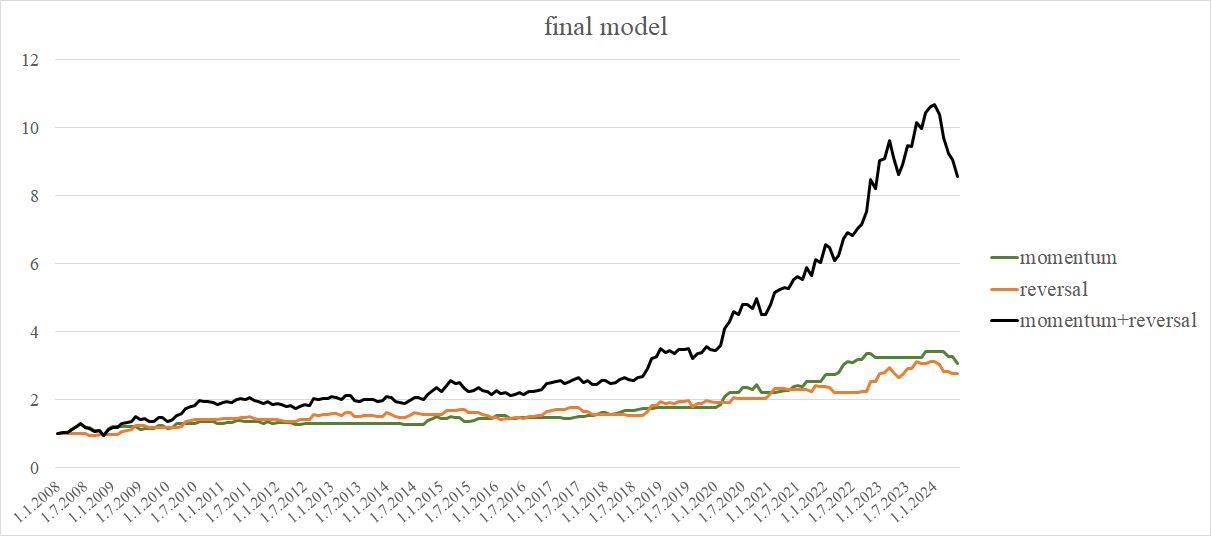

The insights gained from this research open the door for the development of new, exciting strategies. Based on these findings and existing literature, we propose the following strategy using a correlation filter: if the short-term correlation is higher than the long-term correlation, apply the momentum strategy by going long on the 2 best-performing and short on the 2 worst-performing sector commodity ETFs, based on a 12-month ranking, and hold the positions for 1 month. If the short-term correlation is lower than the long-term correlation, apply a reversal strategy by going long on the 2 worst-performing and short on the 2 best-performing sector commodity ETFs (based on a 12-month ranking), and hold the positions for 1 month. As shown in Figure 4 and supported by the results in Table 4, this combined strategy (Mom+Rev) nearly doubles the return of either the standalone momentum or reversal strategies. Although the higher volatility and maximum drawdown suggest an increased level of risk, this may be justified by the significantly higher returns.

Table 4 suggested strategy characteristics

Figure 4 suggested strategy

Conclusion

In this paper, we addressed the challenges of momentum in homogeneous markets like commodities using widely available sector commodity ETFs.

In summary, while a basic momentum strategy applied to commodities yields disappointing results, incorporating a predictor based on intra-market correlation significantly enhances momentum strategy’s performance. This ratio between 20-day and 250-day correlation provides a reliable signal identifying when commodities are trending strongly enough for momentum to distinguish between winners and losers.

Author: Margareta Pauchlyova, Quant Analyst, Quantpedia

References

Quantpedia. (n.d.). Momentum effect in commodities. Retrieved September 1, 2024, from https://quantpedia.com/strategies/momentum-effect-in-commodities/

Quantpedia. (n.d.). What’s the best factor for high inflation periods? (Part II). Retrieved September 1, 2024, from https://quantpedia.com/whats-the-best-factor-for-high-inflation-periods-part-ii/

Du, Jiang and Vojtko, Radovan, Robustness Testing of Country and Asset ETF Momentum Strategies (March 25, 2023). Available at SSRN: https://ssrn.com/abstract=4736699 or http://dx.doi.org/10.2139/ssrn.4736699

Cisár, Dominik and Vojtko, Radovan, How to Use Exotic Assets for Trading Strategy Improvement (September 3, 2021). Available at SSRN: https://ssrn.com/abstract=3916918 or http://dx.doi.org/10.2139/ssrn.3916918

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend