Is Machine Learning Better in Prediction of Direction or Value?

Building machine learning models for trading is full of nuances, and one important but often overlooked question is: what exactly should we try to predict—the direction of the next market move or the actual value of the asset’s return? A recent paper by Cheng, Shang, and Zhao, titled “Direction is More Important than Speed“ offers a clear and practical answer. Their research shows that focusing on direction—simply whether returns will be positive or negative—leads to better model accuracy and, more importantly, stronger real-world investment performance. This is especially true when using machine learning methods, where predicting the direction allows models to better capture downside risks and build more effective trading strategies. For anyone using ML in finance, this paper makes a strong case that predicting where the market is headed is often more valuable than predicting how far it will go.

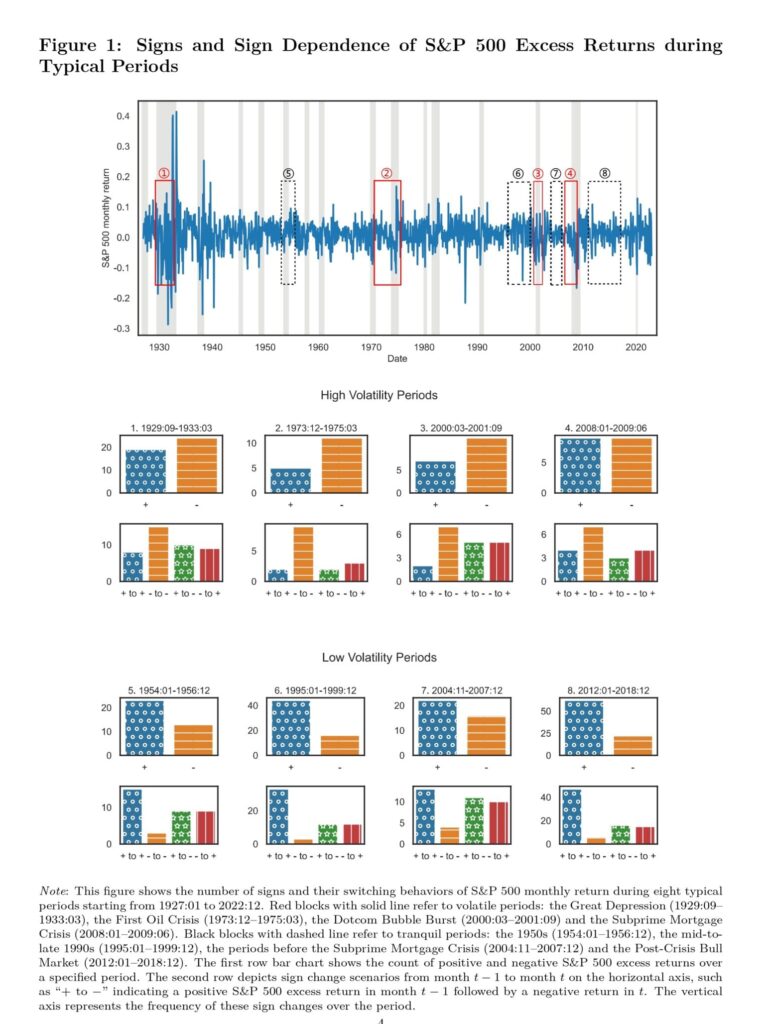

The authors ground their argument in both economic theory and empirical analysis. They show that direction prediction is not just a practical shortcut—it’s theoretically supported by mechanisms like the Campbell-Shiller identity and volatility clustering. For example, if valuation ratios such as the dividend-price ratio increase, theory suggests not only higher expected returns, but also a greater likelihood that the next return will be positive. The authors further argue that volatility itself carries predictive power: during high-volatility periods, markets tend to experience more negative returns, and vice versa. These insights justify treating direction as a standalone, meaningful forecasting target.

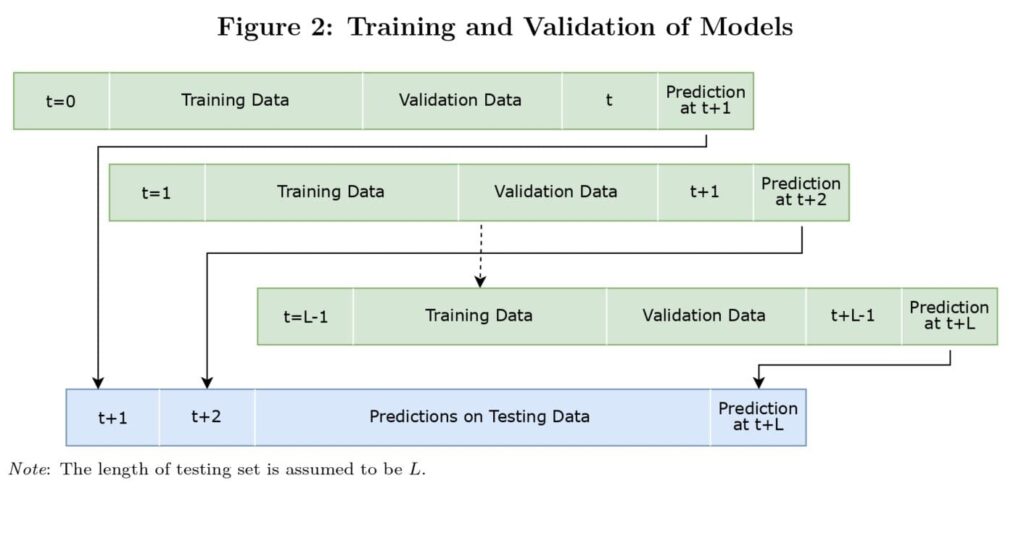

To test their hypothesis, the researchers compare a wide array of models—ranging from simple linear regressions to advanced machine learning techniques like Random Forests and Gradient Boosted Trees—across two tasks: predicting return value vs. predicting return direction. Using 26 well-known macroeconomic and technical indicators (such as dividend yields, interest rates, momentum signals, and volatility measures), they evaluate model performance on both statistical metrics (like accuracy and F1 score) and economic outcomes (such as utility gains and Sharpe ratios from trading strategies). Their results consistently show that direction-focused models outperform value-based ones, especially when it comes to building effective investment strategies.

Key takeway:

Direction prediction is more reliable and actionable than value prediction—especially when using machine learning—leading to stronger investment returns and better downside risk management.

Simple theoretical mechanisms like the Campbell-Shiller identity and volatility clustering provide a solid foundation for direction-based forecasting, reinforcing that this approach is not just statistically advantageous, but also economically intuitive.

Even with fewer input variables, direction models outperform value models, particularly after accounting for transaction costs—making them more practical for real-world trading strategy design.

Authors: Albert Bo Zhao, Tingting Cheng, Yitong Shang

Title: Direction is More Important than Speed: A Comparison of Direction and Value Prediction of Stock Excess Returns

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5176925

Abstract:

A major research topic in asset pricing is predicting the value of stock excess returns. We examine a seemingly simpler and yet less explored problem-predicting the direction. Theoretically, mechanisms such as the Campbell-Shiller identity and volatility clustering can support direction predictability. Using various established predictors from value prediction literature, we compare linear, regularized linear, machine learning, and combination models across both tasks. When shifting from value to direction prediction, models achieve higher accuracy and yield greater economic gains, mainly because of their stronger ability to predict market downturns. Consistent with the value prediction literature, machine learning and combination methods generally outperform simpler models in direction prediction as well. While most models perform better when incorporating the full set of predictors, direction prediction with a limited set of predictors can still rival value prediction using a comprehensive set of predictors. Moreover, blending value and direction strategies outperforms value strategies but does not surpass direction-only results. We also find that the returns of direction strategies can explain the returns of value strategies, but not vice versa.

As such, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“These preliminary analyses suggest that there is some degree of predictability in the sign of returns, which is partly linked to volatility clustering. The real world, involving a variety of influencing factors and diverse functional forms, is far more complex than the analysis here. Does logDP influence the sign of returns in the same way it affects return values? Can other variables identified in the value prediction literature also impact the sign of returns, and if so, how would they perform and in what forms? With these questions in mind, we aim to expand the theoretical framework by incorporating a broad set of factors, including commonly used predictors in the value prediction literature (Rapach and Zhou, 2013; Rapach, Strauss, and Zhou, 2010; Rapach and Zhou, 2020; Welch and Goyal, 2008).7 Additionally, we consider a wide range of models, from simple linear specifications to complex machine learning approaches, as well as combination models.

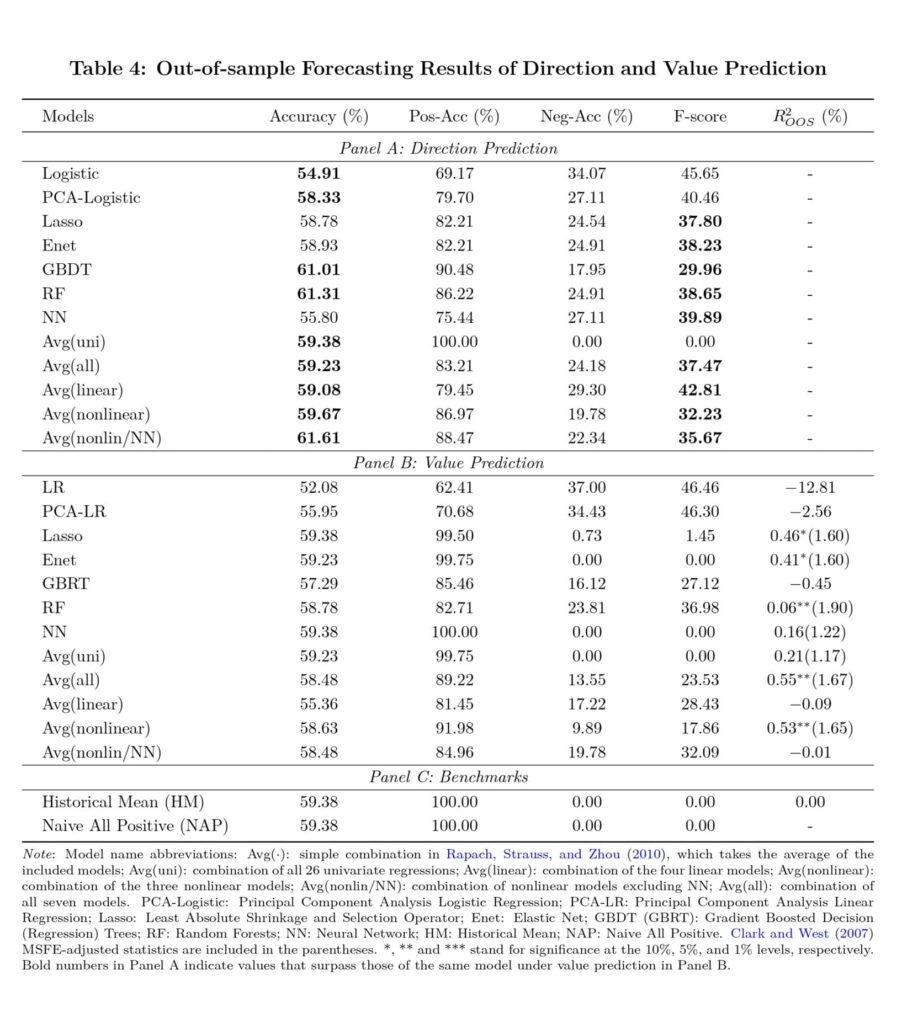

In almost all model comparisons, direction prediction models have a higher Accuracy than their corresponding value prediction models (Table 4). For example, Logistic Regression reports an Accuracy of 54.91, while Linear Regression reports 52.08; Random Forest’s Accuracy for direction prediction is 61.31, while for value prediction it is 58.78. The gap is more prominent when measured by F-score, which strikes a balance between predicting positive and negative returns. Lasso classification reports an F-score of 37.80, while its value prediction counterpart reports 1.45. The F-score of Random Forest increases from 36.98 to 38.65 when switching from value prediction to direction prediction. Even combination-based approaches, which have been widely proven to perform very well in value prediction (e.g. Rapach and Zhou, 2013; Rapach, Strauss, and Zhou, 2010; Zhao and Cheng, 2022), generally show better performances when applied to direction prediction. Further analysis reveals that the improved performance stems from enhanced accuracy in predicting negative returns, as most models struggle—some, such as Lasso and Enet, are particularly ineffective—when their objectives are tuned for value prediction. In other words, direction prediction demonstrates a stronger ability to capture downside risk in stocks.

The investment strategy evaluates the certainty equivalent return for an individual with a risk aversion coefficient of 3. For the value strategy, we follow the standard settings in the value prediction literature. For the direction strategy, we propose two approaches. In the first approach, a positive predicted return results in full allocation to stocks, while a negative prediction shifts the entire investment to the risk-free asset (Direction Strategy 1). In the second strategy, the weight in stocks is adjusted according to the predicted probability, with higher probabilities resulting in greater weights (Direction Strategy 2). When comparing models against the BH and HM benchmarks, only Enet, RF, and some combination methods outperform both BH and HM in both value and direction strategies under transaction costs. These results are consistent with the value prediction literature: improving predictive performance over HM requires either model combination or machine learning enhancements (e.g. Rapach, Strauss, and Zhou, 2010; Zhao and Cheng, 2022).

However, if all models are adjusted for direction prediction and incorporate predicted probabilities into stock weights (Direction Strategy 2), the vast majority of models (except Logistic and NN) generate significantly higher utility gains than the BH strategy (Table 6). When models of the same type are compared pairwise, direction strategies outperform value strategies in nearly all cases, regardless of whether Direction Strategy 1 or 2 is used (Table 7). This indicates that simply shifting the prediction target from value to direction improves performance.

First, we conduct an empirical comparison between the prediction of stock return direction and value, showing that direction is more predictable than value and also yields better investment returns. Second, we broaden the functional forms of direction prediction to encompass machine learning techniques and forecast combinations, revealing that these models surpass simple linear approaches. Third, while valuation-ratio and volatility are important, these mechanisms do not fully explain the predictability, highlighting the need for further research. Our research serves to narrow the gap between direction and value return prediction in asset pricing, adds to the body of knowledge on out-of-sample predictability of stock returns, and extends the application of machine learning in this domain.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend