Alternative investment assets (also such as rare vintage and collectible items, expensive old high-quality alcohol, discontinued fashion, etc.) are a hit among wealthy investors, even though it is not easy to obtain direct or indirect exposure to diversified art investment(s) in a traditional finance kind of way. However, alternative assets are helpful in portfolio diversification as they last (if stored properly), usually appreciate in value (but sometimes not very predictably), and have a low correlation to traditional assets like stocks, real estate, gold, or fixed-income securities. Although alternative assets are highly illiquid and sometimes very challenging to value correctly, researchers are interested in them. We will closely look at one of the research papers that investigates the role of art in the portfolio, utilizing mean-variance optimization and less-used STL decomposition.

Art returns are highly volatile, and much of this volatility can be attributed to the seasonal behavior of the time series. In Barro, Basso, Funari, and Visentin (2023) paper, they analyzed art’s contribution to portfolio diversification. Notwithstanding the high risk, art still performs reasonably well compared with other asset classes, with which it is lowly correlated and may even represent a better safe haven than gold.

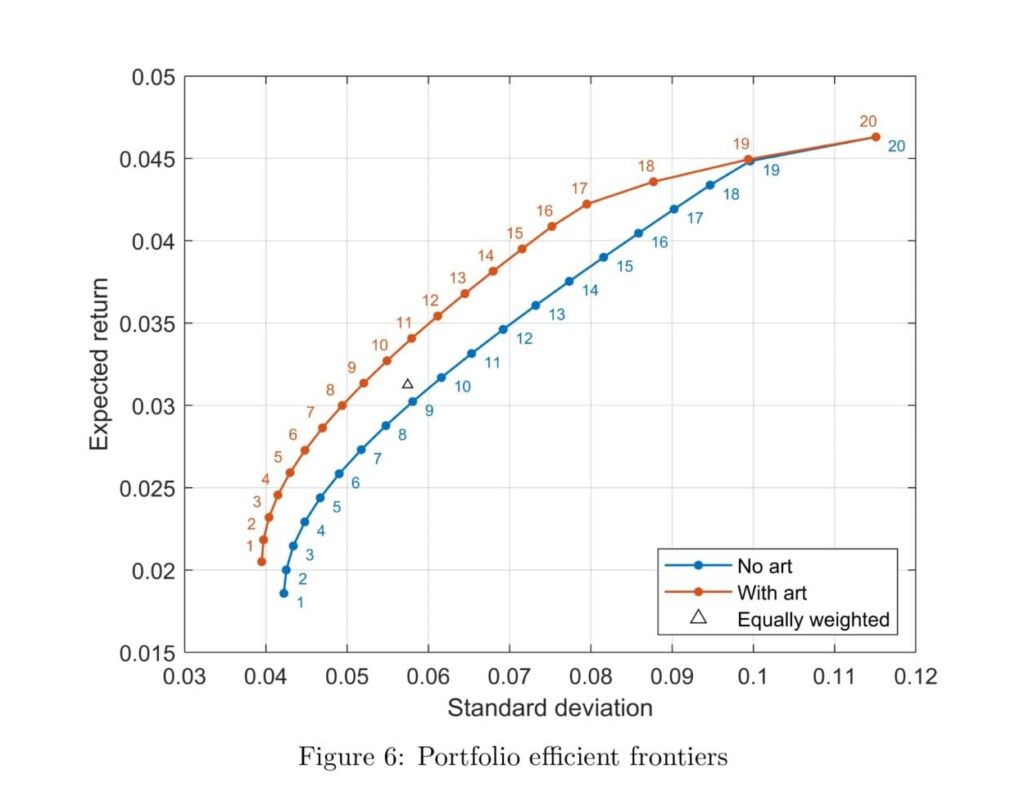

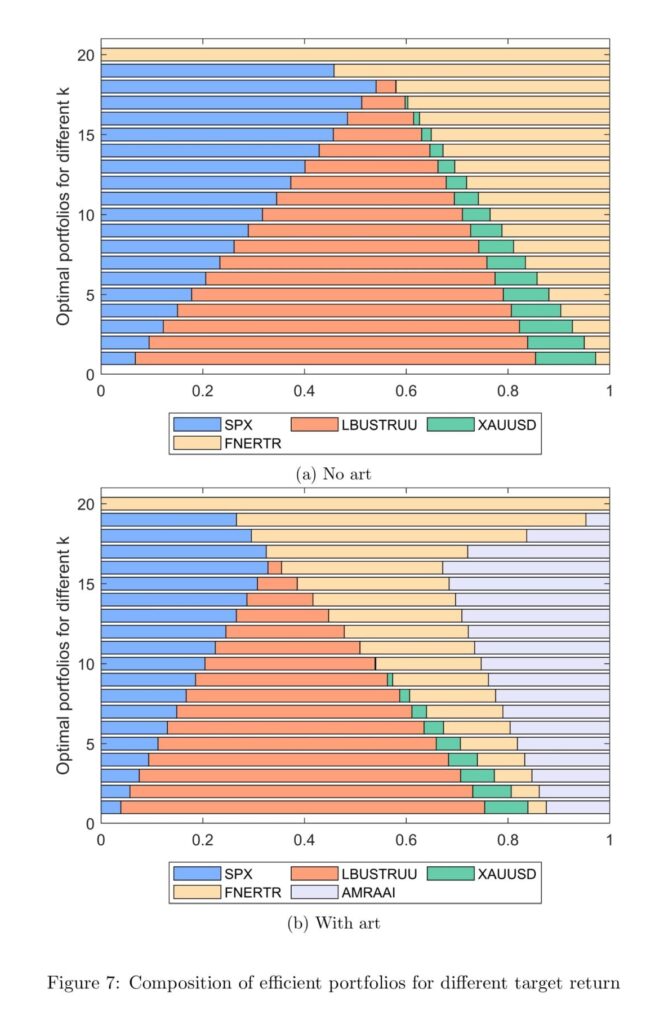

Portfolio analysis has shown that art enters efficient portfolios, allowing the investor to lower the portfolio variance for a given target return. Since art, like gold and real estate, is illiquid, implementing an upper bound to allocate alternative assets in the optimization model resulted in the optimal allocation in art dropping but still reaching the upper bound.

If the investor decides to allocate at most a fixed percentage of wealth in one or more alternative assets, there is appealable evidence that a portfolio of stocks and bonds diversified with art outperforms both a portfolio diversified with gold or real estate and even one diversified with all the alternative investments taken into consideration altogether which is strong but claim to be considered about, especially by the most wealthy clients focused on wealth preservation primarily.

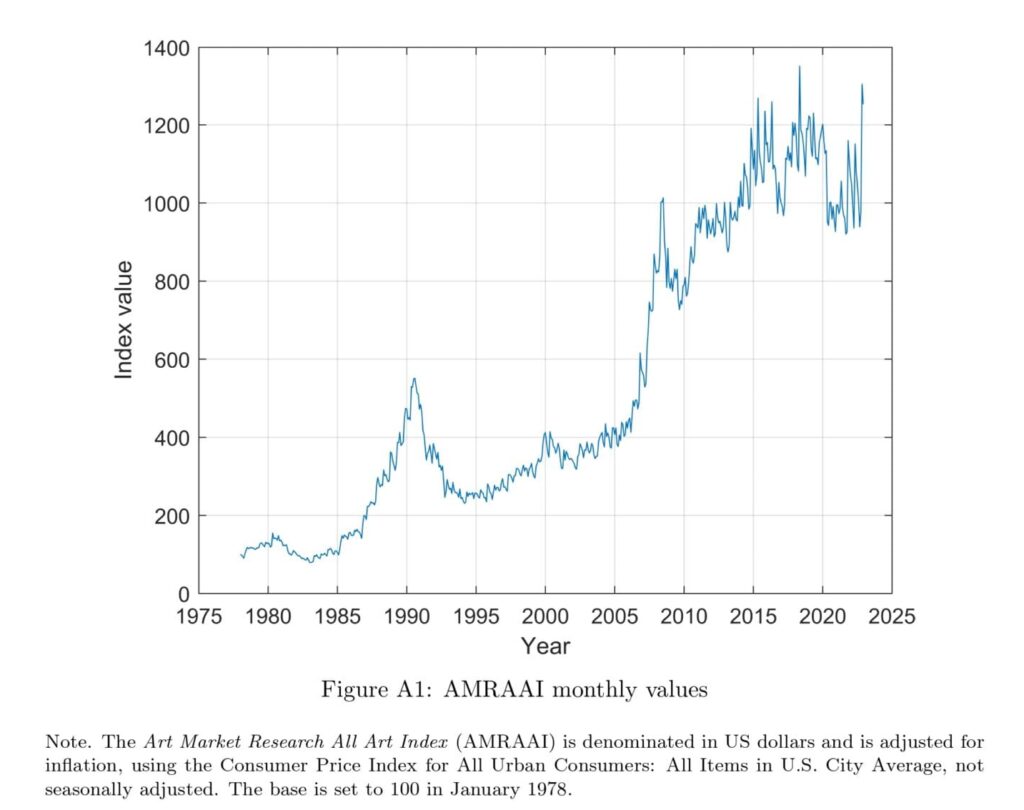

However, the study presents a few limitations one should be aware of. First, like all art indices, the AMRAAI (see featured Figure A1) is not tradable. Thus, it is up to the investor to decide which artworks to invest in (which can be really tricky without expert advice). Ignored transaction costs, which are high in the art market, and further costs arising from holding art (e.g., storage and insurance costs) also create a burden worth considering.

In conclusion, the authors closing thoughts are that investors should seriously take art into consideration if they are concerned with lowering the risk of their portfolio and hedging against economic and financial crises.

Authors: Diana Barro, Antonella Basso, Stefania Funari, and Guglielmo Alessandro Visentin

Title: Portfolio Diversification Including Art as an Alternative Asset

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4617318

Abstract:

In the last decades, financial markets have experienced great uncertainty that has led investors to look for alternative assets to further diversify their portfolios. Art and collectibles fall under such category, and there is a lively debate among academics and practitioners regarding the role of art in financial markets and portfolio choices. For such reason, we investigate the financial characteristics of the art market, and build a portfolio diversified with art to asses whether it outperforms, in terms of risk and return, portfolios which do not include art. We show that art performs well compared with standard and other alternative investments with which art is low correlated. In addition, we find that art returns follow an untypical seasonal pattern, and that much of the volatility in the art market can be attributed to the seasonal component of the time series. Finally, the results of the portfolio optimization analysis indicate that art enters efficient portfolios, and when additional constraints are implemented into the classical mean-variance optimization model, to account for investors’ preferences for liquidity, portfolios which include art still perform well.

And as always we present you some of interesting figures and tables:

Notable quotations from the academic research paper:

“In this paper, we contribute to the research on portfolio diversification through art, by providing further evidence on whether art should be included in financial portfolios. To this aim, first, we carry out a time series analysis of an index representing the art market, to shed light on its characteristics, using a decomposition method that allows us to isolate the effect of the components of the time series on the observed returns. Next, we build a portfolio diversified with art and employ the classical mean-variance optimization model to asses whether it outperforms, in terms of risk and return, portfolios which do not include art. Moreover, we implement additional constraints into the optimization model, in order to take the peculiarities of art and other alternative assets into account. In such a manner, the portfolio allocation obtained resembles that of an investor who considers further aspects as well as mean, variance and covariance of returns.

The scope of our paper is to analyze whether investing in art may benefit the investor in terms of portfolio risk and return. As discussed above, an art index is necessary to the purpose, and we adopt the All Art Index provided by AMR. The index (henceforth AMRAAI), which is exclusive of buyer’s premium, is expressed in pound sterling, and data are available in monthly frequency, from January 1978. AMR monitors the most important auction houses worldwide, and all artists who sold there at least one artwork in the past 24 months are included in the index computation. As a result, the index represents a major share of the aggregate art market, and similarly to a stock market index, such as the SP500, its basket is not fixed and changes over time. To carry out the analysis, we use data spanning from January 1978 to December 2022, and we consider the perspective of an investor who operates in the US market. Hence, we convert the AMRAAI to a US dollar-denominated index using the monthly GBP to USD exchange rate, available in Bloomberg. Moreover, given the change in the purchasing power over this extended time period, we adjust the AMRAAI for US inflation using the Consumer Price Index4, downloaded from the website of the Federal Reserve Bank of St. Louis.

In Section 3.2 we have showed that AMRAAI returns are affected by seasonality, and that returns peak in May and November, since the most prestigious works of art are sold in such months. To analyze the benefits of portfolio diversification through art, we consider an American institutional investor, and we assume that he/she is interested in the high-end of the art market only, so that transactions will occur only in May and November. Thus, we construct a semi-annual art index using only May and November values. Note that in such a manner we avoid the seasonal behavior of AMRAAI returns.

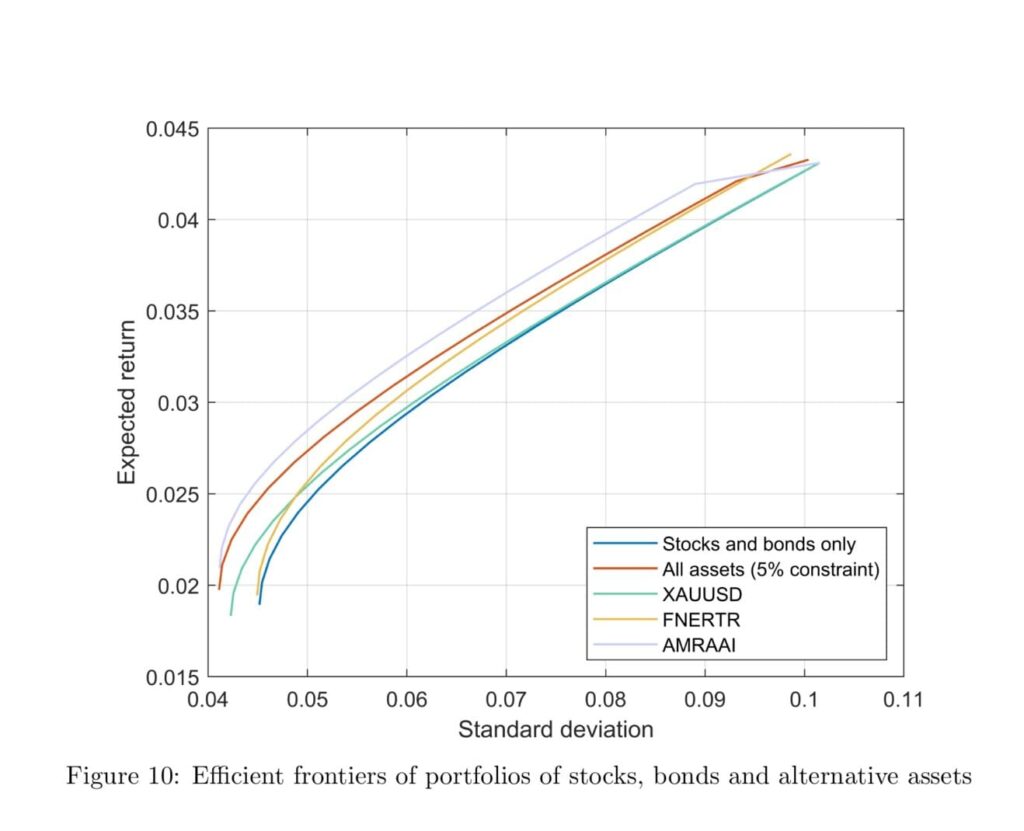

To summarize, when compared to standard and other alternative asset classes, art per- forms reasonably well and dominates gold in terms of risk and return, even if it is dominated by stocks. However, one must bear in mind that in this analysis we are considering exclusively the high-end of the art market, rather than its entirety, and that we are ignoring all transaction costs.

Figure 10 displays the efficient frontiers of portfolios of stocks and bonds diversified with the alternative asset. The results are compared with a portfolio consisting of stocks and bonds only, and with the portfolio, previously calculated, where all five asset classes are considered and the upper bound for each alternative asset is set to 5% of the total wealth. Unsurprisingly, the rightmost efficient frontier represents portfolios of stocks and bonds, whilst efficient frontiers of portfolios diversified with alternative assets lie more to the left in the risk-return plane. Notice that portfolios diversified with art (AMRAAI ) lie leftmost. Thus, had the investor to allocate up to 15% of his/her wealth in one alternative asset among gold, real estate and art, he/she should invest in art, since it allows him/her to obtain, for a given return, the portfolio with the lower volatility. What is more, portfolios of stocks, bonds and art perform better than those consisting of all five assets classes. This implies that art alone offers a good diversification gain.

In conclusion, investing a fraction of wealth in art enhances the performance of the portfolio in terms of risk and return, and artworks may represent a better safe haven than gold, given their higher expected return and the low correlation with other asset classes.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend