Refining ETF Asset Momentum Strategy

Today’s research introduces a refined ETF asset momentum strategy by combining a correlation filter with selective shorting. While traditional long-short momentum strategies usually yield suboptimal results, the long leg proves effective on its own, and the correlation filter demonstrates significant value for improving the timing and performance of the short leg. We propose a final strategy of going long on 4 top-performing ETFs while selectively shorting 1 ETF with a 30% weight. Our findings demonstrate that this combined long-short selective hedge strategy significantly outperforms standalone momentum strategies and the benchmark, delivering superior risk-adjusted returns and effective hedging during unfavorable market conditions.

Introduction

Momentum is undoubtedly one of the most widely recognized market anomalies. It operates on the premise that winners tend to continue outperforming while losers underperform. However, its returns have declined in recent decades, particularly in homogeneous markets with high asset correlations. As shown in “Robustness Testing of Country and Asset ETF Momentum Strategies” highly correlated country ETFs fail to deliver significant alpha. Conversely, the diversity and low correlation of asset ETFs present a more favorable environment for momentum strategies.

Inspired by these findings, we wanted to explore methods to address the declining performance of momentum strategies in homogeneous markets, particularly commodity ETFs. We sought to answer the question “How to Improve Commodity Momentum Using Intra-Market Correlation”. We calculated the ratio between 20-day and 250-day correlation and investigated its use in identifying periods when momentum strategies are likely to succeed. The findings demonstrate that when the short-term correlation exceeds the long-term correlation, a momentum strategy—going long on top-performing ETFs and short on underperformers—yields optimal results. Conversely, when the short-term correlation is lower, a reversal strategy is more effective.

Similarly, “How to Improve ETF Sector Momentum” highlighted the potential of combining long-only momentum with selective shorting. Although the long-short ETF sector momentum strategy by itself does not perform well, the correct independent settings of long and short legs can yield efficient results. By reducing the short leg’s weight to 5%-30% and applying it only during negative market trends, the strategy achieved significantly improved performance.

The main goal of this article is to build upon the aforementioned ideas to enhance ETF asset momentum strategies. We propose combining momentum with a correlation filter to selectively hedge using short positions when appropriate. First we test a simple momentum strategy. Next, we develop the correlation filter as a predictor. We then explore how many assets should be bought and sold and focus on finding the sweet spot—the perfect balance between long and short positions and their weights. The novelty of our paper lies in creating a smarter way to use momentum strategies: combining ideas like selective shorting and correlation trends to make the strategy work better and reduce risks.

Data & Methodology

Our analysis is based on the adjusted close prices of 13 ETFs, obtained from Yahoo Finance. Adjusted close prices were chosen as they account for dividends, stock splits, and other events influencing ETF value. The dataset spans from April 10, 2006, to February 28, 2023.

However, recently, Yahoo Finance discontinued free end-of-day data downloads. As a result, we recommend sourcing data from our preferred provider, EODHD.com – the sponsor of our blog. EODHD offers seamless access to +30 years of historical prices and fundamental data for stocks, ETFs, forex, and cryptocurrencies across 60+ exchanges, available via API or no-code add-ons for Excel and Google Sheets. As a special offer, our blog readers can enjoy an exclusive 30% discount on premium EODHD plans.

Our investment universe consists of 13 ETFs representing various asset classes. These include 6 stock ETFs, 3 bond ETFs, 3 commodity ETFs, and 1 currency ETF.For stock ETFs we chose SPDR S&P 500 ETF Trust (SPY), iShares Russell 2000 ETF (IWM), iShares MSCI EAFE ETF (EFA), iShares MSCI Emerging Markets ETF (EEM), iShares U.S. Real Estate ETF (IYR), Invesco QQQ Trust (QQQ). For bond ETFs we chose iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD), iShares 7-10 Year Treasury Bond ETF (IEF), iShares TIPS Bond ETF (TIP). For commodity ETFs we chose SPDR Gold Shares (GLD), United States Oil Fund, LP (USO), Invesco DB Commodity Index Tracking Fund (DBC). Lastly we included Invesco CurrencyShares Euro Currency Trust (FXE) as the currency ETF.

The benchmark for our analysis is an equally weighted portfolio of the 13 selected ETFs.

The analysis is divided into 4 main steps.

First, the Simple Momentum Strategy. Using price data, we calculate the 1- to 12-month momentum for each ETF each month and rank them based on their performance. This ranking provides the signals for which ETFs to go long and which to short. We test this strategy with equal weights across the portfolio, rebalancing monthly, and accounting for shorting costs.

Second, the Correlation Filter. We calculate short-term (20-day) and long-term (250-day) correlations among ETFs. The ratio of these correlations serves as a filter to identify favorable conditions for momentum strategies. If short-term correlation exceeds long-term correlation, a momentum strategy is applied. If short-term correlation is lower, no position is entered.

Third, the Optimal Number of Assets. We explore the ideal number of ETFs to include in the portfolio for both long and short legs during a fixed period (using an average of the 3, 6, 9, and 12-month momentum periods).

Finally, the Optimal Weighting Scheme. We hypothesize that a short leg with reduced weight can effectively hedge the long leg without excessive risk. We test various weight schemes to determine the most suitable one.

Results

Asset Momentum

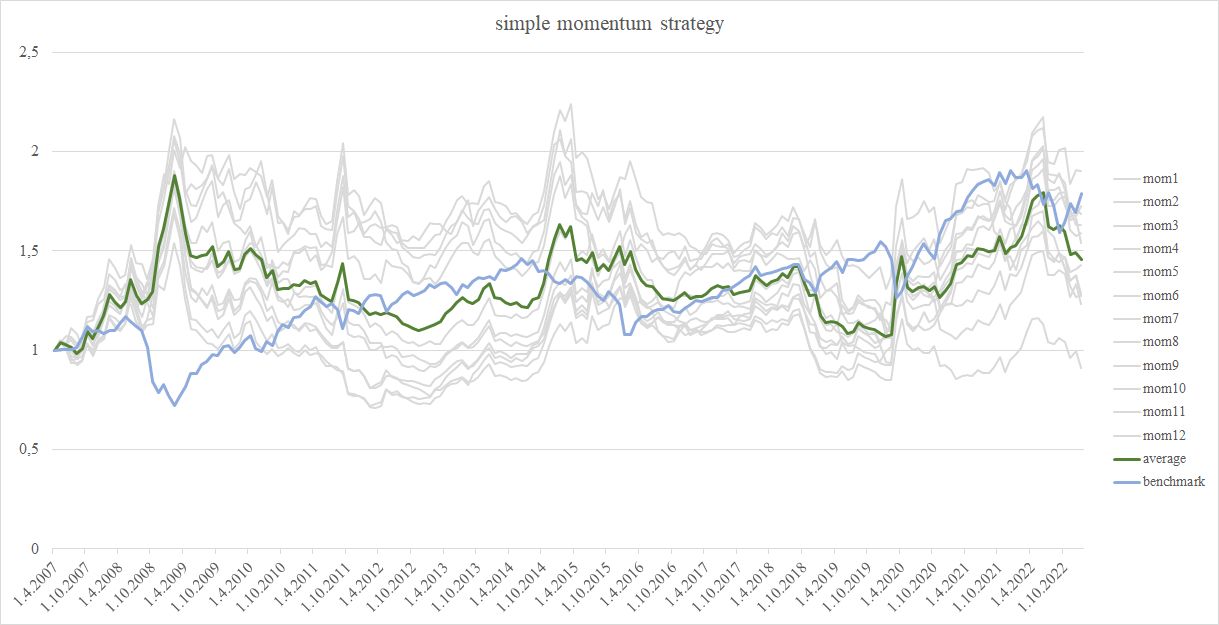

The first step in our analysis was to test a simple momentum strategy. We find that despite variation in ranking period and the number of assets, the long-short momentum strategy’s performance is dissatisfying in most cases. Figure 1 illustrates the cumulative performance of the simple momentum strategy as well as benchmark, while Table 1 provides average performance metrics for portfolios with 4 ETFs held long and 4 ETFs held short. The long-short momentum strategy underperformed the benchmark across all ranking periods, as evidenced by lower Sharpe and Calmar ratios in Table 1. Lower performance and higher volatility compared to benchmark highlight the need for refinement of this strategy.

Figure 1 long-short simple momentum strategy

Table 1 long-short simple momentum strategy characteristics

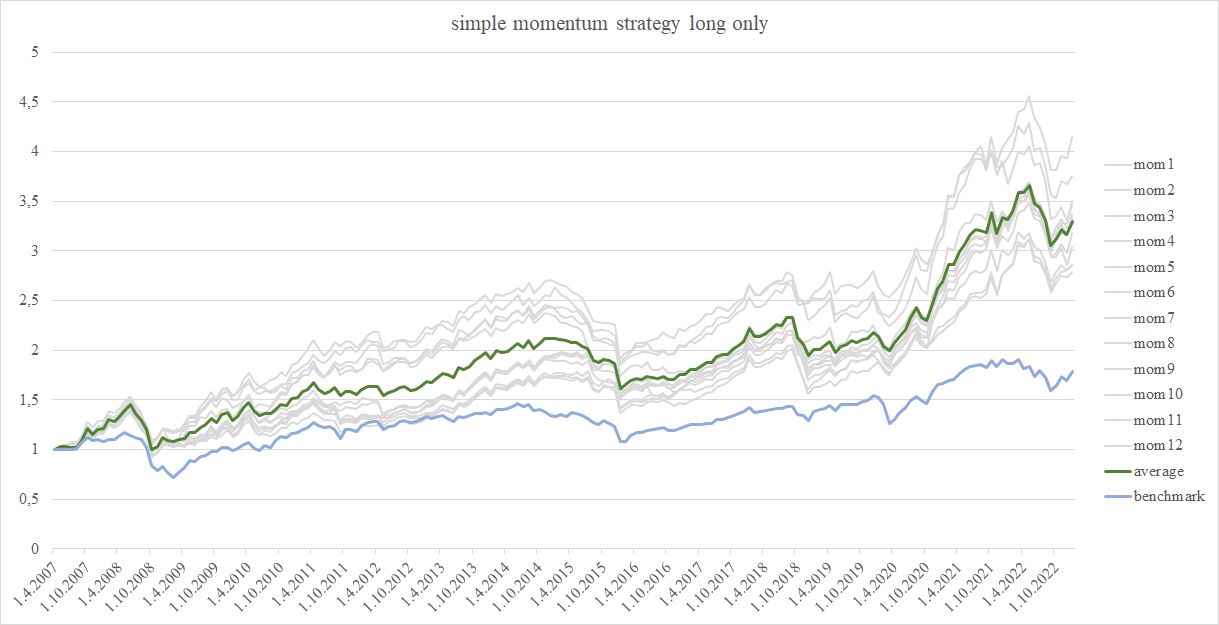

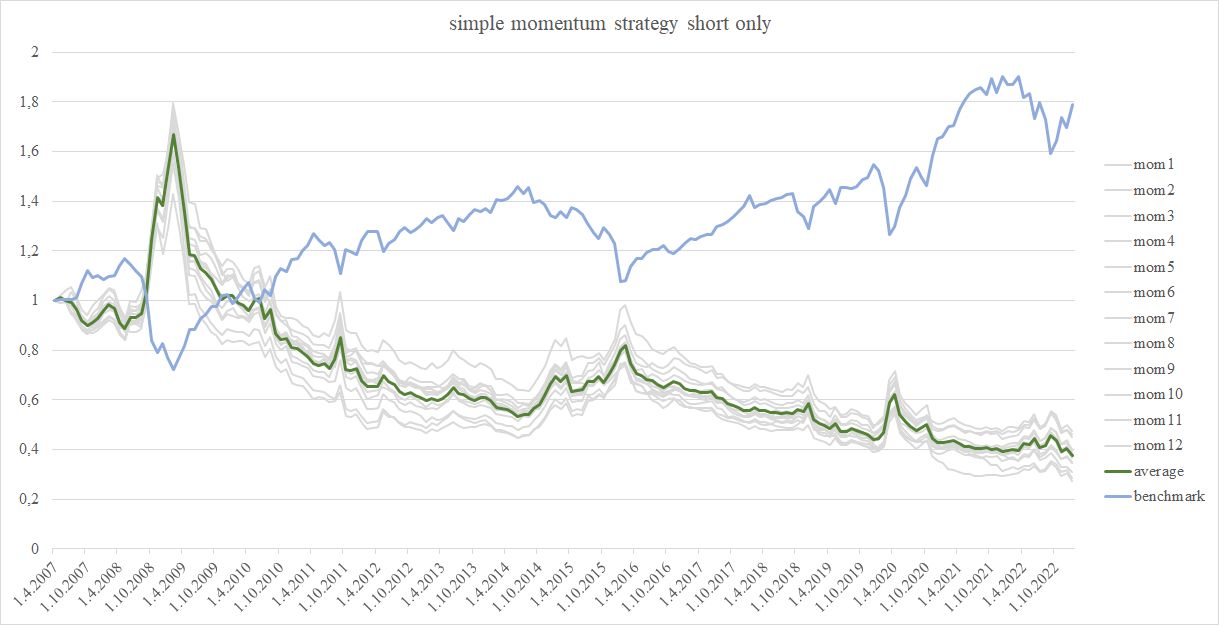

For deeper understanding of underlying dynamics, we decided to look at performance over 1-12 month period for long leg and short leg separately. As shown in Figure 2 and Table 2, the long leg consistently outperformed the benchmark, regardless of the ranking period. In contrast, Figure 3 and Table 3 reveal that the short leg consistently underperformed the benchmark. This indicates that reducing weight of the short positions can improve the strategy’s overall performance as demonstrated in the literature.

Figure 2 long-only momentum

Table 2 long-only momentum characteristics

Figure 3 short-only momentum

Table 3 short-only momentum characteristics

Correlation Filter

As in our previous articles, we used the correlation filter as a predictor to identify when it is favorable to apply a momentum strategy. The main idea is that if the average short-term (20-day) correlation exceeds the average long-term (250-day) correlation, it indicates that ETFs are trending in one direction, making momentum strategies more effective in distinguishing between winners and losers. This analysis was conducted separately for the long leg and short leg.

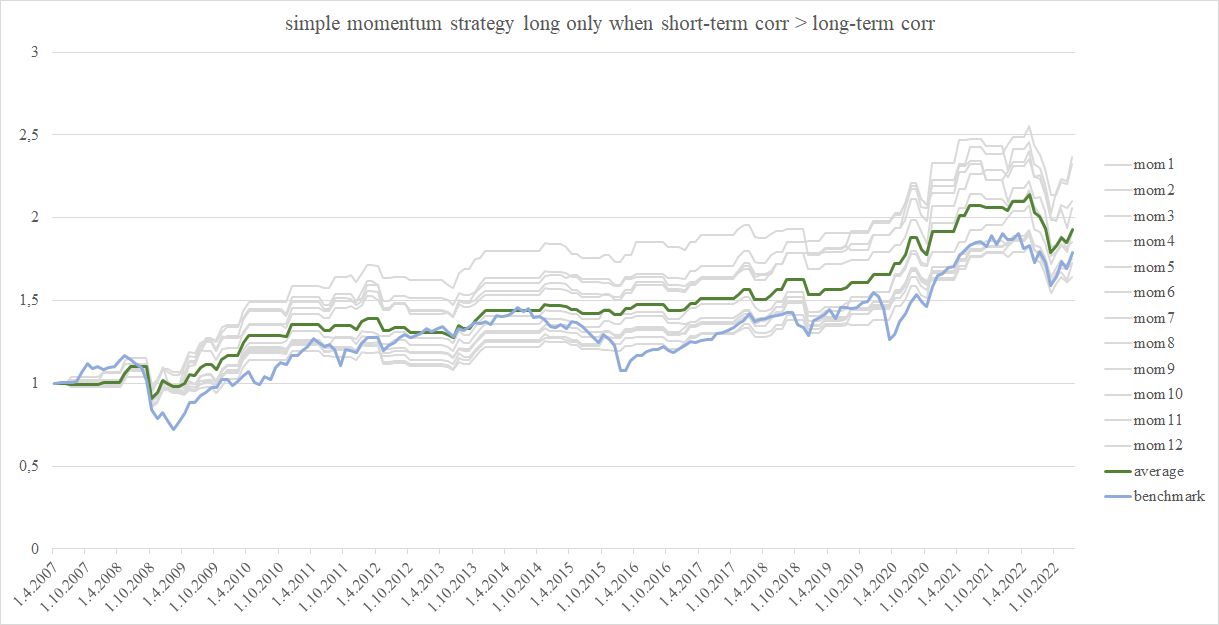

We first applied the correlation filter to the long leg, analyzing situations where short-term correlation exceeds long-term correlation and where short-term correlation is lower than long-term correlation. When short-term correlation exceeds long-term correlation, the long leg’s performance improves compared to the benchmark, as reflected in higher Sharpe and Calmar ratios (see Figure 4 and Table 4). Even when short-term correlation is lower than long-term correlation, the long leg’s performance remains acceptable, as shown in Figure 5 and Table 5.

We conclude that the correlation filter has a limited impact on the long leg. Momentum alone is sufficient to drive returns for the top-performing ETFs, and the filter does not significantly enhance or diminish results in this case.

Figure 4 long-only momentum when short-term correlation exceeds long-term correlation

Table 4 long-only momentum when short-term correlation exceeds long-term correlation characteristics

Figure 5 long-only momentum when short-term correlation is lower than long-term correlation

Table 5 long-only momentum when short-term correlation is lower than long-term correlation characteristics

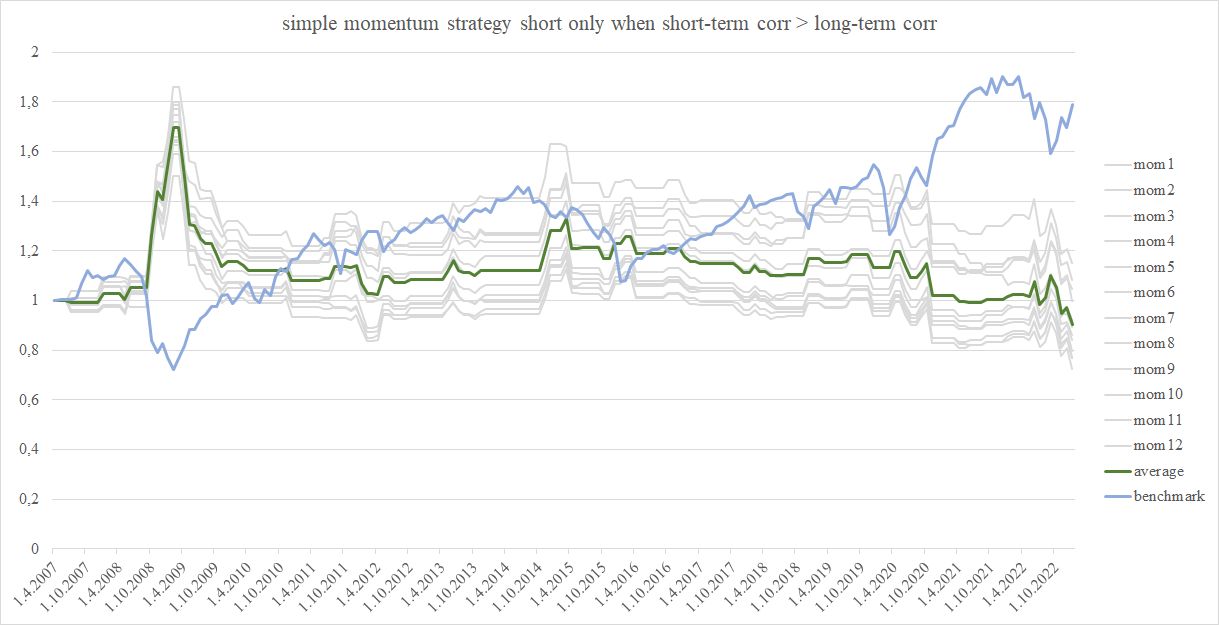

We then applied the correlation filter to the short leg to identify periods when short positions would be more effective. The filter seems to reliably separate periods of strong underperformance (figure 7, table 7) and not so abysmal performance (Figure 6, Tables 6). This feature makes a correlation filter useful for selective hedging by picking the right moments to open cheap short positions (as the green line in Figure 6 suggests).

Figure 6 short-only momentum when short-term correlation exceeds long-term correlation

Table 6 short-only momentum when short-term correlation exceeds long-term correlation characteristics

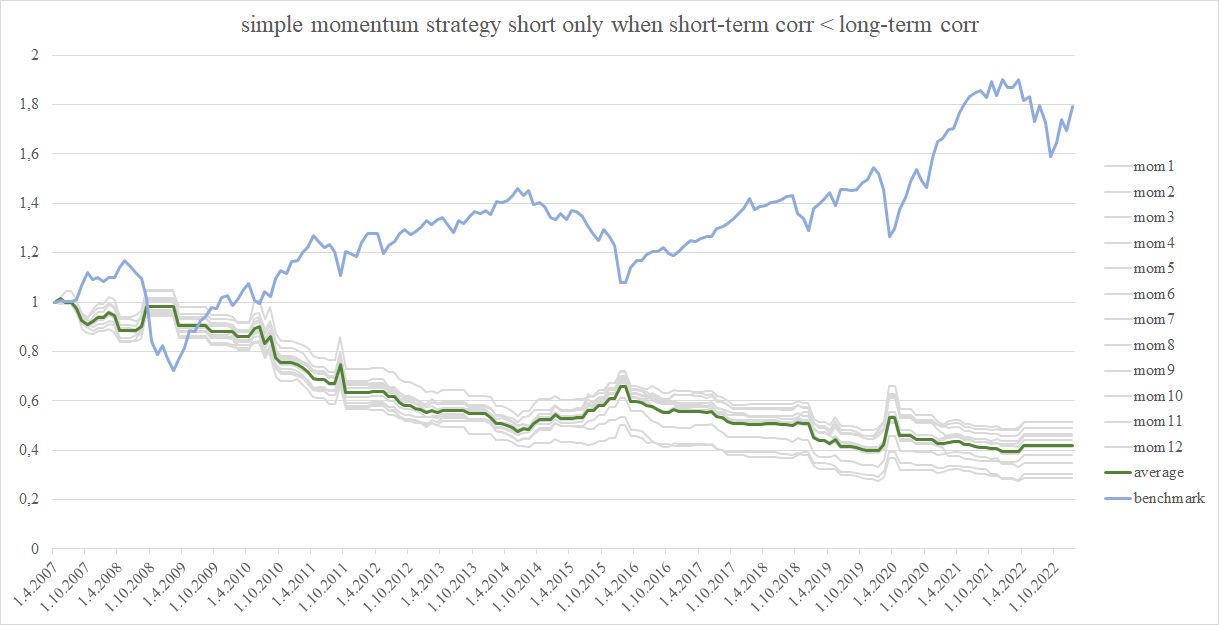

Figure 7 short-only momentum when short-term correlation is lower than long-term correlation

Table 7 short-only momentum when short-term correlation is lower than long-term correlation characteristics

The correlation filter + momentum are most useful for improving the timing and selection of short positions. This makes it effective to use for selective hedging as it helps to avoid shorting during unfavorable conditions and capitalizing on favorable ones. Momentum alone is the key driver for the long leg, requiring minimal filtering.

The previous analyses tested 1-12 month ranking periods, but we sought to narrow down the momentum timeframes. For the next stages, we decided to use the industry standard and average performance across four specific timeframes: 3, 6, 9, and 12 months.

Number of assets in fixed period

This part of the analysis focuses on determining the optimal number of ETFs to include in the portfolio for both long and short legs.

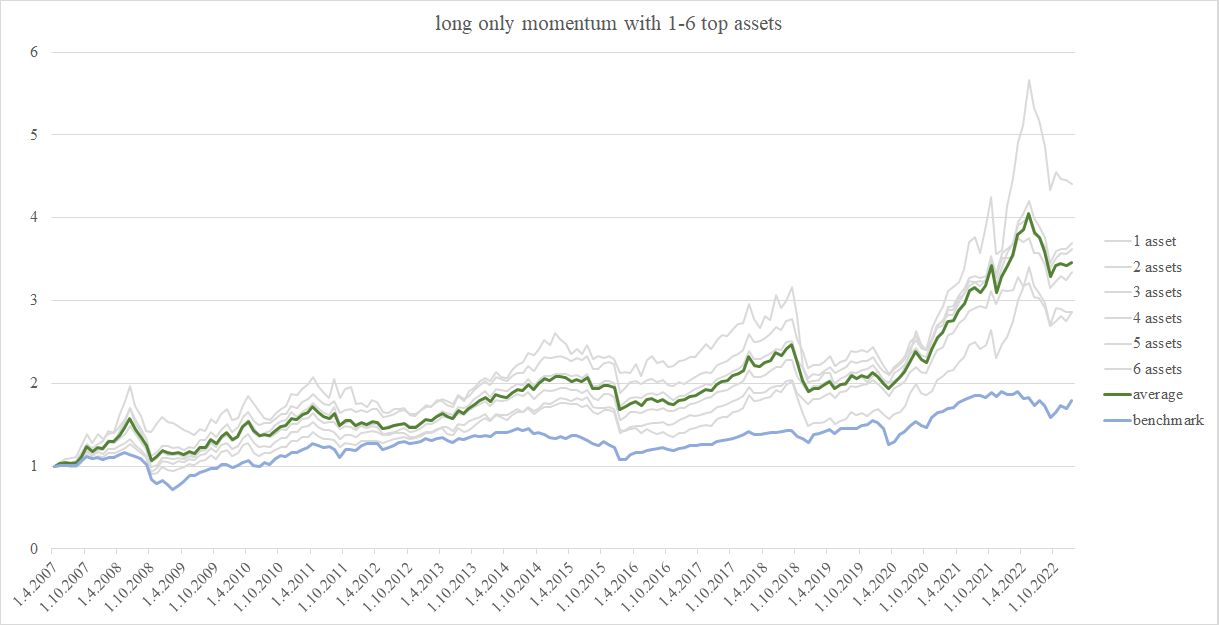

First, we tested portfolios with 1 to 6 ETFs in the long leg, using the average performance over 3, 6, 9, and 12-month momentum periods. The results show that portfolios with 3 to 6 ETFs provide the most stable performance, as seen in Figure 8 and Table 8. We believe that holding 4 assets (the top tercile of the investment universe) is optimal.

Figure 8 long-only momentum with varying number of assets

Table 8 long-only momentum with varying number of assets characteristics

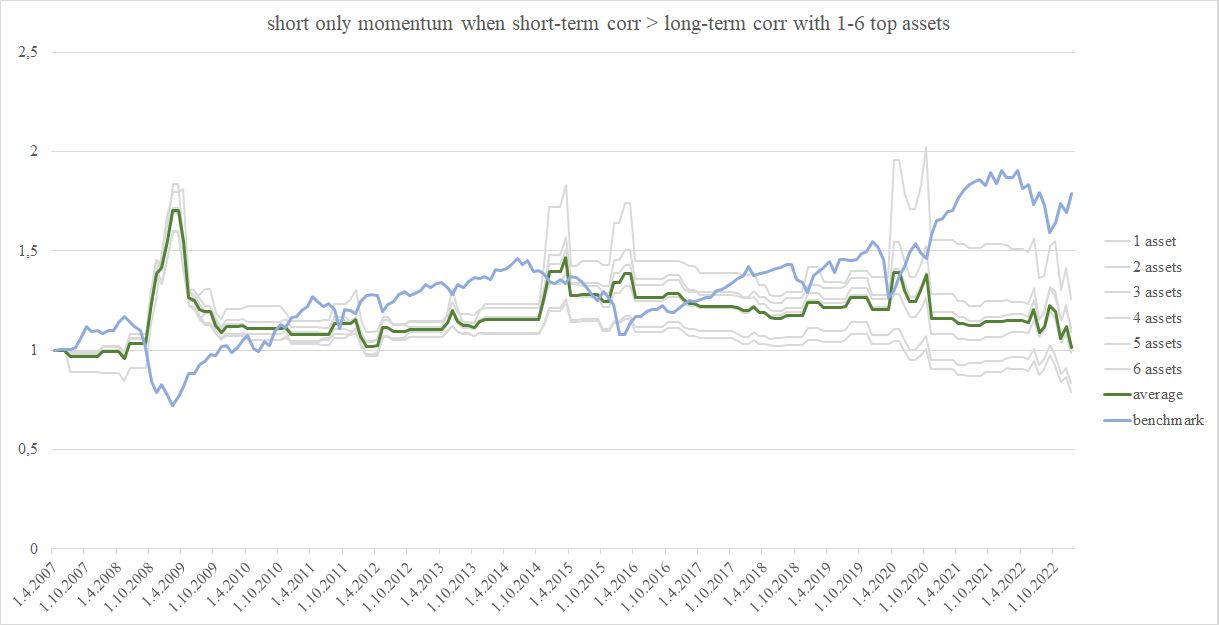

For the short leg, we followed the same process and found that the performance of the short leg is best when it includes fewer (1-3) ETFs, as shown in Figure 9 and Table 9. We consider shorting a single ETF to be optimal.

Figure 9 short-only momentum when short-term correlation exceeds long-term correlation with varying number of assets

Table 9 short-only momentum when short-term correlation exceeds long-term correlation with varying number of assets characteristics

Long-short selective hedge

Based on our earlier findings and related literature, we develop our final strategy by combining the long leg with weighted and selectively applied short leg. We then compared its performance to that of the long-only momentum strategy and the benchmark.

The long leg uses the pure momentum strategy, investing in the 4 top-performing ETFs based on the average of 3, 6, 9, and 12-month momentum rankings. As established earlier, this position provided stable performance without requiring additional filtering.

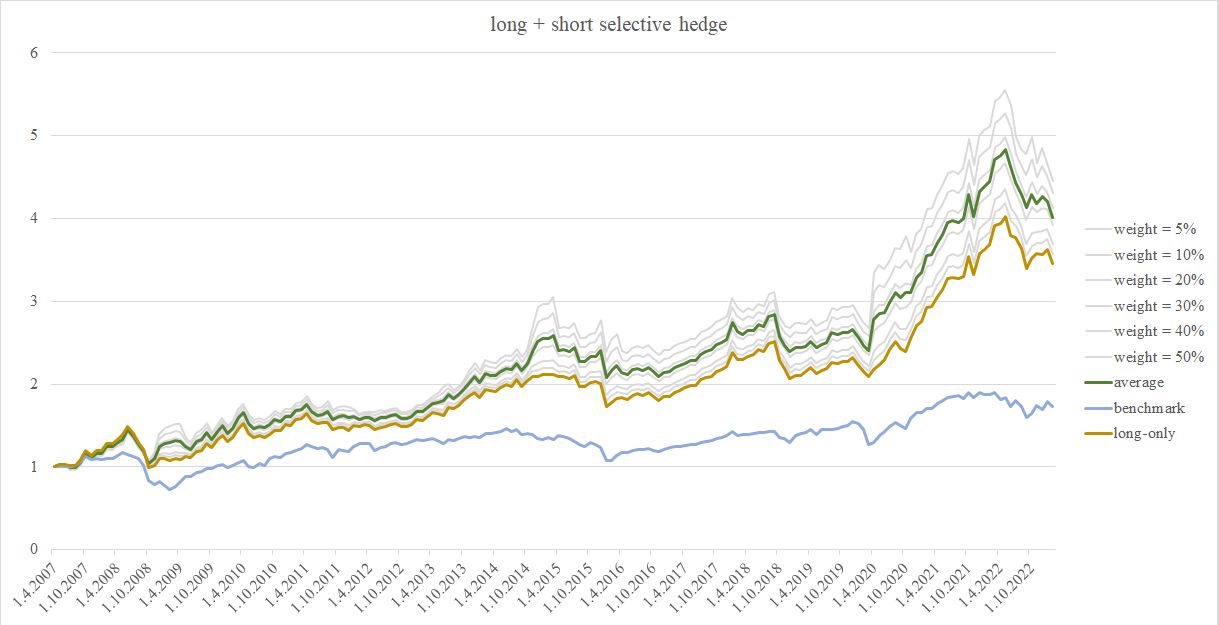

For the short position, we opted to short a single ETF and tested weights ranging from 5% to 50%. We believe a 30% weight offers the best balance, as it minimizes risk while effectively hedging during unfavorable market conditions. Table 10 provides an overview of performance metrics across different weights. Moreover, the 30% weight aligns with prior findings and literature highlighting the benefits of reduced short exposure.

In conclusion, the final long- short selective strategy outperforms the long-only momentum strategy and the benchmark, as shown in Figure 10 and Table 10. The Sharpe and Calmar ratios are significantly higher for the long-short selective strategy, indicating better risk-adjusted returns.

Figure 10 100% long momentum + variable weight of short selective hedge

Table 10 100% long momentum + variable weight of short selective hedge – performance characteristics

Conclusion

After our efforts to enhance commodity and sector ETF momentum strategies, we applied the knowledge to improve ETF asset momentum. By combining the correlation filter—calculated as the ratio of 20-day to 250-day correlations among ETFs—with selective shorting, we developed a robust long-short strategy. The final strategy of going long on the 4 top-ranked ETFs and selectively shorting 1 ETF with a 30% weight, significantly enhances performance and outperforms the benchmark. Additionally, this strategy surpasses long-only momentum by providing effective hedging during adverse conditions.

These key findings of our analysis are: Traditional long-short momentum strategies underperform. After separating the long and short legs, we found the long-only leg to be effective, but the short-only leg required adjustments to improve performance. The correlation filter had a minimal impact on the long leg but proved highly effective for the short leg, reliably identifying periods for selective hedging. The long-short selective hedge strategy combines a long leg with a 30% weighted short leg, using a correlation filter. The strategy achieves a superior performance and return-to-risk ratios.

Author: Margaréta Pauchlyová, Quant Analyst, Quantpedia

References

Beluská, Soňa and Vojtko, Radovan, How to Improve ETF Sector Momentum * (October 11, 2024). Available at SSRN: https://ssrn.com/abstract=4988543 or http://dx.doi.org/10.2139/ssrn.4988543

Du, Jiang and Vojtko, Radovan, Robustness Testing of Country and Asset ETF Momentum Strategies (March 25, 2023). Available at SSRN: https://ssrn.com/abstract=4736699 or http://dx.doi.org/10.2139/ssrn.4736699

Vojtko, Radovan and Pauchlyová, Margaréta, How to Improve Commodity Momentum Using Intra-Market Correlation (September 16, 2024). Available at SSRN: https://ssrn.com/abstract=4964417 or http://dx.doi.org/10.2139/ssrn.4964417

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend