Seasonality Patterns in the Crisis Hedge Portfolios

Introduction

Building upon the established research on market seasonality and the potential for front-running to boost associated profits, this article investigates the application of seasonal strategies within the context of crisis hedge portfolios. Unlike traditional asset allocation strategies that may falter during market stress, crisis hedge portfolios are designed to provide downside protection. We examine whether incorporating seasonal timing into these portfolios can enhance their performance and return-to-risk ratios, potentially offering superior risk-adjusted returns compared to static or non-seasonal approaches.

Crucially, we also analyze the extent to which the benefits of seasonal timing are diminished by the actions of other market participants seeking to exploit the same predictable patterns. This research contributes to the existing literature by focusing on the intersection of seasonality and crisis hedging, providing valuable insights for investors seeking to optimize portfolio resilience in turbulent market environments.

Background

The existence of seasonality in financial markets has been a topic of academic inquiry for decades. Early studies, such as Keim (1983), documented predictable patterns in stock returns across months and quarters. Theobald (1992) also explored these patterns, particularly in thinly traded stocks. More recent research by Asness et al. (2013) confirms the presence of seasonal effects, highlighting their potential value in portfolio construction.

While seasonality offers opportunities for enhanced returns, it is also well understood that investors exploit these patterns, leading to potential front-running, elaborated by Moskowitz and Grinblatt (2002), where seasonality-driven strategies underperform due to arbitrage activity. According to our study, Front-Running Seasonality in US Stock Sectors, a front-running strategy that selects sectors ETFs based on their performance in the previous month, can outperform the benchmark. This suggests potential seasonality in US stock sectors.

Formulation in Context of Existing Research & This Study Statement

Building on this foundation, this paper investigates the efficacy of incorporating seasonality into crisis hedge portfolios. We examine whether seasonal factors can improve portfolio performance during market downturns and whether front-running behavior boosts or mitigates such benefits.

Our analysis thus extends the existing literature gap on seasonality in traditional asset allocation by focusing specifically on crisis hedge portfolios, offering valuable insights for portfolio managers seeking to navigate rough market conditions.

Data & Methods

Hedging Investment Universe Asset Selection

We aim to validate the seasonal patterns within a specified cross-hedge portfolio. To accomplish this Black Swan Hedging Model of Gioele (2019) from the Antifragile Asset Allocation strategy, we adopted the hedge portfolio constituents delineated in Table 5‘s list of ETFs. We are closely examining our hedging application concerning the presented hedge portfolio.

Following Giordano‘s footsteps, we also nod to Nassim Nicholas Taleb, options trader turned academic researcher, for his original thinking that produced the conceptualization of Black Swans and Antifragility.

Following in the table, six selected assets are listed:

For example, the data can be obtained from Yahoo Finance to elucidate the investment universe further. However, recently, Yahoo Finance discontinued free end-of-day data downloads. As a result, we recommend sourcing data from EODHD.com – the sponsor of our blog. EODHD offers seamless access to +30 years of historical prices and fundamental data for stocks, ETFs, forex, and cryptocurrencies across 60+ exchanges, available via API or no-code add-ons for Excel and Google Sheets. As a special offer, our blog readers can enjoy an exclusive 30% discount on premium EODHD plans. The analysis covers the period from 2007-02-13 to 2024-09-05, and the daily granularity is sufficient for the types of studies carried out.

As our benchmark, the most diversified and complex composition of assets is possible within the methods’ realm.

Seasonality Types

Furthermore, we can now move on to describing the two seasonality types employed in this study:

- Time-series seasonality (TSS)—Similar to our commodities study, we conduct an intra-asset comparison, analyzing performance over 12 months and examining months t-12 (true-seasonality) and t-11 (front-running seasonality) for potential predictors.

- Cross-sectional seasonality (CSS): We perform an inter-asset comparison within the portfolio, identifying the top and bottom performers within groups. Again, we focus on months t-12 and t-11 as predictors.

Results

Time-Series Seasonality (TSS)

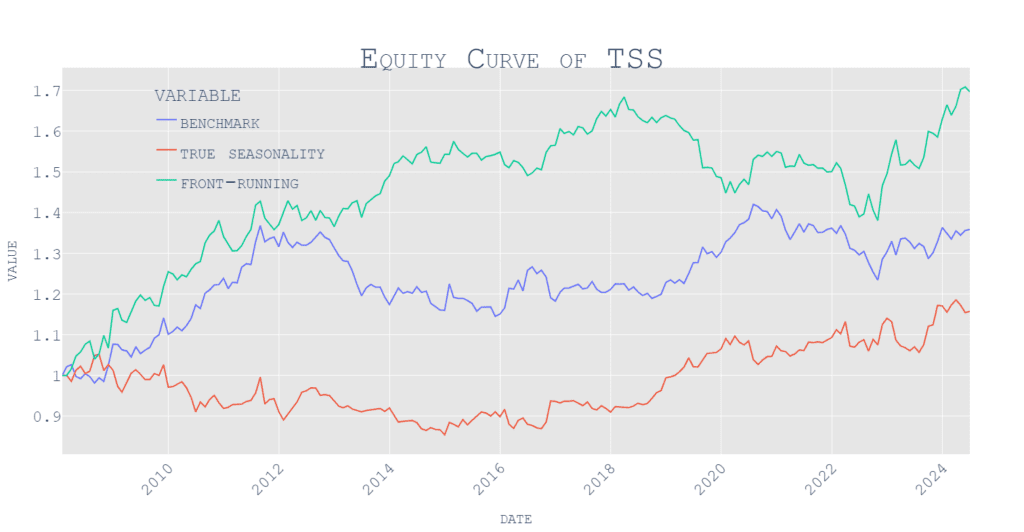

At first, we performed this type of seasonality to get a glimpse of both true (pure) seasonality and potential front-running aspects. Additionally, the charts and tables show the performance of the benchmark, which is the equally-weighted portfolio built from the six ETFs present in the crisis hedge investment universe.

First, we show the results in graphical form, appreciating the investment amount in the equity curve.

Again, presenting critical performance and risk metrics in the form of a table:

Interestingly enough, choosing any methodology would yield positive performance. However, as in the past articles/papers related to the seasonality patterns, we see that the performance of the seasonal strategy, which selects ETFs based on their performance over the same month (past January predicts future January returns, etc. etc.) underperforms benchmark (equally-weighted portfolio of ETFs) and alternative strategy that front-runs the seasonal signal by one month (past January predicts the performance of the December returns, etc. etc.)

Now, let us try the second approach…

Cross-Sectional Seasonality (CSS)

Here, we will apply two variants,

- long-only and

- spread (long-short) portfolios.

Front-Running Cross-Sectional Seasonality Strategies

Figures for long-only portfolios will first be presented, followed by a spread top-bottom (winner-minus-loser WML) portfolio for a fixed number of instruments (ranging from 1 to 3 for long legs and 0 to 3 for short legs). The benchmark for front-running is once again the equally weighted universe of underlying ETFs.

Here is a returns and risk table overview for all presented variants:

Surprisingly, all variants of the front-running strategy outperform the benchmark. The long-only variants have, on average, better performance and return-risk ratios than long-short variants. The sweet spot is going long two assets with the best performance in the month T-11. Adding short legs introduces too much risk into the overall strategy.

True (Pure) Cross-Sectional Seasonality Strategies

The benchmark for the true (pure) seasonality strategies is again the equally weighted portfolio of ETFs (as in previous cases). The same procedure is carried out as in the previous section; however, this time, we go long the ETFs with the best performance in T-12 month (and, additionally, short the worst performing ETFs in the case of long-short strategies):

And accompanying performance results and risk metrics table:

The overall results are disappointing when judging against front-running strategies. All of the variants of the true/pure seasonal strategies (based on T-12 sorting) underperform front-running seasonal strategies (T-11). Once again, we can confirm that even in the investment universe, which consists of ETFs that can be considered “crisis hedges”, front-running seasonality signals by one month outperform other alternative seasonality strategies.

Conclusion

In our crisis hedge ETF universe, front-running is evident in cross-sectional seasonal patterns and time-series seasonality. This dual occurrence underscores the pervasive nature of front-running across different dimensions of market seasonality. Incorporating seasonality into crisis hedge portfolios can significantly enhance performance and our results indicate that both time-series and cross-sectional seasonal strategies provide robust downside protection and superior risk-adjusted returns compared to static or non-seasonal approaches. This research bridges the gap between traditional asset allocation and seasonal strategies, providing a pivotal framework for portfolio managers aiming to enhance resilience in volatile market environments.

Author: Cyril Dujava, Quant Analyst, Quantpedia

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend