On the brink of the new millennium, the legendary value investor Warren Buffett studied the fundamentals behind the exceptional performance of the Dow Jones Industrial Average between 1981 and 1998 compared to its poor performance during the equally long period between 1964 and 1981. From 1981 to 1998, the Dow Jones index increased almost tenfold despite much slower economic growth than in the previous seventeen-year period. Buffett suggested that the market value of equity (MVE) scaled by gross domestic product (GDP) would have forecasted higher returns for 1981-1998 by indicating cheaper valuations for the stock market.

The rationale behind the market value of the equity to gross domestic product (MVE/GDP) ratio as the stock market valuation measure is simple. When the equity prices go up without a commensurate increase in economic output, the forward earnings yield decreases, making the equity investments less attractive. On the other hand, if the share prices scaled by GDP fall, the forward earnings yield increases, making equities more attractive. Unlike purely price-based valuation measures, such as the cyclically-adjusted price-to-earnings (CAPE) ratio, the MVE/GDP has the advantage that its numerator incorporates a qualitative (i.e., price) as well as a quantitative (i.e., number of shares) dimension. The model assumes that new share issuance increases (decreases) when equity markets are overvalued (undervalued) if corporate managers are able to time the market.

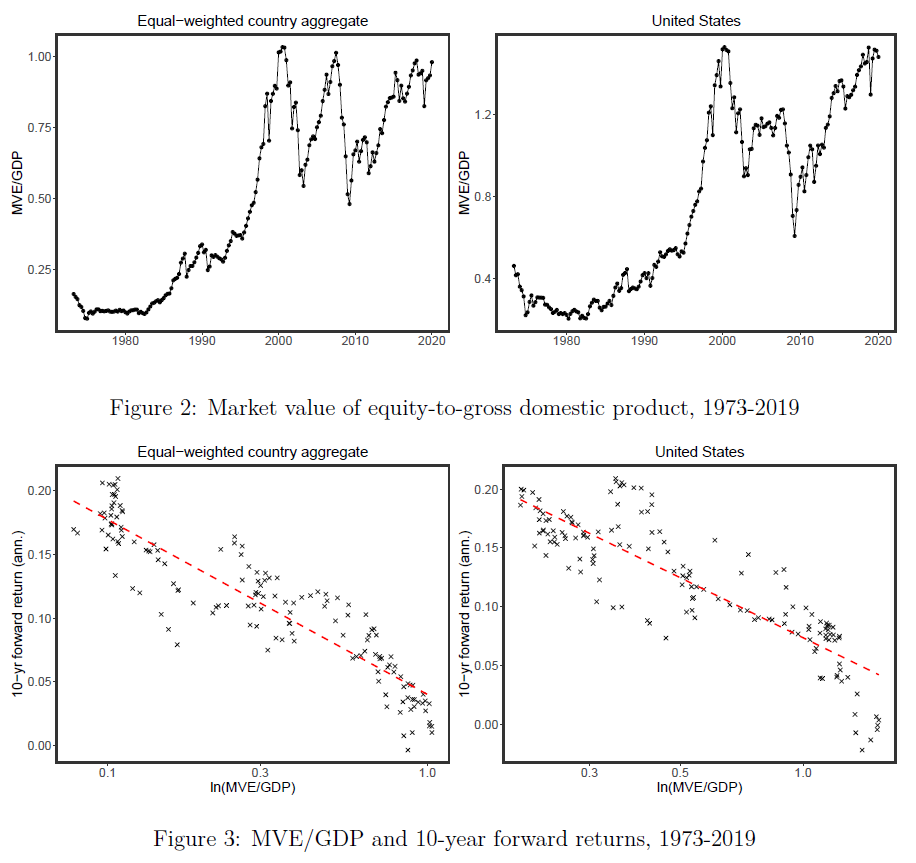

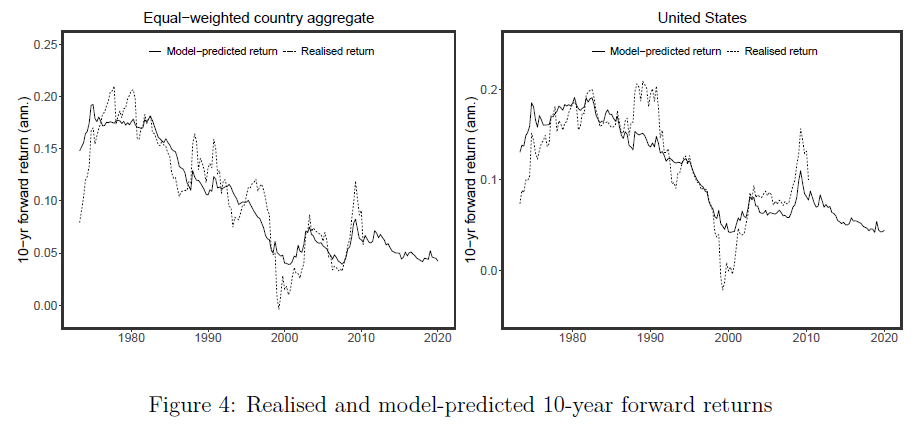

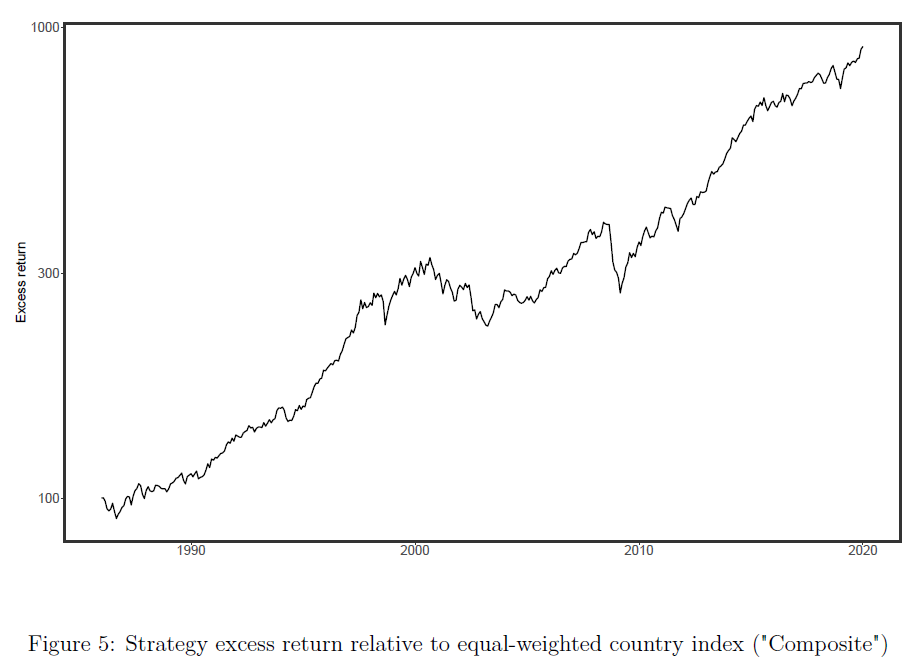

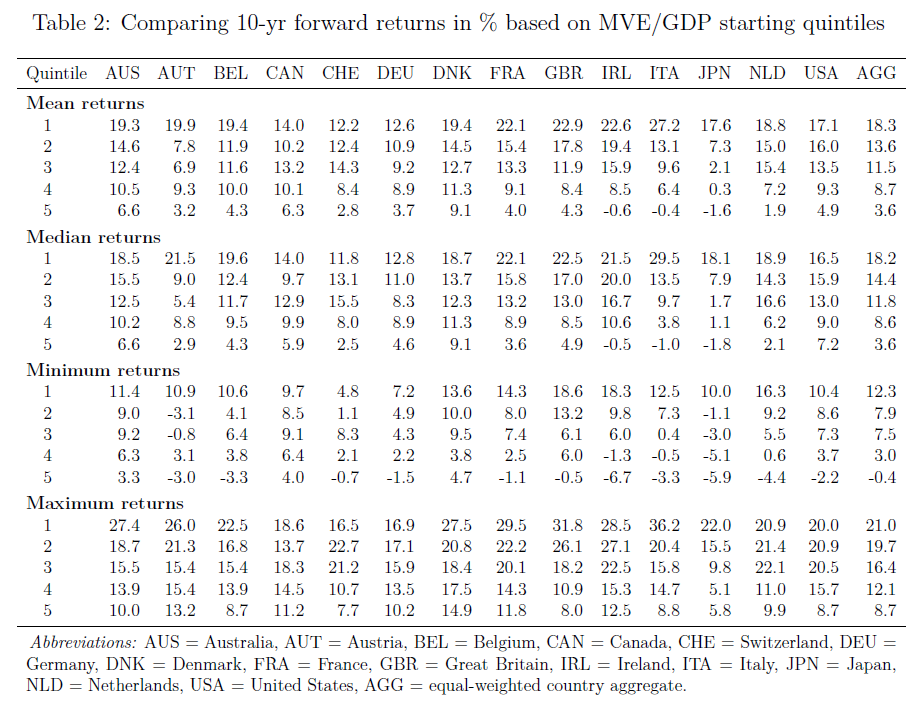

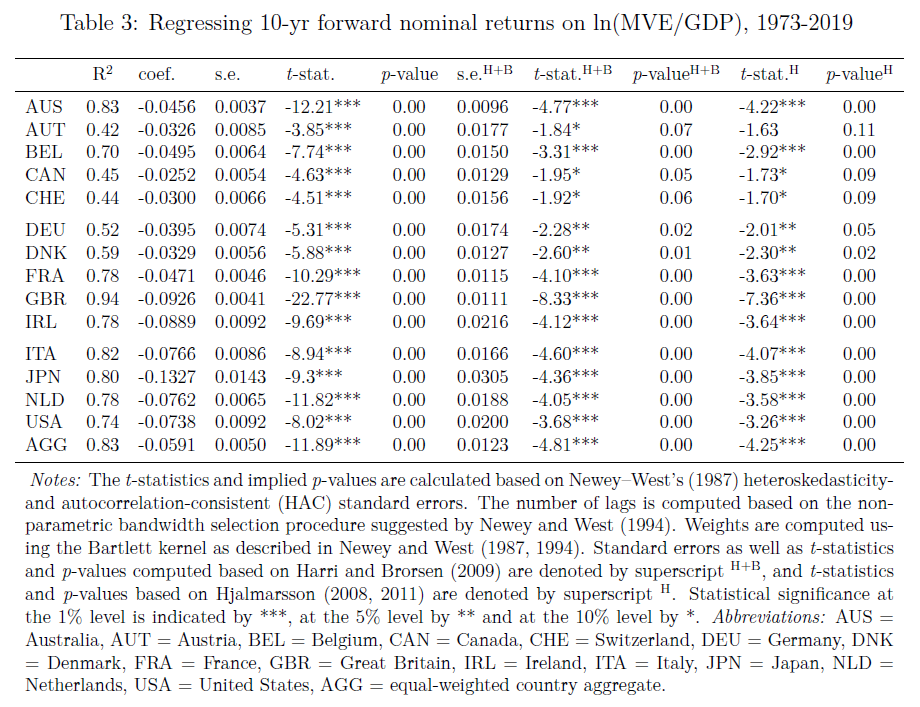

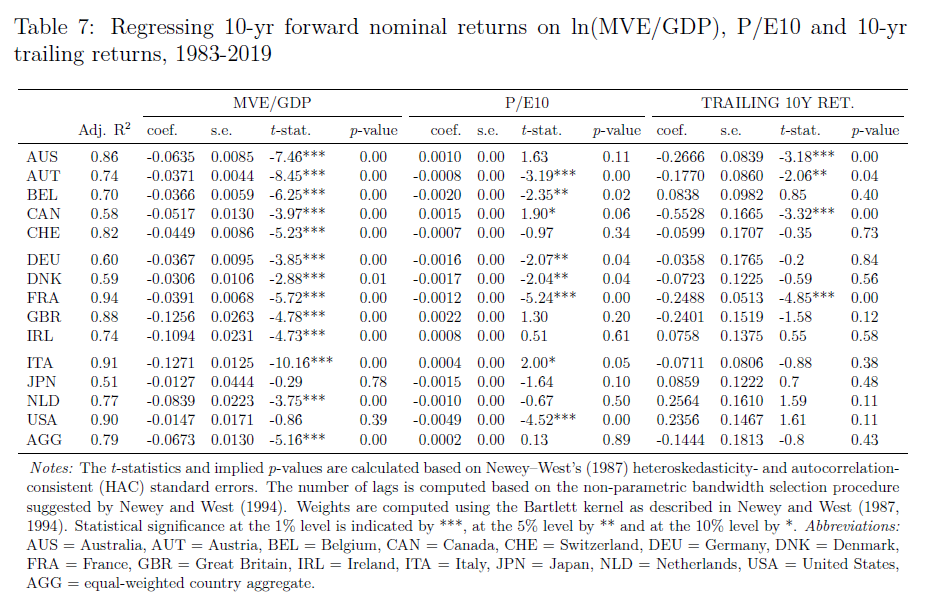

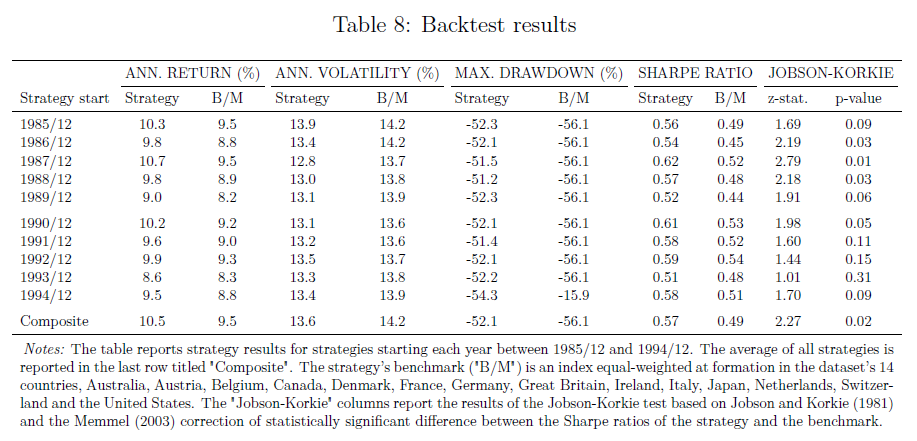

Despite Warren Buffett’s claim that the MVE/GDP ratio is “probably the best single measure of where valuations stand at any given moment,” its predictive ability has been the subject of relatively little academic scrutiny. A novel paper by Swinkels and Umlauft (2022) fills this gap and examines whether the MVE/GDP ratio can forecast international equity returns, which complements the existing research limited to the United States. Their findings can be summarized as follows. First, based on the data from fourteen developed markets going back to 1973, the “Buffett indicator” exhibits superior forecasting qualities over longer time horizons. More specifically, MVE/GDP explains, on average, 83% of the variation in 10-year forward returns, ranging from as low as 42% for Austria to 94% for Great Britain. Second, when the CAPE ratio and the mean-reversion are included in the predictive regression, MVE/GDP remains significant, suggesting that its predictive ability is not subsumed by other popular valuation signals. Most importantly, these research findings can be utilized in practice. A simple trading strategy that invests in countries with the highest model-predicted returns yields statistically significant and economically meaningful alpha over a corresponding buy-and-hold benchmark while experiencing lower volatility and maximum drawdown.

Authors: Laurens Swinkels and Thomas S. Umlauft

Title: The Buffett Indicator: International Evidence

Link: https://ssrn.com/abstract=4071039

Abstract:

Warren Buffett suggested that the ratio of the market value of publicly traded stocks to economic output could identify equity market mispricings. We extend the existing research from the United States to international equity markets by investigating the return-predictive characteristics of the market value of equity-to-gross domestic product for a dataset comprising fourteen countries. The findings corroborate that the “Buffet indicator” explains a large fraction of ten-year return variation for the majority of countries outside the United States. Low ratios have predicted above-average investment returns, while periods of high ratios have, on average, been followed by below-average returns over the subsequent ten-year period. We also compare the “Buffett indicator” to other well-known stock market valuation signals and phenomena, such as the cyclically-adjusted price-to-earnings ratio and mean-reversion in stock returns.

As always we present several interesting figures and tables:

Notable quotations from the academic research paper:

“At the turn of the millennium, Buffett wondered about the exceptional performance as measured by the Dow Jones Industrial Average during the 17-year window between 1981 and 1998 compared to the dismal performance during the equally long period between 1964 and 1981 in spite of a significantly more beneficial macroeconomic setup for the latter period, as economic output increased at more than twice the rate between 1964 and 1981 than between 1981-1998. In two Forbes interviews (Buffett and Loomis 1999, 2001), Buffett suggested that the market value of equity (MVE) scaled by gross domestic product (GDP), which subsequently will be referred to as the MVE/GDP ratio, would have heralded higher returns for 1981-1998 by indicating cheaper valuations for the stock market. In spite of Buffett’s claim that the ratio of market capitalisation to economic output is “probably the best single measure of where valuations stand at any given moment”, its forecast ability has drawn comparatively little academic scrutiny. Our research aims to fill this gap.

The contribution of this paper is threefold. First, we analyse the international evidence of the forecasting ability of the MVE/GDP ratio for equity market returns. Our research complements existing research that is limited to the U.S. (see Lleo and Ziemba 2018 and Umlauft 2020). Our data goes back to 1973, therefore substantially extending the international study by Chang and Pak (2018) that starts in 1997. Second, we compare this predictor to other well-known stock market valuation signals, such as the cyclically-adjusted price-to-earnings ratio (CAPE) of Campbell and Shiller (1988, 1998, 2001) and mean-reversion in stock returns as documented by, e.g., Poterba and Summers (1987), Fama and French (1988), Spierdijk, Bikker and Van den Hoek (2012), Moskowitz, Ooi and Pedersen (2012) and Zaremba, Kizys, and Raza (2020). Third, we provide empirical evidence for real-time profitability over the backtest period 1985-2019, supplementing the existing literature on long-run stock return predictability (see, e.g., Goyal and Welch (2008) and Diris, Palm, and Schotman (2015)).

The analysis conducted in this paper demonstrated that the market value of equity relative to gross domestic product provides a useful tool for investors. The metric possesses strong and robust predictive properties over longer horizons (c. ten years), as market valuations relative to economic output have tended to mean-revert to a long-term equilibrium since 1973, although the latter half of the observation period has witnessed higher MVE/GDP ratios than the period until the turn of the millennium. Further research is required to determine whether this represents a temporary deviation from a long-term equilibrium, or, in fact, may mark a paradigm shift.

Given the forecast quality of the market value of equity-to-gross domestic product ratio as demonstrated in this article, MVE/GDP constitutes an additional input factor for the purpose of equity market valuation and the formation of long-term return expectations. MVE/GDP should not replace conventional valuation measures, such as the cyclically-adjusted price-to-earnings ratio, however. As Campbell and Shiller (1998) point out, conventional valuation measures (i.e. price-to dividend and cyclically-adjusted price-to-earnings ratio) deserve a special place among forecasting variables due to the high-quality and long

availability of data, going back to 1871 for the United States. Rather, MVE/GDP should be seen as a complementary valuation tool by providing incremental information on a non-earnings-based basis. The demonstrably higher explanatory power of P/E10 for the purpose of forecasting excess returns makes a convincing case for using MVE/GDP and P/E10 concomitantly.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend