The Impact of Crowding on Alternative Risk Premiums

Related to all factor strategies …

Author: Baltas

Title: The Impact of Crowding in Alternative Risk Premia Investing

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3360350

Abstract:

Crowding is a major concern for investors in the alternative risk premia space. By focusing on the distinct mechanics of various systematic strategies, we contribute to the discussion with a framework that provides insights on the implications of crowding on subsequent strategy performance. Understanding such implications is key for strategy design, portfolio construction, and performance assessment. Our analysis shows that divergence premia, like momentum, are more likely to underperform following crowded periods. Conversely, convergence premia, like value, show signs of outperformance as they transition into phases of larger investor flows.

Notable quotations from the academic research paper:

“Crowding risk is listed as one of the most important impediments for investing in alternative risk premia. We contribute to this industry debate by exploring the mechanics of the various ARP in the event of investor flows, and study the implications of crowdedness on subsequent performance.

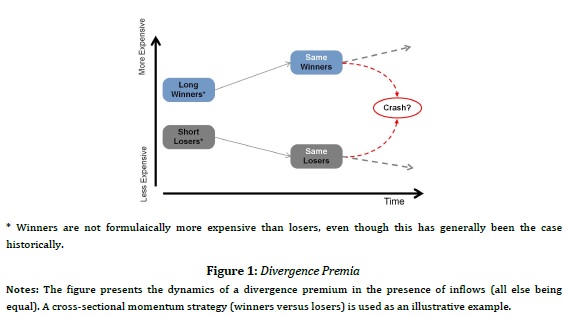

The cornerstone of our methodology is the classification of the ARP strategies into divergence and convergence premia. Divergence premia, like momentum, lack a fundamental anchor and inherently embed a self-reinforcing mechanism (e.g. in momentum, buying outperforming assets, and selling underperforming ones). This lack of a fundamental anchor creates the coordination problem that Stein (2009) describes, which can ultimately have a destabilising effect.

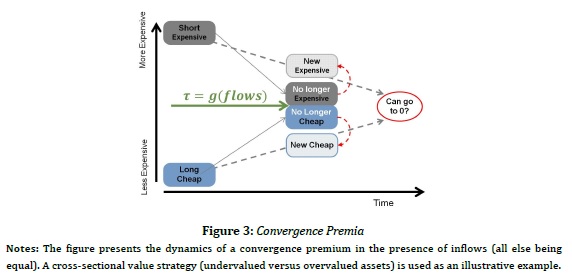

Conversely, convergence premia, like value, embed a natural anchor (e.g. the valuation spread between undervalued and overvalued assets) that acts as an self-correction mechanism (as undervalued assets are no longer undervalued if overbought). Extending Stein’s (2009) views, such dynamics suggest that investor flows are actually likely to have a stabilising effect for convergence premia.

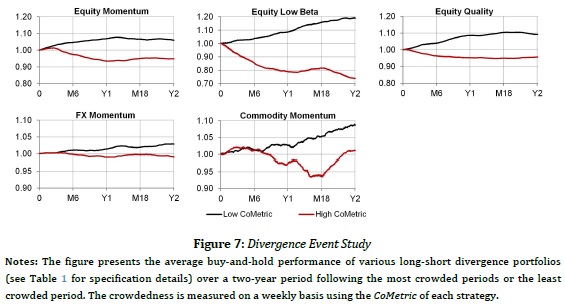

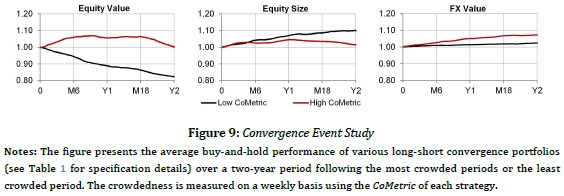

In order to test these hypotheses we use the pairwise correlation of factor-adjusted returns of assets in the same peer group (outperforming assets, undervalued assets and so on so forth) as a metric for crowding.

We provide empirical evidence in line with these hypotheses. Divergence premia within equity, commodity and currency markets are more likely to underperform following crowded periods.

Whereas convergence premia show signs of outperformance as they transition into phases of higher investor flows.

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend