What’s the Size of the Risk Premia (from the Analysts’ Perspective)

The topic of today’s short blog post concerns a subject that’s connected to everybody participating in financial markets worldwide: different subjective return expectations. It is reasonable to have some expected returns you can count on if you are putting your money at risk. But how do they differ between different market professionals? And are return expectations influenced by recessions? We will look closely at financial analysts and their views on risk premia. The main point from the authors of the analyzed paper stresses the idea that analysts are counter-cyclical.

Büsing and Mohrschladt (May 2023) provide evidence on the time-series and cross-sectional properties of analysts’ presumed risk premia. Their new method allows to retrieve these risk perceptions by combining recommendation and target price data.

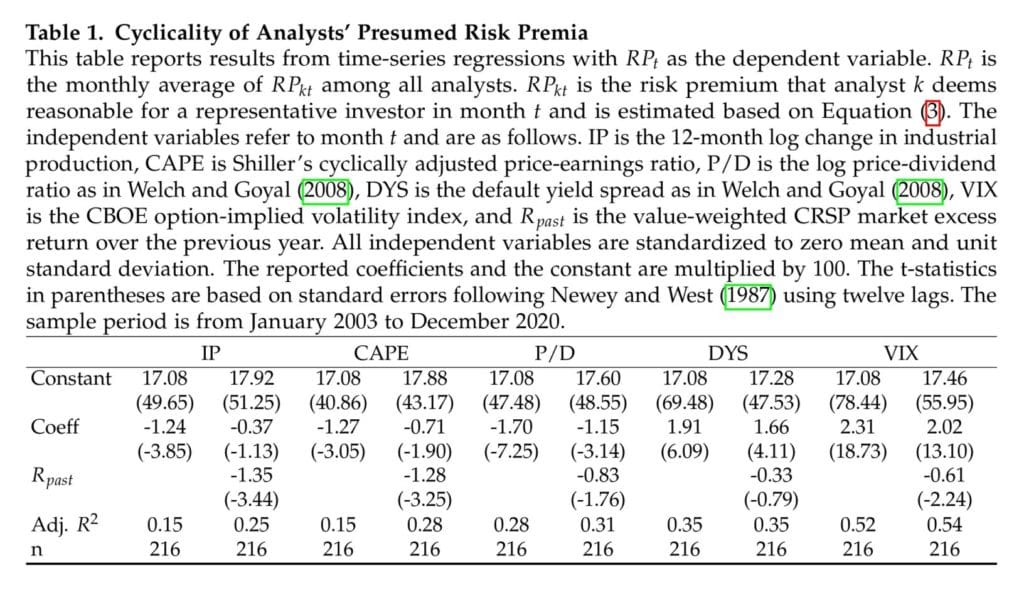

What are the results? In line with rational models explaining market return predictability, the presumed risk premia are comparably high in down-markets, high-VIX periods, and times of low price-dividend ratios. In the cross-section, analysts seem to consider high-beta, small, and value stocks riskier than their low-beta, big, and growth counterparts. Many behavioral theories have been proposed in recent years to explain the time-series predictability associated with cyclical state indicators and size and value effects in the cross-section of realized stock returns. Findings from the paper indicate that these empirical observations partly reflect compensation for risk as implied by corresponding rational models.

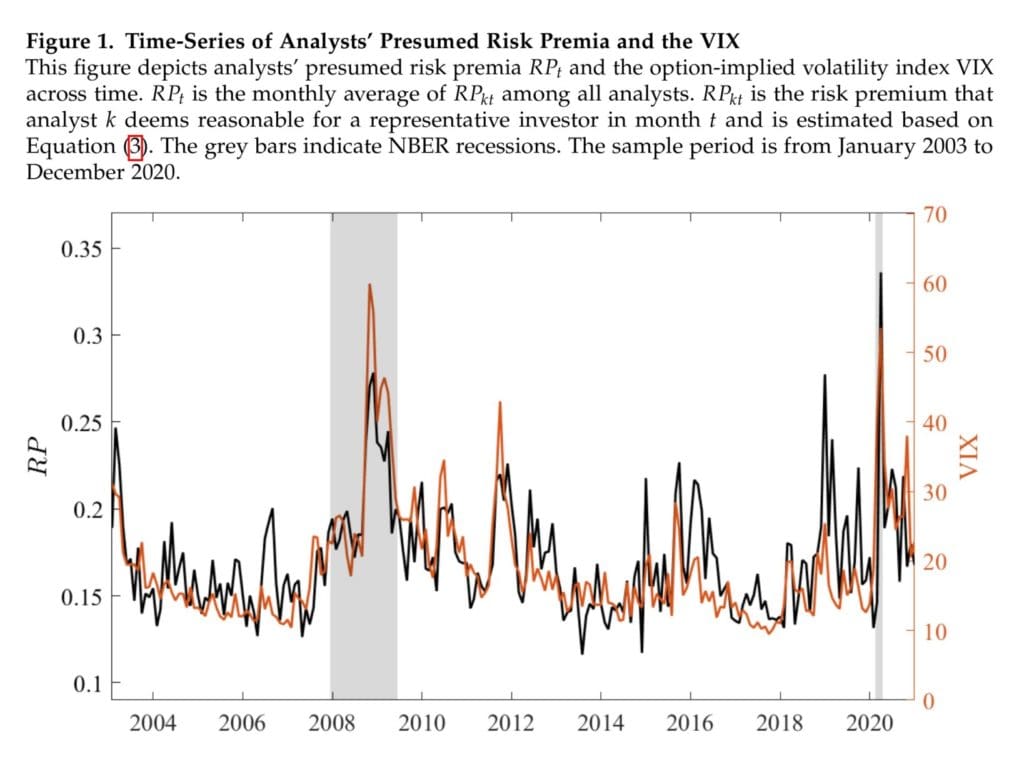

The time-series variation in the presumed risk premium (RPt) that the average analyst deems reasonable for a representative investor; thus, its visual representations, are shown in Figure 1. RPt is clearly not stable over time but rather volatile; during two NBER recessions in the sample period, the global financial crisis and the COVID-19 crisis, RPt rises sharply and peaks. When the recessions are over, RPt returns to moderate levels again. Note the interesting correlation with VIX (72.12% [t = 15.23].).

The most important question at the end is: What’s the annual market price of risk applied by financial analysts? The research paper estimates that it is, on average, 5%, which is a nice fit for the true historical market-wide equity premium over a very long time.

Authors: Pascal Büsing and Hannes Mohrschladt

Title: Risk Premia – The Analysts’ Perspective

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4460200

Abstract:

We examine the time-series and cross-section of stock market risk premia from the perspective of financial analysts. Our novel approach is based on the notion that analysts’ stock recommendations reflect both their subjective return expectations and their perceived stock risk. Thus, we can empirically infer presumed risk premia from recommendations and target price implied expected returns. We show that analysts’ presumed risk premia are strongly countercyclical such that their correlation with the VIX is 72%. Moreover, they predict future stock market returns and are closely related to the price-dividend ratio and other cyclical state variables. In the cross-section, the presumed risk premia are comparably large for high-beta, small, and value stocks lending support to a risk-based interpretation of these characteristics.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“Unfortunately, data on every investor’s stock preferences for a fixed level of expected stock return is not available to academia (and will presumably never be). But at least, we take a small step in this direction by investigating the influential group of financial analysts.

Referring to the time-series of analysts’ presumed risk premia, our findings point toward strong countercyclicality, that is, analysts’ required rate of return is substantially higher following down-markets, in recessions, and during high-volatility periods. For example, the correlation between the option-implied volatility index VIX and the analysts’ presumed risk premia is 72%.

Referring to the cross-section, we find that analysts’ presumed risk premia increase in a stock’s market beta. More specifically, our cross-sectional analyses imply that the annual market price of risk applied by financial analysts equals approximately 5% such that it matches the historical market-wide equity premium quite well. Consequently, our findings support rational asset pricing models such as the CAPM that imply higher risk premia for stocks that show a positive covariance with the market. Moreover, we show that this cross-sectional market price of risk is positively correlated with the VIX.

[E]mpirical analysis [starts] by examining the time-series variation in the presumed risk premium (RPt) that the average analyst deems reasonable for a representative investor. As described in Subsection 2.2.1, we can estimate RPkt by minimizing the sum of squared residuals in Equation (3) for each analyst in every month.8 We then compute the monthly average RPt over all analysts to obtain a time-series of presumed risk premia.

Hence, analysts presume higher risk premia when the market is expected to be comparably volatile. This observation shows that analyst recommendations take into account a typical risk-return tradeoff: in order to bear an increased level of volatility and uncertainty, analysts presume higher risk premia for the representative investor.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend