Why Most Markets and Styles Have Been Lagging US Equities?

Over the past decade and a half, the US equities have set the hard-to-beat performance benchmark. Nearly all of the other countries, no matter if small or big, emerging or developed, have lagged behind. However, what are the forces behind this outperformance? Why did most of the other markets and even investing styles bow to the US large-cap growth dominance? A new paper written by David Blitz nicely analyses the rise of the behemoth.

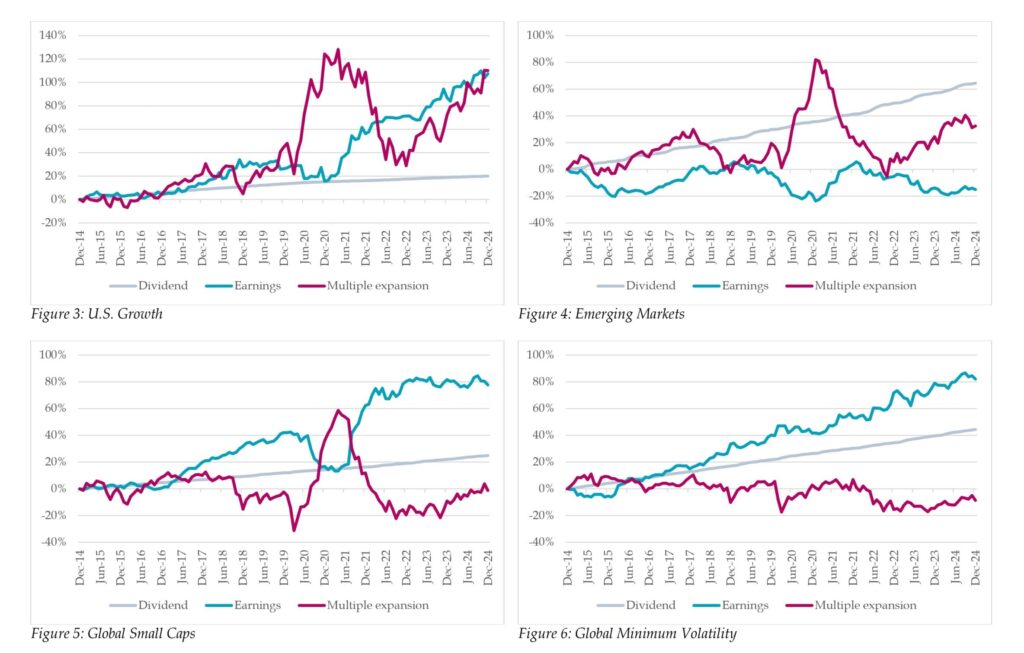

The decomposition of equity returns into earnings growth and multiple expansion provides a powerful lens through which to evaluate market performance. Over the last years, U.S. equities were harnessing robust earnings growth and significant multiple expansion—a potent combination driven by the meteoric rise of big tech names. This framework, rooted in the classic return decomposition formula (Return = Dividend Yield + Earnings Growth ± Change in P/E Ratio), enables investors to separate the intrinsic performance of a company from the market’s sentiment about its future prospects. Such clarity is invaluable, especially when contrasting the exuberant U.S. market with other segments where valuation dynamics and operating performance have followed different trajectories. We can easily review the snapshot of the world’s equity markets and investing styles in the pictures 1 and 2. The US growth dominance is clearly visible.

And what about the other markets and styles?

Emerging Markets (EM, Figure 4) as a whole delivered weak or even negative earnings growth over the past decade. Although valuations increased during this period, the fundamental performance did not support these higher prices, leading to overall underperformance. However, there were notable exceptions within EM (see Figures 1 & 2): Taiwan and India stood out with strong earnings growth and positive multiple expansion, resulting in competitive returns. In contrast, countries like China, Korea, and the EMEA region experienced negative earnings growth and poor market performance, weighing down the broader EM category.

Based on Figure 5, the earnings growth of global small-caps has alternated chiefly between flat periods and rallies, demonstrating an overall upward trajectory. This pattern reflects the inherent volatility within smaller companies—moments of sluggish growth punctuated by rallies that lift fundamental performance. Multiple expansion, however, has only provided a temporary respite when earnings briefly declined, as seen during the 2020-2021 period.

In contrast, global low-volatility stocks have delivered an impressively steady stream of earnings growth year after year, as highlighted in Figure 6. Despite this consistent performance, these stocks remain particularly unloved by investors because their valuations have remained essentially frozen. This divergence between fundamental improvements and stagnant multiples suggests that solid operating results alone may not be enough to capture market enthusiasm without a corresponding shift in investor sentiment.

Summarizing the broader picture, U.S. equities—propelled by an exceptional growth narrative and buoyed by multiples that have soared to record levels—have dominated global indices over the past decade. Meanwhile, other markets and styles, such as European equities, Emerging Markets, value stocks, and low-volatility stocks, appear relatively cheap for different reasons. Specifically, while small-cap and low-volatility stocks have consistently delivered solid earnings growth, they have been hampered by stagnant valuation multiples; Emerging Markets equities, on the other hand, have struggled with weak operating performance despite some compensation from rising multiples.

What’s the main takeaway? History reminds us that dividends and earnings growth are the cornerstones of long-term returns and that valuation multiples tend to mean-revert. With the possibility that the U.S. earnings cycle could (and would) eventually peak—and its premiums on growth stocks might contract— it would be prudent to maintain diversified portfolios that balance exposure across regions, sectors, and styles, thus positioning themselves to capture opportunities regardless of how the next decade unfolds.

Authors: David Blitz

Title: Decomposing Equity Returns: Earnings Growth vs. Multiple Expansion

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5159811

Abstract:

This short article decomposes equity returns into earnings growth and multiple expansion to help understand why most markets and styles have been lagging and are now cheap compared to the US equity market. The breakdown uncovers differing reasons for underperformance: small-cap and low-volatility stocks have delivered solid earnings growth but lagged due to stagnant valuations, while Emerging Markets equities have suffered from weak earnings growth despite rising valuations. For a turnaround, Emerging Markets equities primarily need improved operating performance, especially in China, Korea, and EMEA, while small-cap and low-volatility stocks do not really have a profitability problem but need to regain favor among investors.

As ever, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“Our approach is inspired by the return decomposition formula of John Bogle:

Return = Dividend Yield + Earnings Growth +/- Change in P/E Ratio

The application of this formula to the U.S. equity market shows that stock returns in some decades are driven by earnings growth, while in other decades multiple expansion was the main driver. There can also be decades during which both components deliver or both fail to deliver.

Figure 1 shows the results of our equity return decomposition by index, while Figure 2 contrasts the fundamental return against multiple changes. We consider different regions, some individual countries, small-caps, low-volatility stocks, and value versus growth stocks in different regions.

The total return of U.S. growth stocks stands out most, driven by a combination of the highest earnings growth and the most multiple expansion, again reflecting the rise of big tech. However, the U.S. dominance is so strong that even U.S. value stocks outperformed growth stocks in Europe, Japan, and Emerging Markets. Within the Developed Markets, the weakest operating performance has been delivered by European Value stocks, with earnings essentially flat after ten years. In Emerging Markets, both value and growth stocks had negative earnings growth. EM growth stocks benefited most from multiple expansion, while EM value stocks had a solid contribution from dividends.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend