Sector/industry picking or country picking can be a profitable trading style but is usually much more challenging than it seems at first sight. Building a good trading model requires a lot of research and dedication. Unfortunately, due to the limited numbers of industries and countries, sorting them on aggregate characteristics can wash out important cross-sectional variations in the characteristics and lead to concentrated portfolios prone to noisier realized returns.

In their fresh Dimensional Fund Advisors research piece, Dong, Huang, and Medhat (2023) touch on the question of whether investors should systematically emphasize certain industries or countries to increase expected returns. Their overhead view provides new insights and sums that investors will likely be better off pursuing premiums in the larger cross-section of individual securities and maintaining broad diversification across the smaller cross-sections of industries and countries.

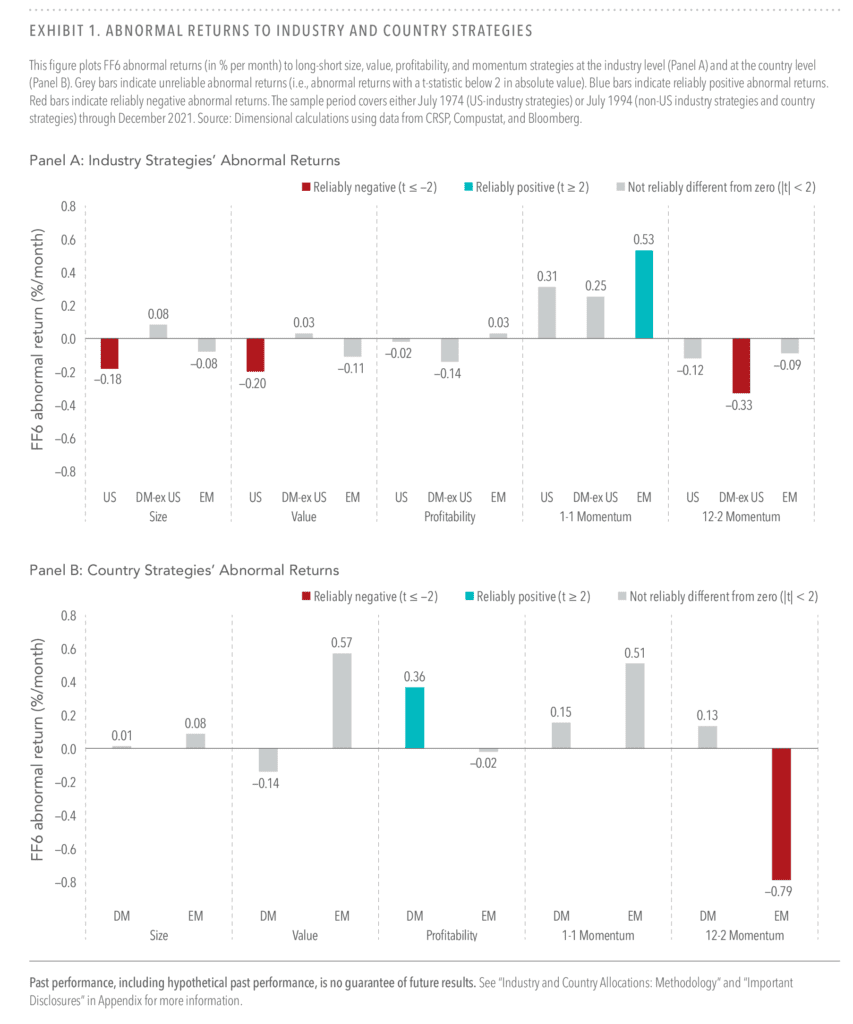

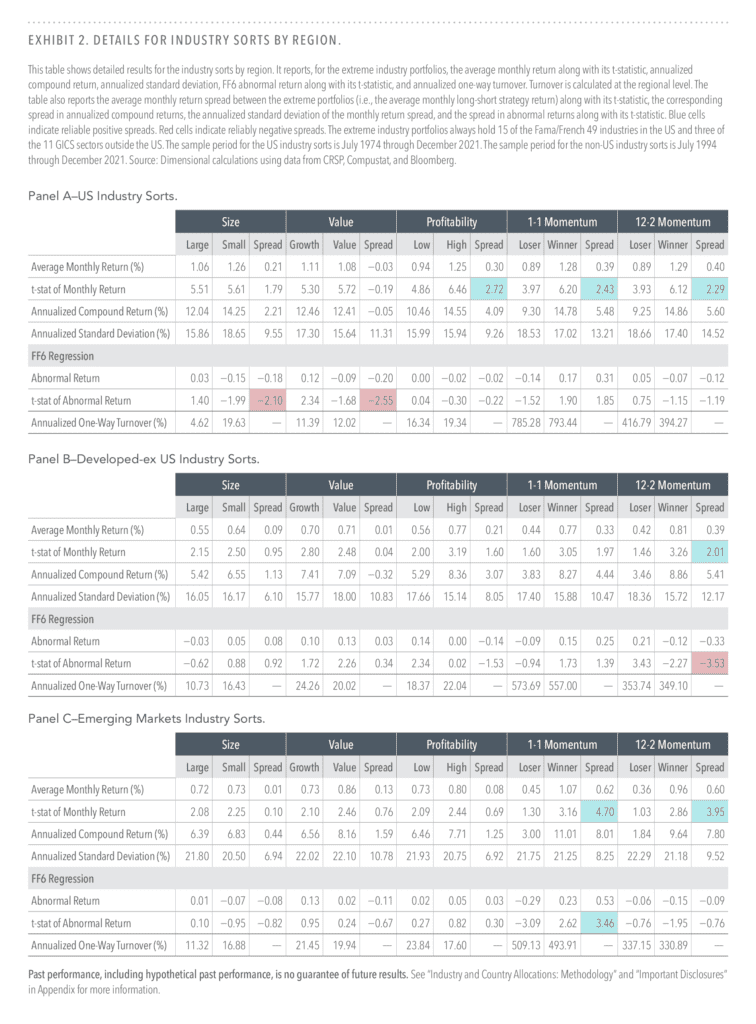

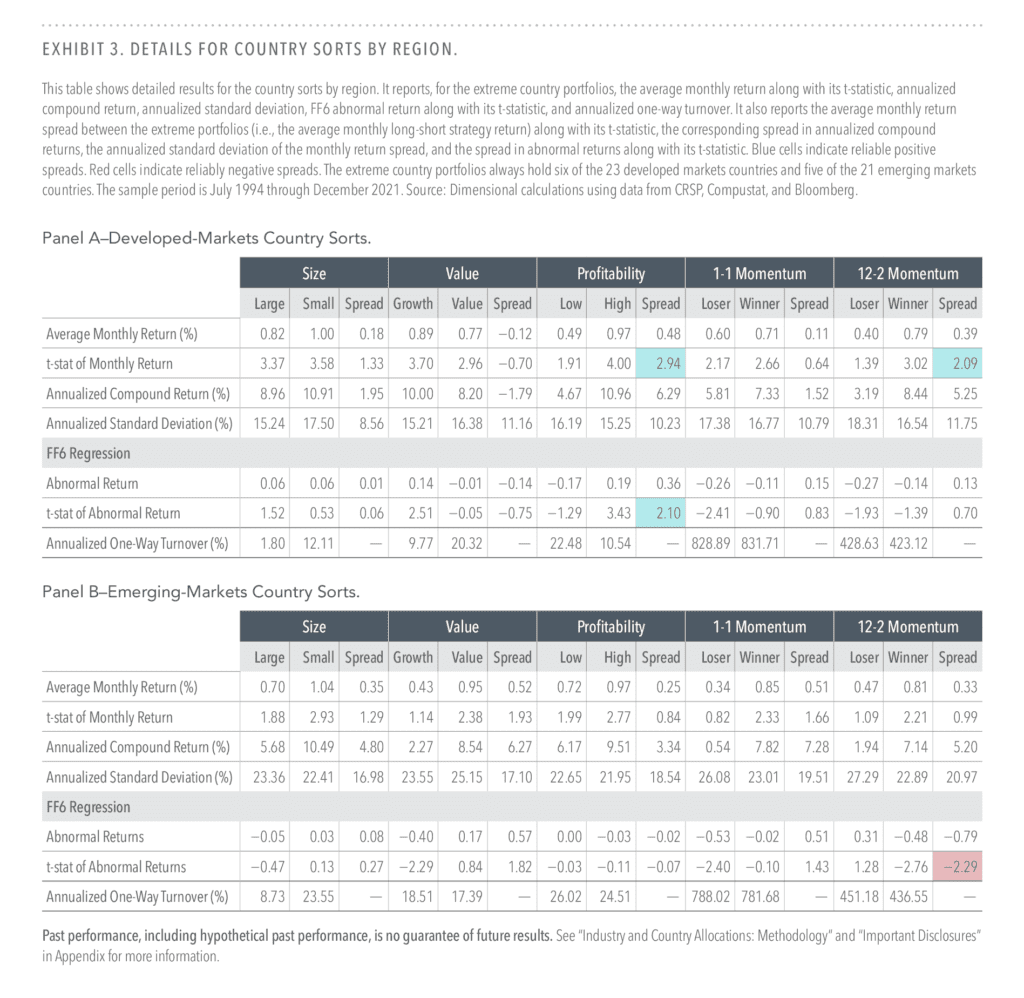

Exhibit 1 provides a simple summary of the results. It shows FF6 abnormal returns to the long-short size, value, profitability, and momentum strategies at the industry level (panel A) and at the country level (panel B). For the industry strategies, only the 1-1 momentum strategy in emerging markets generates a reliably positive abnormal return. Exhibit 2 elaborates on the results for the industry sorts. It reports summary statistics for the long and short sides of the industry strategies along with their spreads in the US (Panel A), non-US developed markets (Panel B), and emerging markets (Panel C). For size, value, and profitability, only the US profitability sort generates a reliably positive average return spread (0.30%/month with a t-statistic of 2.72), and none of the abnormal return spreads are reliably positive. Exhibit 3 shows detailed results for the country sorts. For emerging markets, none of the long-short country strategies earn reliably positive average returns or abnormal returns. For developed markets, the profitability and 12-2 momentum sorts generate reliably positive average return spreads, yet only the profitability strategy earns a reliably positive abnormal return.

The small cross-sections at the industry and country levels can also cause considerable difficulties in capturing premium interactions. Several other papers highlight the importance of accounting for the interactions between the size, value, and profitability premiums in pursuing higher expected returns (Novy-Marx, 2013; Fama and French, 2015; Dai, Saito, and Watson, 2021). Emphasizing smaller, deeper value, and more profitable stocks within a strategy’s investable universe commonly requires a three-way sort. With a small number of entities to sort at the industry and country levels, it can be difficult to avoid overly concentrated positions.

We study the size, value, profitability, and momentum premiums at the industry and country levels in developed and emerging markets. While sorting industries and countries on aggregate characteristics has produced a few reliable average return spreads, the corresponding abnormal returns relative to security-level factors are mostly unreliable or short-lived. Taking positions in industries and countries based on aggregate characteristics can lead to concentrations unjustified by an increase in expected returns and is ill-suited for capturing premium interactions. Using security-level sorts along with diversification considerations appears to be a more viable approach to pursuing higher expected returns.

And; as always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“The idea of labeling entire industries or countries as, say, value or growth, has some intuitive merit. Aggregation, the argument goes, may mitigate security-level noise unrelated to differences in expected returns. On the flip side, because there are far fewer industries and countries than securities, aggregation can wash out important cross-sectional variation in characteristics and result in concentrated positions. Looking at the literature, we find inconclusive evidence on the efficacy of systematic strategies at the industry and country levels.1

We find that industry and country strategies are, in general, inferior to their security-level counterparts for capturing the size, value, profitability, and momentum premiums in both developed and emerging markets. For size, value, and profitability, we find mostly unreliable premiums, the majority of which are subsumed by security-level factors. For momentum, we find that any reliable abnormal returns require high turnover and disappear with less frequent rebalancing, raising doubts about their efficacy in real-world strategies. Our main implication for investors is that using security-level sorts along with sensible diversification considerations is a more viable approach to building systematic strategies.

The US sample consists of all common stocks traded on the NYSE/AMEX/Nasdaq exchanges with available market and accounting data from CRSP and Compustat. The sample covers July 1974 through December 2021, where the start date is determined by the inclusion of Nasdaq stocks. The non-US sample consists of common stocks with available market and accounting data from Bloomberg. The non-US sample covers July 1994 through December 2021, where the start date is determined by data availability.

We construct the industry strategies separately for three regions: the US, non-US developed markets, and emerging markets. Separating developed and emerging markets is common in the literature and further separating the US from other developed markets allows us to use the longer sample period for the US. We sort industries within a country on a given aggregate characteristic and form three country-specific industry portfolios corresponding to low, neutral, and high levels of the characteristic. For regions outside the US, we aggregate the country-specific industry portfolios by their countries’ market capitalizations to regional industry portfolios. This procedure improves diversification and removes any country bets for the non-US industry portfolios. In the US, we use the 49 industries defined by Fama and French (2007), and the three industry portfolios always contain 15, 19, and 15 industries (so that the low and high portfolios each contain roughly 30% of the number of industries).4

We use the low and high portfolios to construct long-short size, value, profitability, and momentum strategies at the industry or country levels. The strategies’ long sides are, respectively, the industries or countries with the smallest size, lowest relative price, highest profitability, and strongest past performance, so we would expect them to have positive average returns.

[…] For the country strategies, only the profitability strategy in developed markets generates a reliably positive abnormal return. Hence, even before a deeper analysis, Exhibit 1 suggests that any benefits to pursuing the premiums at the industry and country levels are few and far between.

[…] While valuation theory suggests we should see positive average return spreads from the industry-level size, value, and profitability sorts, the results presented here show that most of these return spreads are statistically unreliable. This suggests that aggregating from the relatively large number of securities to the relatively few number of industries tends to wash out important cross-sectional variation in the characteristics and lead to more concentrated portfolios prone to noisier realized returns.

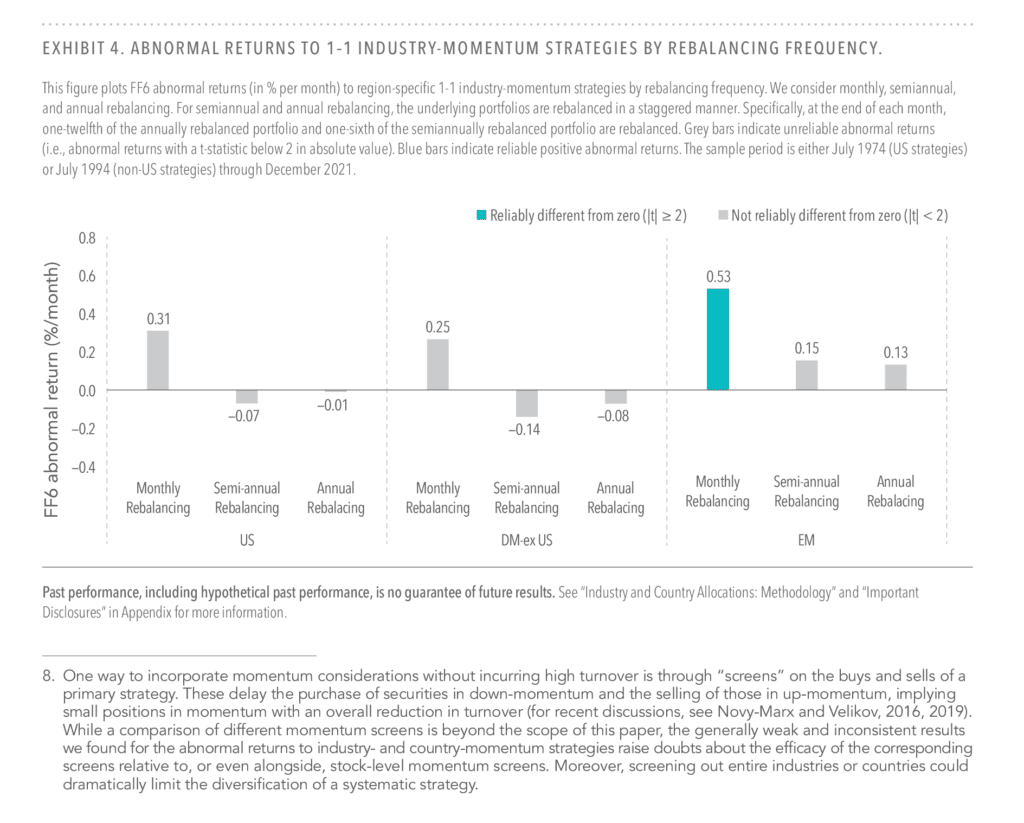

Exhibit 4 illustrates this by showing the 1-1 industry-momentum strategies’ abnormal returns as a function of rebalancing frequency for all three regions. In addition to the standard monthly rebalancing, we also consider semiannual and annual rebalancing. To avoid the latter results being driven by the choice of rebalancing month, the portfolios are rebalanced in a staggered manner. Specifically, at end of each month, one-twelfth of the annually rebalanced portfolio and one-sixth of the semiannually rebalanced portfolio are rebalanced.

Our results thus far suggest industry and country bets do not increase expected returns for an investor already pursuing the premiums at the security level. Nonetheless, the implicit allocations to industries and countries that come with pursuing security-level premiums can still lead to unintended concentrations. This is because some industries and countries tend to show up disproportionately often in one end of the spectrum when sorting on the characteristics.”

Quantpedia is The Encyclopedia of Quantitative Trading Strategies

We’ve already analysed tens of thousands of financial research papers and identified more than 700 attractive trading systems together with hundreds of related academic papers.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.