Can Twitter Images Predict Price Action During FED Announcements?

The Federal Open Market Committee (FOMC) meetings are called the “Superbowl of Finance” due to their significant impact on financial markets. These meetings, where critical decisions about monetary policy are made, attract the attention of traders and investors worldwide. The SPDR S&P 500 ETF Trust (SPY) performac and equity risk premia are closely watched during times close to the rate change announcement, as they can provide insights into market sentiment and potential movements. Crypto has recently become mainstream and has also been accepted as a general asset class. Market participants in that space are also closely watching the results of press conferences and judging the ability of the Fed’s Chair to satisfy the questions of curious reporters on future projections about economic growth and explain anticipated decisions.

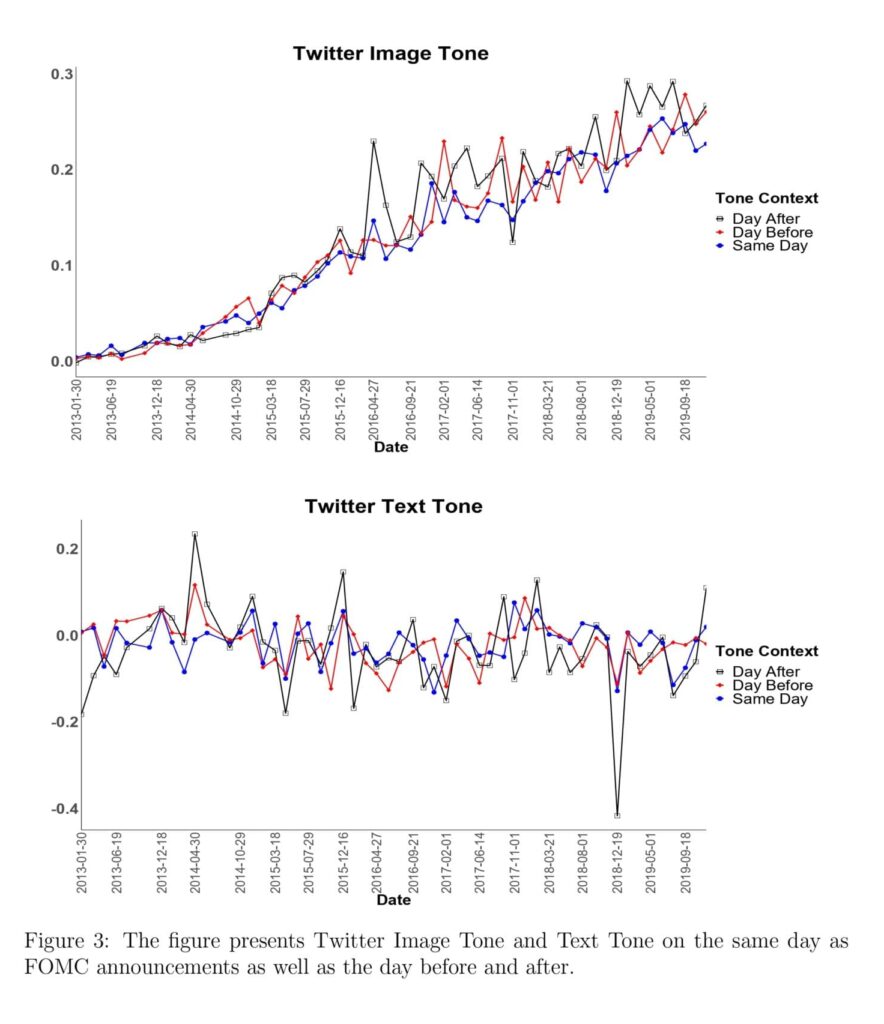

Interestingly, the intersection of social media and text analysis coupled with image analysis provides uncanny insights about monetary policy: recent research has shown that sentiment analysis of Twitter images can predict stock performance during FOMC days much better than text alone. Research paper finds that, in addition to the increased use of images around FOMC announcements, the image tone is significantly and negatively associated with the implied FOMC risk premium and positively associated with realized returns around FOMC announcement days for both equity and Treasury bond markets. Meanwhile, Twitter text tone is not statistically significant with the implied FOMC risk premium or realized excess returns. These results align with the established importance of public sentiment expressed on Twitter and the increasing usage of visual media for expressing opinions. The insignificant results for text tone might be driven by the issues of quantifying the text of tweets due to the increased substitution of images over text and issues with accurate quantification of tweet text due to varied aspects such as emoticons, sarcasm, and slang.

This innovative approach leverages natural language processing and image analysis to gauge market sentiment, offering a new tool for investors to consider. Are days of pure text parsing long gone as they can no longer provide reliable information about general investor public sentiment? While there isn’t a direct strategy derived from this analysis, the regression tables provided in the research offer valuable insights that are insightful for further analysis.

The paper’s introduction highlights the importance of understanding market sentiment and its predictive power, especially during critical financial events like FOMC meetings. Section 3.3 delves deeper into the methodology and findings, making it a compelling read for astute readers interested in social media and financial market relationships.

Authors: Sakshi Jain, Alexander Kurov, Bingxin Li, and Jalaj Pathak

Title: Twitter Image Tone and FOMC Announcements

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4937152

Abstract:

We quantify the image and text tone of tweets around FOMC announcements and report evidence on the increasing use of visual content. We find that it is the tone of images in tweets, rather than the text, that is significantly associated with the implied FOMC risk premium and realized return in the equity and bond markets around FOMC announcements. One standard deviation increase in image tone corresponds to a six basis point decrease in the implied FOMC risk premium. These results are in line with the established importance of public sentiment expressed on Twitter; and with increasing visual media usage in the expression of opinions which feature unconventional elements such as emoticons, sarcasm, and slang. The impact of image tone is robust for financial market-related tweets, varying measures of risk premium, text tone, subsets of tweets, and different time intervals around FOMC announcements.

And as always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“Specifically, we quantify the text and image tone of tweets around FOMC announcements and examine their corresponding impact on implied FOMC risk premiums and realized returns for both equity and bond markets. We quantify the Twitter image tone using the CNN photo classification machine learning model (Obaid and Pukthuanthong, 2022; Jiang et al., 2023). Whereas the Twitter text tone is calculated using TweetNLP (Camacho-Collados et al., 2022). The implied FOMC risk premium used in this study is calculated according to Liu et al. (2022) and is an options-based measure computed around FOMC announcements that minimizes potential contamination caused by other risk factors.1 The study focuses on the period from 2013 to 2019 due to the availability of Twitter data from 2013.2 The seven-year dataset encompasses numerous significant policy actions by the Federal Reserve, including the continuation of quantitative easing, the federal funds rate liftoff, gradual rate hikes, and policy reversals.

As supported by Azar and Lo (2016), Masciandaro et al. (2023) and Schmanski et al. (2023), Twitter is a good proxy for the sentiment of the general public which eventually translates to the sentiment of the market especially around the major economic events such as the FOMC announcements. Further, with the decreasing attention spans, we believe the images are an important means of expressing and receiving information, at par with text, or possibly even more (Obaid and Pukthuanthong, 2022). We argue that images are more closely associated with key information, whereas text tends to offer more comprehensive details. On Twitter, a post may typically include a single image with an additional line of text. This suggests that Twitter users use images to convey the most important message they want to share, while text serves to offer additional context or background information. This structural distinction highlights why images are often more pertinent to the main point and why text provides supplementary, and sometimes less central, details. With these considerations, we hypothesize a negative and significant relationship between Twitter tone and the Implied FOMC risk premium (Liu et al., 2022) and a positive relationship with realized returns (Cieslak et al., 2019) due to Twitter tone being a proxy for market sentiment and hence an increased positive tone/decreased negative tone implying an improved market perception and sentiment for both equity and bond markets.

The negative relationship of image tone with the implied FOMC risk premium is in line with the interpretation of the implied FOMC risk premium established by Liu et al. (2022). According to their definition, the implied FOMC risk premium is negatively associated with positive economic developments, and vice versa. This is because during periods of economic growth such as increases in GDP and consumption growth, the risk premiums are lower due to lower perceived risk, while during periods of economic downturns, the risk premiums are higher to compensate for higher perceived risks. We also find a positive and significant relationship between image tone and S&P 500 index excess returns (Cieslak et al., 2019), as well as the realized returns in bond markets (Adrian et al., 2013). Since risk premium reflects the pessimism in the market, a positive measure of public expression has a negative association with it. However, the excess returns in equity and bond markets reflect the optimism in the market and thus have a positive relationship with the public expression on Twitter.

In contrast to the negative and significant relationship between tweet image tone and the implied FOMC risk premium, the association between tweet text tone and the implied FOMC risk premium is not significant. […]

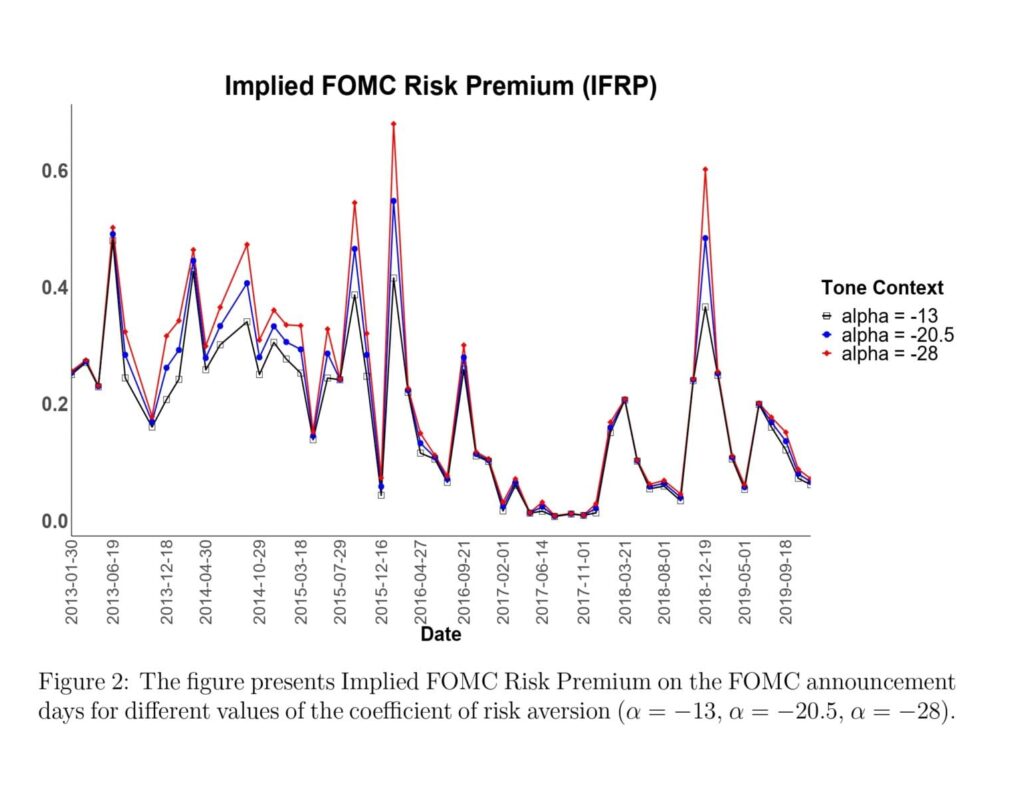

Figure 2 presents the implied FOMC risk premiums (IFRP) for the day of FOMC announcements for the risk aversion coefficients of γ = 5, γ = 7.5 and γ = 10 leading to α = −13, α = −20.5 and α = −28 respectively (Liu et al., 2022; Campbell and Thompson, 2007). The trends reveal pronounced fluctuations, with a notable peak in IFRP using an α of -20.5 in both 2016 and 2018. IFRP values with α of -28 and -13 follow a similar pattern, showing overlapping trends from 2016 to 2018.

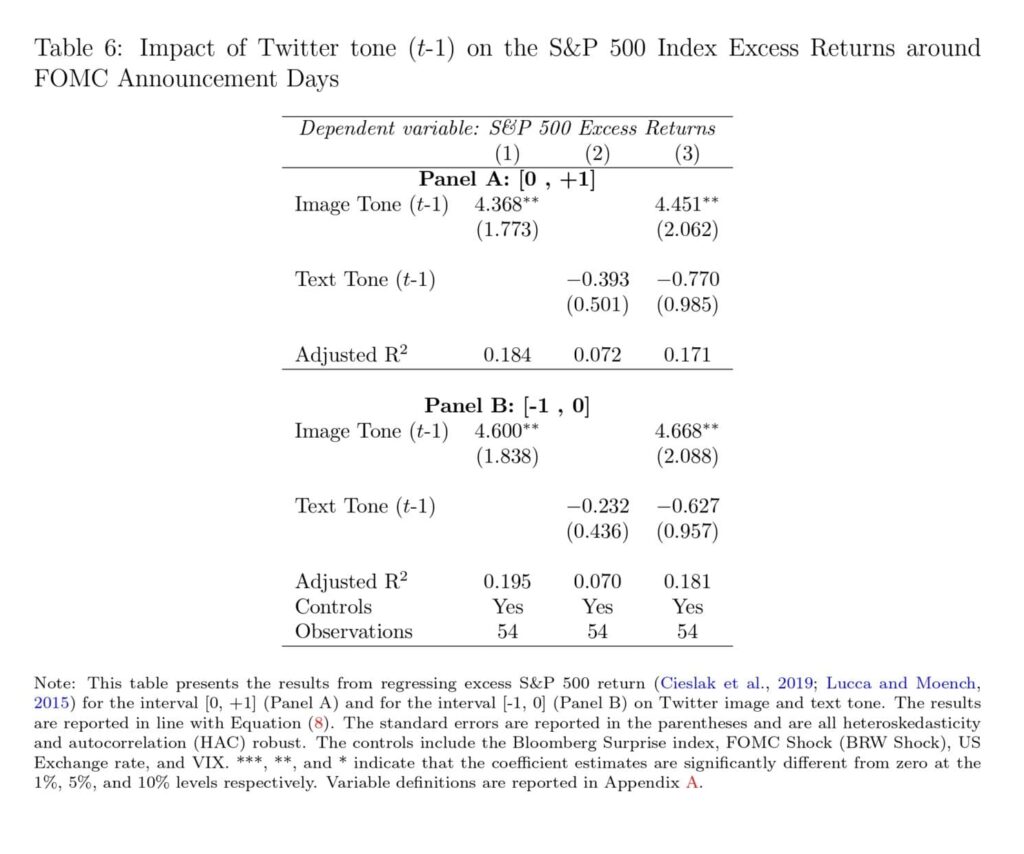

Table 6 presents the impact of Twitter images and text tone on the S&P 500 index excess returns. The excess return is calculated by measuring returns that exceed the risk-free returns of the 30-day US Treasury bills (Cieslak et al., 2019; Lucca and Moench, 2015). Panel A presents the results for the impact of the day t − 1 Twitter image and text tone on the FOMC announcement day excess returns calculated for interval [0, +1] with respect to the FOMC announcement. Similarly, panel B shows the results for the associations between the Twitter image and text tone calculated on the day prior to FOMC announcements and the excess return for the interval [−1, 0].”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend