Building Meta-Strategies with Quantpedia API

Quantitative investors usually start their research by analyzing individual trading strategies. They compare performance, risk, implementation complexity, market exposure, and the economic intuition behind each anomaly. However, once historical equity curves of individual strategies are available, a different research question becomes possible. Instead of asking only which individual strategy looks attractive, we can ask how to allocate capital across a broad universe of strategies.

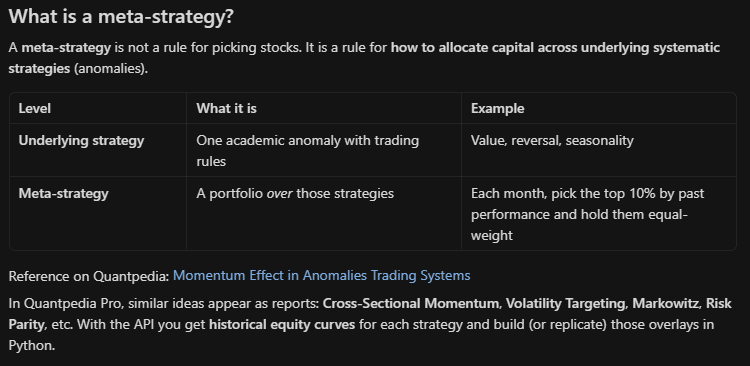

This is where meta-strategies become useful. A meta-strategy does not invest directly in stocks, ETFs, futures, or other financial instruments. Instead, it invests in underlying trading strategies. These strategies become portfolio building blocks, and the researcher can apply allocation rules such as momentum, risk parity, volatility targeting, or mean-variance optimization directly to their return streams.

The Quantpedia API makes this type of analysis practical. It provides access not only to strategy metadata, but also to historical strategy equity curves. Therefore, users can move from strategy discovery to systematic strategy portfolio construction.

From Individual Strategies to Strategy Universes

A traditional quantitative portfolio usually starts with a universe of securities. A researcher may rank stocks by momentum, estimate volatility, optimize weights, or build diversified portfolios based on risk contributions. The same logic can be applied one level higher.

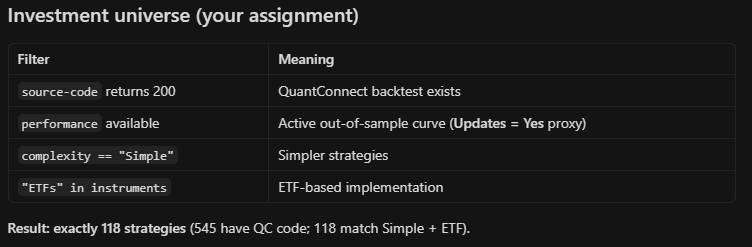

Using the Quantpedia API, researchers can define a universe of strategies based on selected metadata fields. For this case study, we focus on a simple and practical investment universe consisting of investment strategies with simple implementation complexity, ETF-based instruments, available QuantConnect source code, and active performance updates. After applying these filters, the resulting universe contains 118 strategies.

This universe is suitable for a case study because it contains strategies that are relatively simple, ETF-based, and have available implementation code. At the same time, the strategies are actively updated, which makes them more useful for systematic analysis.

The important point is that the API allows the researcher to define this universe programmatically. Instead of manually reviewing hundreds of strategy pages, the user can retrieve the relevant strategy set through API filters and use it as an input for further portfolio research.

What Are Meta-Strategies?

A meta-strategy is a portfolio construction rule applied to a universe of underlying strategies. Each underlying strategy has its own historical equity curve and return stream. The meta-strategy uses these return streams to decide how much capital should be allocated to each strategy over time.

For example, a researcher may ask whether more capital should be allocated to strategies with strong recent performance, whether exposure should be reduced for strategies with high volatility, or whether portfolio weights should be based on correlations and risk contributions. These questions are not about designing a new individual trading rule. They are about designing an allocation framework across already existing strategies.

This is why the availability of strategy equity curves through the API is important. Once these return streams are accessible, strategies can be treated similarly to funds, assets, or factors in a portfolio construction framework.

Case Study: Momentum Across Trading Strategies

As a simple example, we test a cross-sectional momentum overlay applied to a universe of trading strategies. The idea is straightforward. Instead of ranking stocks by recent performance, we rank strategies by recent performance. Strategies that performed best over the recent past are selected for the portfolio, while weaker-performing strategies are excluded.

In this case study, the meta-strategy is rebalanced monthly. At each rebalance date, all strategies are ranked by their cumulative return over the previous six months. The top 10% of strategies are selected, and the portfolio allocates equally across the selected group. The process is then repeated at the next monthly rebalance.

This approach can be interpreted as momentum applied to anomalies or trading systems. The underlying assumption is that strategy performance may show some degree of persistence. If certain strategies are currently working well in the prevailing market environment, they may continue to perform well over the near future.

This does not mean that the best-performing strategy will always remain the best. It also does not mean that momentum is always superior to diversification. The point of the case study is to demonstrate how such a hypothesis can be tested using Quantpedia API data.

Why Strategy Momentum May Work

Momentum is one of the most documented effects in financial markets. It is usually studied at the level of individual securities, sectors, asset classes, or factors. However, similar logic can also be applied to trading anomalies and systematic strategies.

Quantpedia already contains a related strategy, Momentum Effect in Anomalies Trading Systems, which focuses on the idea that anomaly returns may display persistence. The primary source paper behind this idea is Huang’s Real-Time Profitability of Published Anomalies: An Out-of-Sample Test, which studies whether published anomalies can remain profitable out of sample and whether recursively selecting stronger anomaly performers can improve results.

The same theme also appears in broader research on anomaly and factor momentum. Wang, Yan, and Zheng study time-series and cross-sectional momentum in anomaly returns and find evidence that momentum effects can appear in anomaly long-short returns. Ehsani’s work on factor momentum extends the discussion to factor portfolios and shows that momentum across factors can explain a meaningful part of equity momentum. Related studies by Geczy and Samonov, Zaremba and Shemer, and Blitz further discuss momentum across asset classes, factor premia, and the practical caveats of factor timing, including turnover and performance decay.

This research background is important because it connects the case study to a broader empirical question. If anomalies, factors, or trading systems exhibit performance persistence, then it may be possible to build a higher-level allocation model that rotates among strategies according to their recent behavior.

This concept is especially relevant for meta-strategy research. If individual strategies respond differently to changing market regimes, then a dynamic allocation model may help shift exposure toward strategies that are currently better aligned with the environment.

However, this should always be tested carefully. Strategy momentum can increase concentration risk, turnover, and sensitivity to recent market conditions. Therefore, it should be compared against simpler portfolio construction methods.

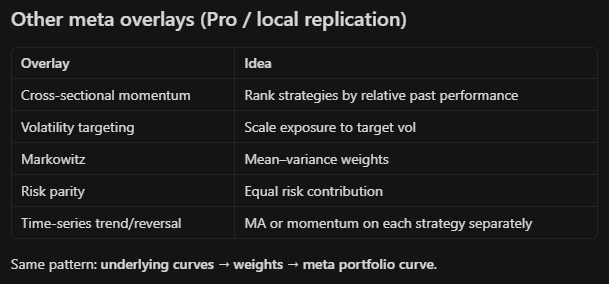

Alternative Meta-Strategy Overlays

Momentum is only one possible example. The same API-based framework can be extended to many other portfolio construction methods. Researchers can apply equal-weight allocation across all selected strategies, volatility targeting to strategy returns, risk parity across strategy equity curves, mean-variance optimization, trend-following overlays, drawdown-based allocation rules, or custom ranking models based on multiple strategy characteristics.

This flexibility is the main advantage of working directly with API data. Once the universe and equity curves are available, the user can define almost any allocation rule and evaluate its historical behavior.

The API therefore allows users to perform meta-analysis on top of Quantpedia’s strategy database. Instead of only asking whether a single strategy is interesting, users can analyze how groups of strategies behave together and how different allocation models affect the final portfolio.

Performance Comparison

To illustrate the framework, the momentum-based meta-strategy can be compared with simpler allocation approaches, such as equal-weight allocation or naive risk parity. The equal-weight portfolio allocates capital evenly across all selected strategies and provides a broad benchmark for the whole strategy universe. The risk parity portfolio attempts to balance risk contributions across strategies, which can help reduce the impact of highly volatile strategies and create a more risk-aware allocation.

The momentum portfolio, in contrast, is more selective. It allocates only to the top-ranked strategies based on their trailing six-month returns.

The comparison highlights the trade-off between diversification and selectivity. A broad equal-weight portfolio is simple and diversified, but it does not react to changes in strategy performance. A momentum overlay is more dynamic, but it can become more concentrated and may experience larger drawdowns during regime shifts.

This is exactly the type of question that meta-strategy research is designed to answer. The goal is not only to identify which allocation method performs best in one backtest, but also to understand the risk-return trade-offs of different ways of combining strategies.

Quantpedia API as a Meta-Research Framework

The broader implication of this case study is that the Quantpedia API can be used as a research framework for strategy-level portfolio construction. Through the API, users can filter strategies by metadata, create custom strategy universes, retrieve historical equity curves, calculate risk and return characteristics, rank strategies by custom metrics, build dynamic portfolios, compare allocation models, and test meta-strategy hypotheses.

This significantly expands the use of the Quantpedia database. The API is not only a tool for retrieving information about individual strategies. It also allows researchers to analyze relationships between strategies and build higher-level models on top of them.

This is useful because recreating hundreds of individual strategy backtests manually would be time-consuming. By accessing strategy equity curves directly, users can focus on portfolio-level research questions without rebuilding every underlying model from scratch.

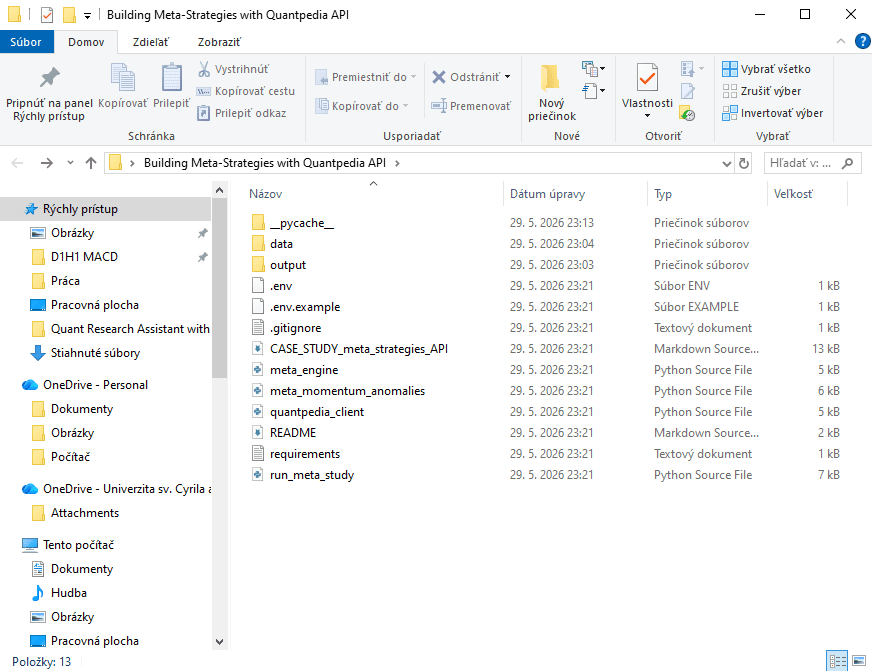

In practice, the API-based workflow can be organized as a compact research project. The main project folder contains the API client, meta-strategy engine, run script, requirements file, environment configuration, cached data, and the written case study. This structure keeps the data retrieval, portfolio construction logic, and final research output separated, which makes the analysis easier to reproduce and extend.

The output folder then contains the generated research files. Besides the final equity curve chart, the workflow can export monthly strategy returns, selected meta-strategy weights, summary metrics, a run summary, and a structured research bundle that can be reused for further analysis or reporting. This makes the framework practical for sensitivity tests, alternative allocation rules, or follow-up client studies.

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend