Too Much Arbitrage Contributes to Overreaction in Post Earnings Announcement Drift

A new financial research paper has been published and is related to all equity long short strategies but mainly to:

#33 – Post-Earnings Announcement Effect

Authors: Li

Title: Does Too Much Arbitrage Destablize Stock Price? Evidence from Short Selling and Post Earnings Announcement Drift.

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3249254

Abstract:

Stein (2009) suggests that too much arbitrage capital exploiting underreaction can lead to overreaction, pushing price further away from fundamental value. I test this hypothesis by investigating the relation between changes in short interest ratio around earning announcement and the subsequent drift return. There are two main findings in this paper. First, my results suggest that too much arbitrage capital does contribute to overreaction (with a t-statistics around 4 on average). These findings are robust to alternative sample periods or length of the window for drift calculation. Second, contrary to the findings in prior literature that show that short sellers mitigate the magnitude of drift, my results show that almost all of this effect are actually contributed by the observations that are more likely to represent overreaction.

Notable quotations from the academic research paper:

"Conventional wisdom believes that as more arbitrage capital starts to trade a given anomaly, any abnormal returns will be eventually eliminated (up to risk and limits to arbitrage) and stock prices will be pushed closer to fundamental values. In other words, the more arbitrage capital, the more efficient the market is likely to become. However, Stein (2009, Presidential Address: Sophisticated Investors and Market Efficiency) questions this simple intuition and shows that when the anomaly does not have a fundamental anchor and when arbitrageurs are not aware about how many other arbitrageurs are trading the same anomaly, arbitrage activity may lead to price overshoot, pushing price further away from fundamental value. Prior literature has very little empirical evidence regarding this implication. Therefore, in this study I try to test whether too much arbitrage capital destabilizes stock price.

The anomaly utilized in this paper is post earnings announcement drift (henceforth, PEAD). Three major advantages associated with PEAD makes it an ideal setting for testing the above implication.

First, it does not have a fundamental anchor so that arbitrageurs do not have a benchmark to gauge the level of under or over valuation. Second, it is one of the most persistent anomalies that are often followed by actively managed hedge funds. Third, it allows me to pin down the time at which arbitrageurs are most likely to take actions – that is, if an arbitrageur was to maximize his profit, he would be more likely to take action in a tight window around the earnings announcement date.

The proxy for arbitrage capital is the change of short interest ratio around earnings announcement date. It is widely documented that short sellers tend to be informed traders who incorporate information and move prices closer to fundamental values. Also note that, in this study, I only focus on announcements with negative earnings surprise since these are the stocks that short sellers are more likely to target.

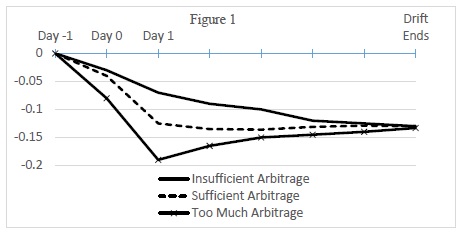

The relation between PEAD and change of short interest ratio is illustrated in figure 1.

Day 0 is the date when the earning announcement is released. Day -1 is one day before and Day 1 is one day after the announcement date. Together, the 3-day window forms the initial response period in which arbitrageurs will trade most intensively. The solid line illustrates the return pattern for negative earnings surprise announcement with insufficient arbitrage capital. In this case, a minor negative return is realized in the initial response period which is followed by a further negative drift. The dashed line illustrates the case when there is sufficient arbitrage capital. In this case, more arbitrage capital adjusts the price to fundamental value faster and therefore a moderate negative return (more negative than the solid line) is realized and no obvious further drift follows. The crossed line illustrates the case when there is too much arbitrage capital. In this case, due to too much arbitraging, a large negative initial response (potential overshoot) is followed by a positive drift (correction).

My findings suggest that too much arbitrage does seem to destabilize stock price. First, holding all else equal, announcements with larger increase in short interest ratio experience significantly more negative initial response (more correction). Next, I show that negative earnings announcements with positive abnormal drift have significantly higher change in short interest ratio than those with negative abnormal drift. Moreover, I find that, holding all else equal, stocks with the largest increase in short interest ratio (SIR decile 10) is almost 10% more likely to result in overreaction than stocks with the largest decrease in short interest ratio (SIR decile 1). In the end, I show that, holding all else equal, change in short interest ratio significantly contributes to overreaction. In particular, within stocks that have positive abnormal drift, the ones that experience the largest increase in short interest ratio average 1.55% higher drift than the ones that experience the largest decrease in short interest ratio. Robustness tests show that my results are not likely to be driven by extreme values in abnormal drift, particular year observations, or length of window for return calculations."

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend