A Deeper Look into Factor Momentum

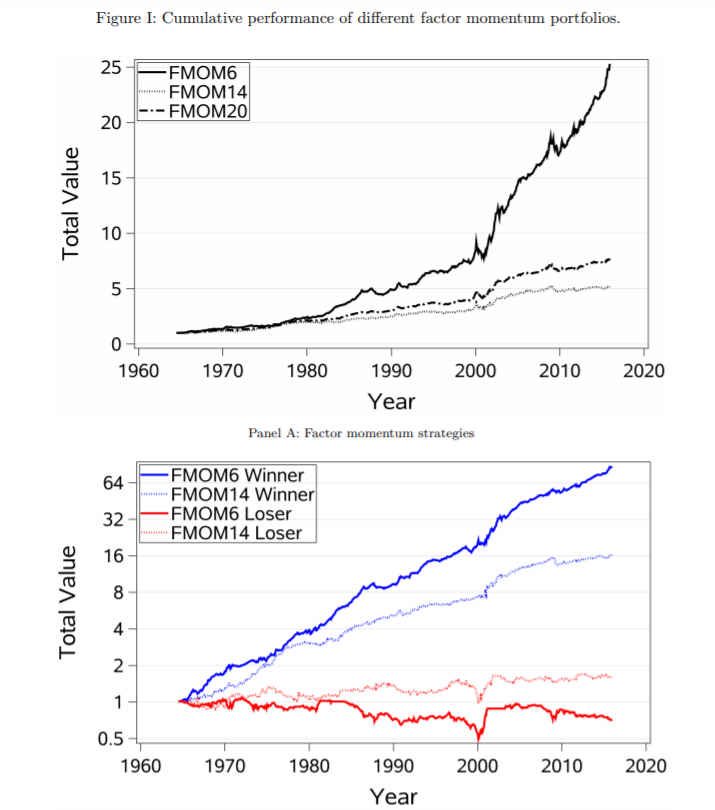

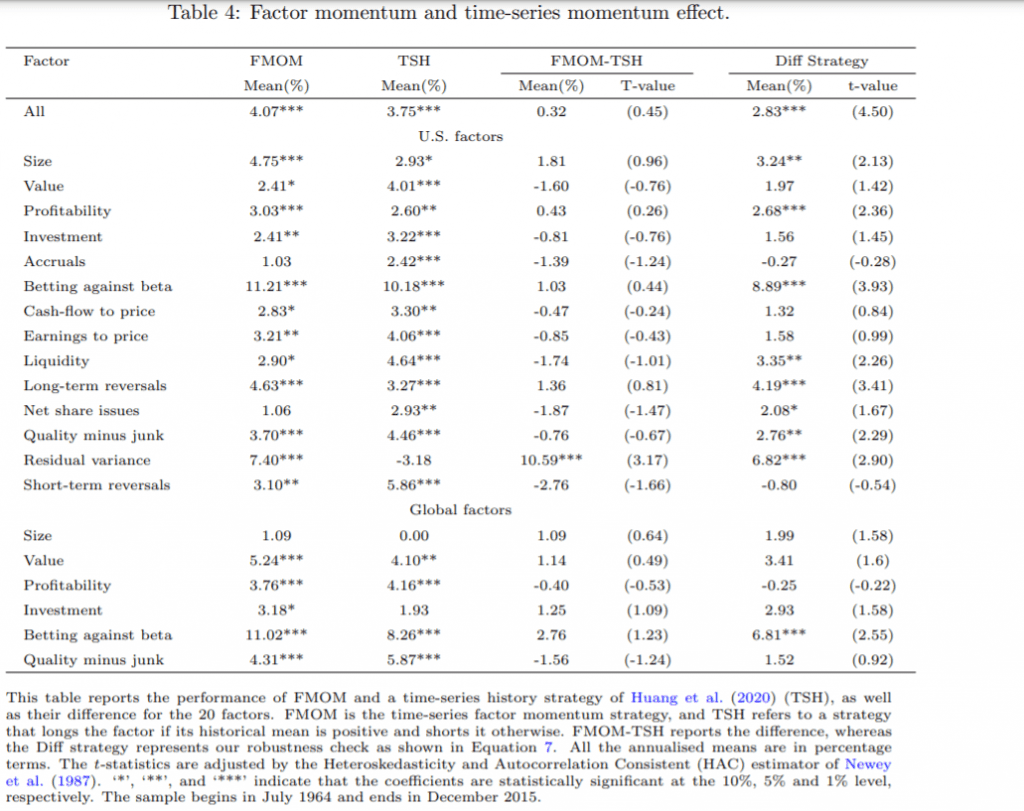

Momentum seems to be present everywhere and based on academic studies, it is even hard to find assets where the anomaly does not work. Among the large number of research papers related to momentum, the discovery of factor momentum is still relatively new. It is a truly important finding in the world of systematic strategies – there seems to be a return continuation among factors. The novel research of Fan et al. (2021) builds on the recent academic research and shows that, after all, the factor momentum might be different. To be more precise, the authors show that looking at the universe of 20 factor strategies, the factor momentum seems to work and can span individual equity momentum strategies (standard momentum, industry momentum and intermediate momentum). However, the factor momentum is mostly driven by only six factor strategies, and the return continuation of the remaining factors is weak. Additionally, those fourteen non-return continuation strategies cannot span the momentum effects mentioned above. Therefore, the results show that the factor momentum works on the aggregate but individually works much better. In fact, the factor momentum return of the six return continuation factor is significantly better compared to the rest or buy-and-hold portfolio. Moreover, the authors have also identified that the “best” factor momentum strategy is the Betting against beta and conclude that the reason is the unique weighting scheme utilized by the factor. The beta weighting assigns a higher weight to smaller companies, where the momentum tends to be stronger. Overall, the research paper is an important extension of the factor momentum literature.

Authors: Minyou Fan, Youwei Li, Ming Liao and Jiadong Liu

Title: A Reexamination of Factor Momentum:How Strong is It?

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3844484

Abstract:

Recent studies have shown that most financial market anomalies exhibit a momentum effect. Based on a dataset covering 20 factors, we find that the factor momentum effect is weak in general. Six factors exhibit strong return continuation and dominate the factor momentum portfolio, while the remaining 14 factors do not. The choice of factors affects the ability of factor momentum to explain individual stock momentum. We uncover why the betting against beta factor exhibits the strongest factor momentum. This is because of its unique rank weighting scheme, whereas all the remaining factors are based on value-weighted portfolios.

As always we present several interesting figures and tables:

Notable quotations from the academic research paper:

“A factor momentum strategy is long recent top-performing factors and short poorly performing factors. Therefore, it is by nature a type of factor timing strategy. Recent literature has shown that factor momentum has significant investment performance compared to traditional individual stock momentum (Gupta and Kelly, 2019) and that factor momentum can explain both individual stock momentum and industry momentum (Arnott et al., 2019, Ehsani and Linnainmaa, 2021).

This study examines the strength and profitability of factor momentum based on a universe of 22 financial market anomalies following Ehsani and Linnainmaa (2021). We confirm the main findings in Arnott et al. (2019), Ehsani and Linnainmaa (2021) that factor momentum exists as a whole. We take a step further and examine the pervasiveness of factor momentum effect at individual factor level.

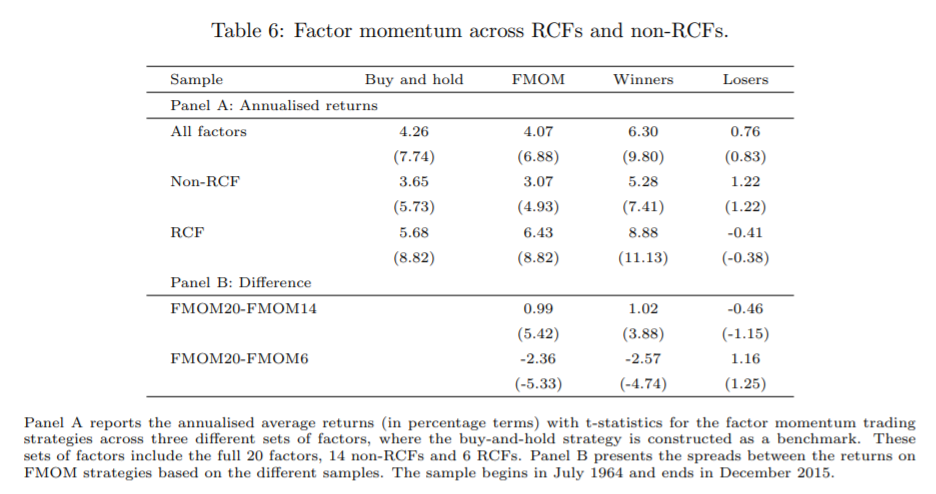

We find that only six factors in our sample show a strong momentum effect and dominate the factor momentum portfolio, whereas the return persistence of the remaining factors is weak. We call these six factors return continuation factors (RCFs) and the remaining factors non-RCFs. We

find that the six RCFs can explain individual stock momentum and industry momentum, while the explanatory power of non-RCFs is weak. Therefore, we conclude that factor momentum may be specific to a certain set of factors but does not apply to all of them. This is especially the case with the betting against beta (BAB) factor, which account for more than 25% of the total factor momentum profits. We argue that this is because of its unique rank weighting scheme instead of the conventional value-weighted portfolio. We find that there is a large variation in return persistence across different factors. For each factor, we use three tests, two time-series regressions and one return decomposition model, to examine its return persistence. The results suggest that only six factors (RCFs) exhibit strong

time-series return persistence, whereas the remaining 14 factors (non-RCFs) do not.

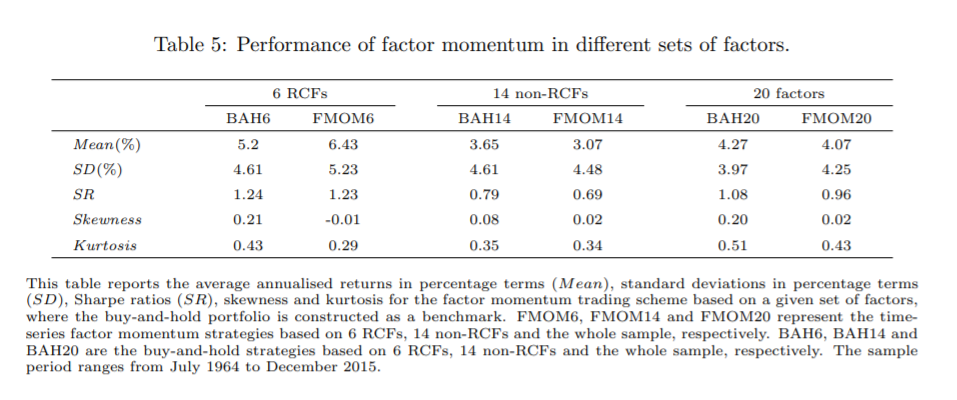

Based on the above findings, we decompose the entire sample into two sub-samples: the six RCFs with strong return persistence and the 14 non-RCFs that show weak return persistence. The momentum profit generated by the RCFs (6.43%) is substantially greater than the profit of either the portfolio with the 14 non-RCFs (3.07%) or the entire portfolio with 20 factors (4.07%). The factor momentum across RCFs accounts for 48.03% of the profits of the factor momentum portfolio sampling all 20 factors. The six RCFs dominate the profitability of the factor momentum portfolio, while the 14 non-RCFs contribute much less. These findings are robust to the consideration of

different formation period and holding period combinations.

Among the 20 factors, the betting against beta factor of Frazzini and Pedersen (2014) makes the largest contribution to the FMOM profits. We find that the strong momentum effect of BAB stems from its unique rank weighting scheme, whereas all the other factors use the value-weighted

portfolio in our sample. This challenges an intuitive hypothesis that momentum in anomalies are caused by their stock selection mechanism. Our finding sheds light on a future research question: is the weighting scheme in financial anomalies causing factor momentum?”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend