Are Funds Flows Influenced by Mortality?

Countries from the majority of the developed world face one challenge: Their population is steadily aging; the average age of individuals has been rising over recent periods. The United States is not different in this sense. Whenever there’s a never-inevitable reaching of higher ages, people reconsider their choices and often cut on riskier ones. These preferences also have interesting implications on the investment decisions of most humans with a limited timespan on planet Earth, thus impossibly having an infinite investment horizon, as would Buffet quip. As we are not Homo economicus but rather emotionally-driven creatures, we all face many different challenges. It is upon us how we deal with them; often not perfectly or optimally, even if we are unaware of it. Still, it is generally possible to model the probabilities of each given possibility and predict its outcome. Would people take fruits of their hard investing labor and hopefully enjoy sweet profits during our old age to increase the quality of their life?

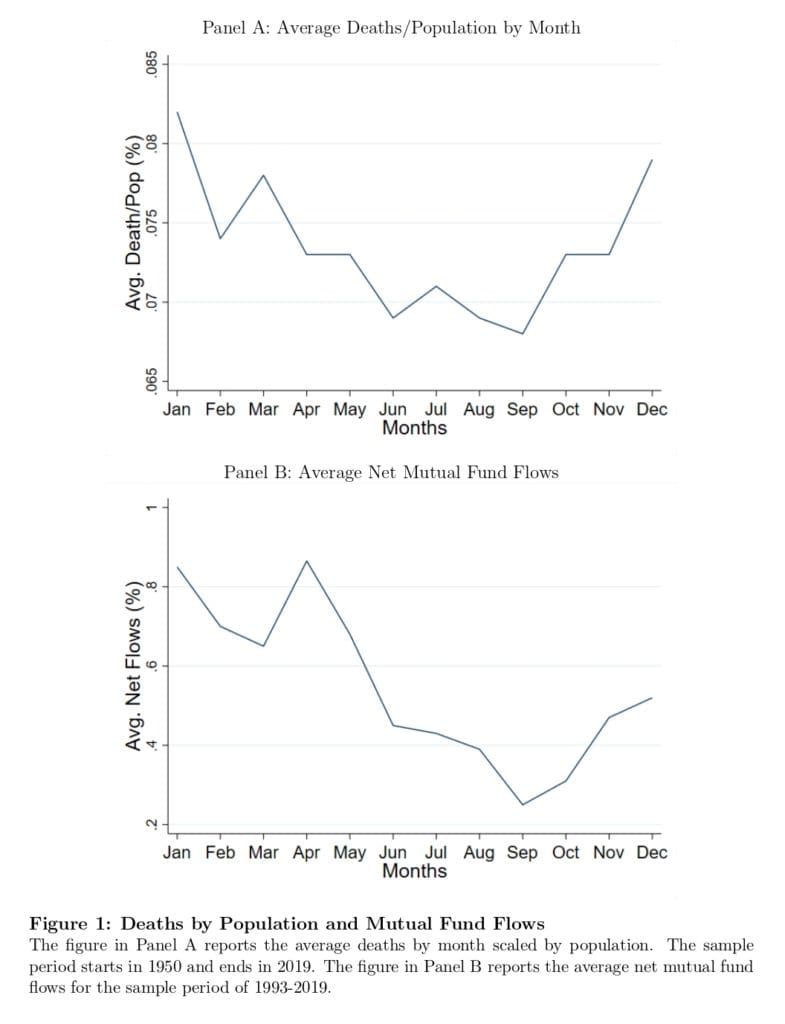

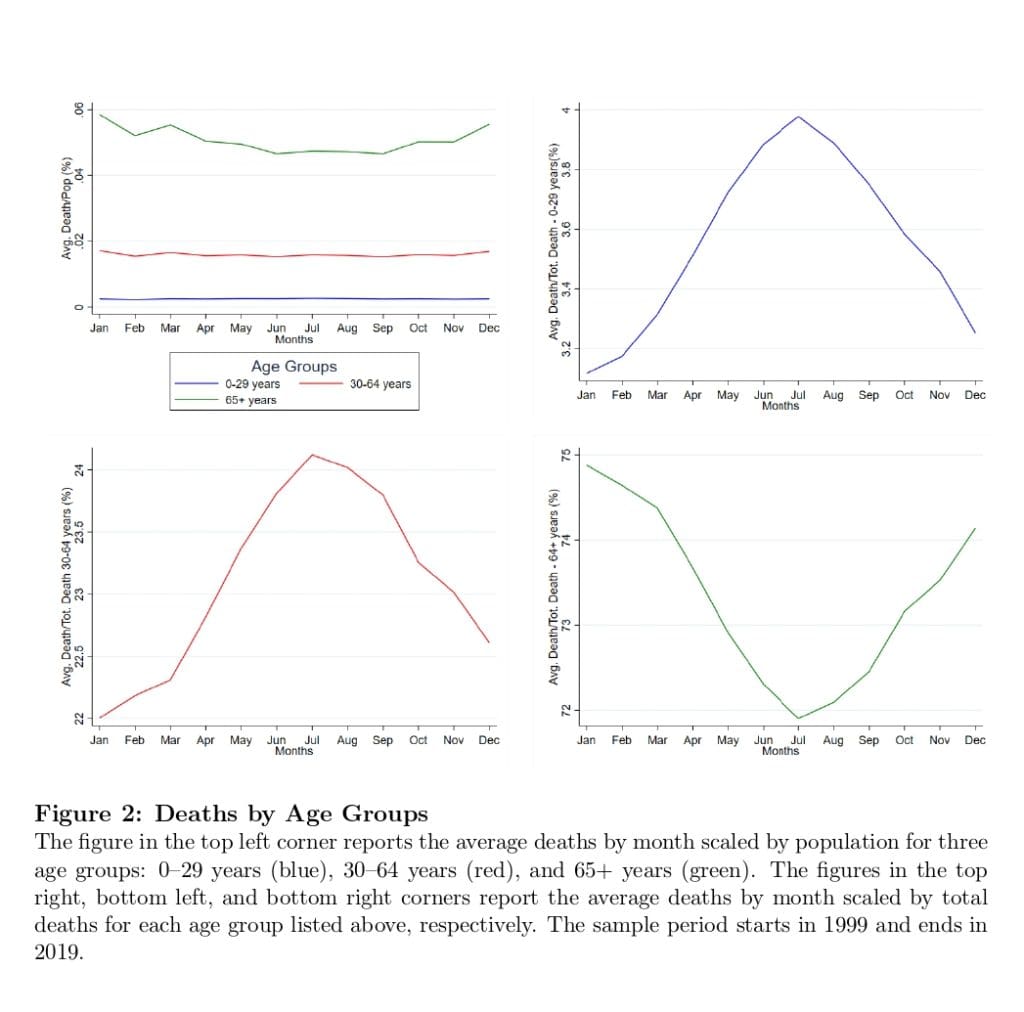

Deleted: Specifically, Kumar, Rantala, and Rizzi from University of Miami (December 2022) have looked into if time variation in mortality rates may have a predictable impact on aggregate mutual fund flows and asset prices and presents us with the subject of modeling demographic processes, which are pretty finely predictable (see figures below). Is there a potential link between demographic changes associated with aging and aggregate financial market outcomes? Their key conjecture is motivated by the observation that elderly people regularly liquidate their mutual fund holdings. What we would like to point out and find extremely important if the status quo of the rising aging average and median status continues is that the presented effects of aging-induced demographic changes in financial markets that could impact the mutual fund industry and those affected stock prices would continue.

As a result, periods with high mortality rates would be associated with higher net fund inflows because aggregate withdrawals would decline. And these effects would be more prominent among funds that cater to older investors, such as high dividend yield and high bond allocation funds. Periods with high mortality rates are associated with more positive net mutual fund flows, and these effects are stronger among high dividend yield and high bond allocation funds. That can be nicely seen from the presented figures. They also find that high mortality exposure stocks consistently earn abnormal returns during abnormal mortality months. Results give a prominent disclaimer: “This strategy is not tradable without a mortality prediction model, but the results demonstrate the asset pricing implications of mortality.”

Authors: Alok Kumar, Ville Rantala, Claudio Rizzi

Title: Mortality, Mutual Fund Flows, and Asset Prices

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4310155

Abstract:

Motivated by the observation that elderly liquidate their mutual fund holdings regularly, we examine whether mortality patterns have a predictable impact on aggregate mutual fund flows and asset prices. Our key conjecture is that periods with high mortality rates would be associated with higher net fund inflows because aggregate withdrawals decline. Consistent with our conjecture, we find that fund inflows are more positive during high mortality months, even after accounting for known seasonality in fund flows. This relation is stronger among funds that cater to older investors, such as high dividend yield funds and high bond allocation funds. We also find that high mortality exposure stocks consistently earn abnormal returns during abnormal mortality months. Collectively, our evidence indicates that mortality-induced demographic shifts impact the mutual fund industry and stock prices.

As always we present several interesting figures and tables:

Notable quotations from the academic research paper:

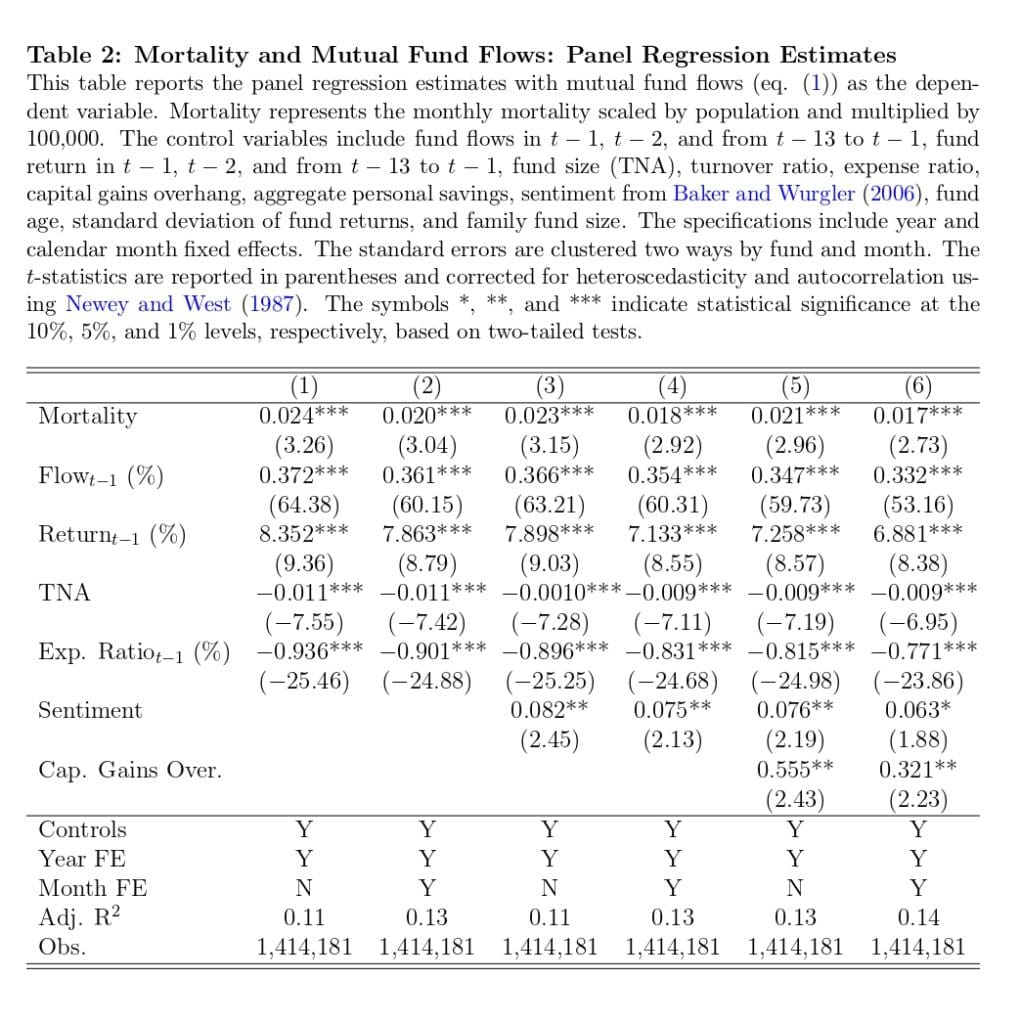

“We start by analyzing the relation between mortality and mutual fund flows by estimating panel regressions that explain mutual fund monthly net inflows. Our sample period is from 1993 to 2019. We exclude the post-2019 years because it is very difficult to separate the wide-ranging idiosyncratic effects of the pandemic from the systematic impact of mortality during the pandemic period. […] We find that the coefficient on the mortality rate is 0.021 with a t-value of 2.96. This evidence indicates that a one standard deviation increase in mortality is associated with a 0.189% increase in fund net inflows. The coefficient remains statistically significant when we include calendar month fixed effects, which control for regular seasonality in fund flows and mortality rate. When they are included, the coefficient is 0.017 with a t-value of 2.61.

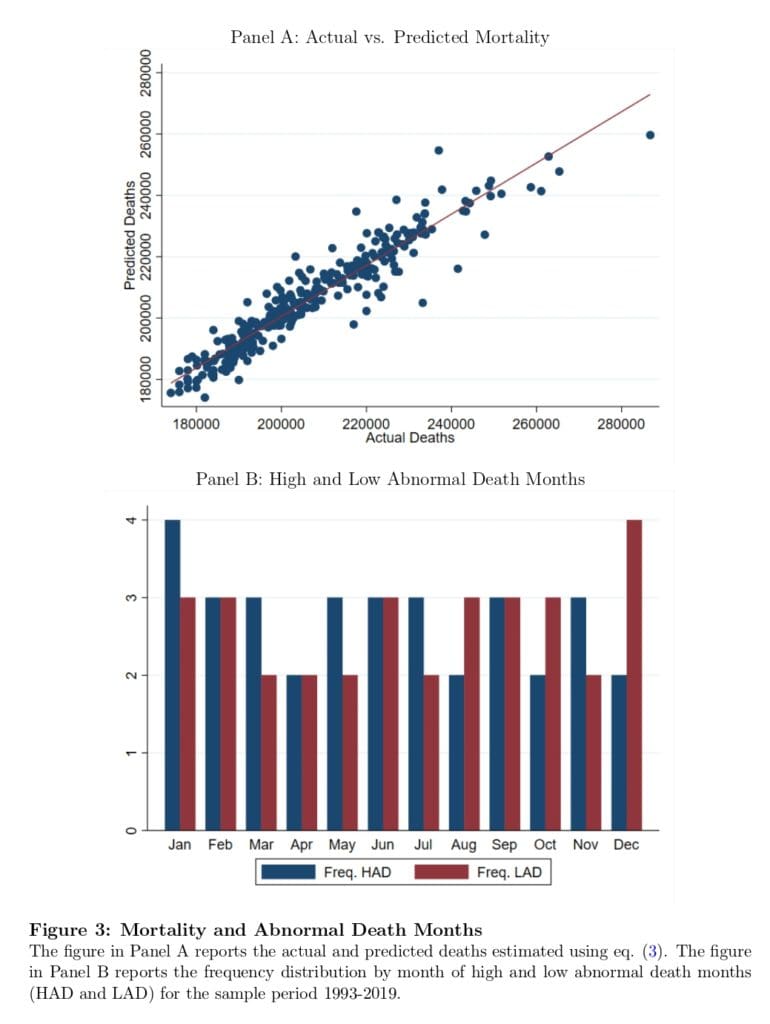

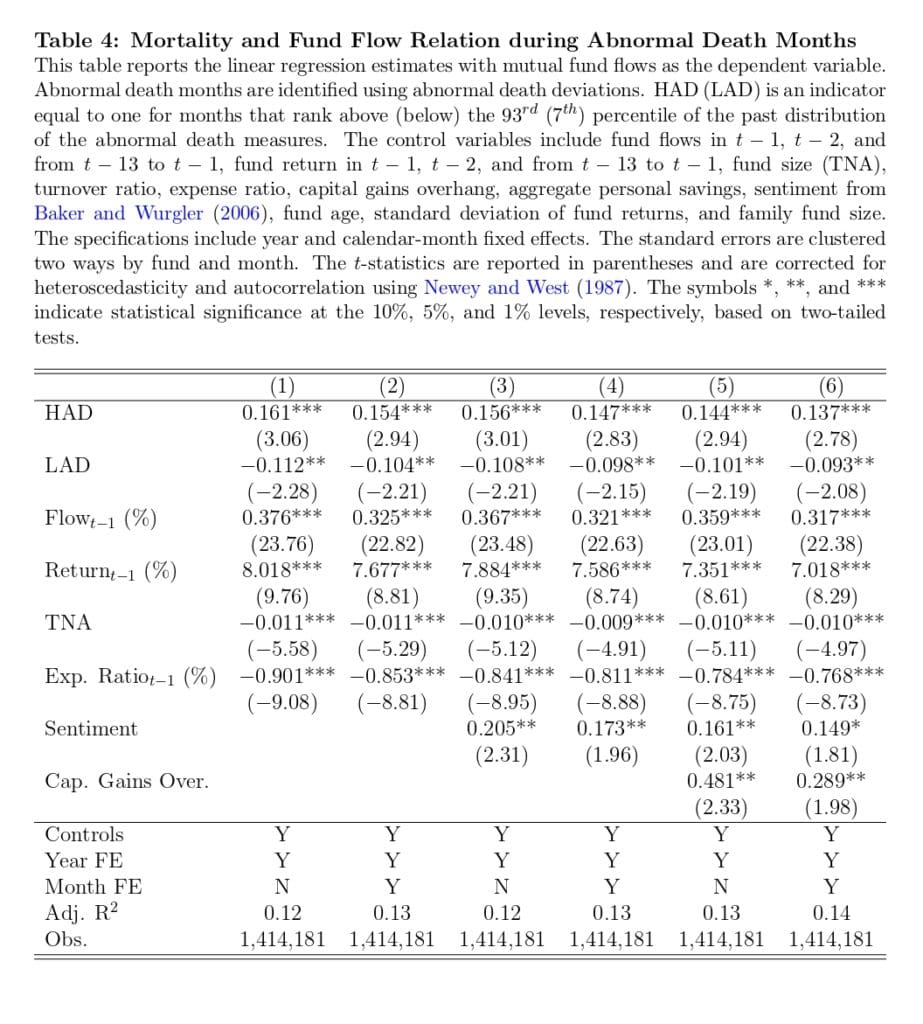

We categorize high and low abnormal mortality months by comparing the scaled abnormal deaths to the empirical distribution of abnormal deaths for the same calendar month. We define a month as a high abnormal mortality month (HAD) if abnormal mortality is higher in no more than one of the past 15 observations for the same calendar month and as a low abnormal mortality month (LAD) if it is lower in no more than one of the past 15 observations for the same month.4 These thresholds correspond to the 7th and 93rd percentiles of the abnormal mortality distribution during the past 15 years. The HAD and LAD months are evenly distributed across calendar months. On average, there are three HAD and LAD observations for each calendar month within our sample period and no month has more than four or less than two observations in either category.

We estimate panel regressions explaining mutual fund monthly net inflows with dummies for the HAD and LAD months. The regressions include the same control variables as our previous specifications. In the full specification with month fixed effects, the coefficient on HAD months is 0.137 with a t-value of 2.78 and the coefficient on LAD months is −0.093 with a t-value of −2.08. These coefficients imply that mutual fund net inflows are 0.14 percentage points higher during high abnormal death months and −0.09 percentage points lower during low abnormal death months. In dollar terms, the effect suggests that, during HAD months, mutual funds experience an estimated net $2.15 billion increase in flows.5 For LAD months, we estimate a net $1.46 billion decrease in flows.6

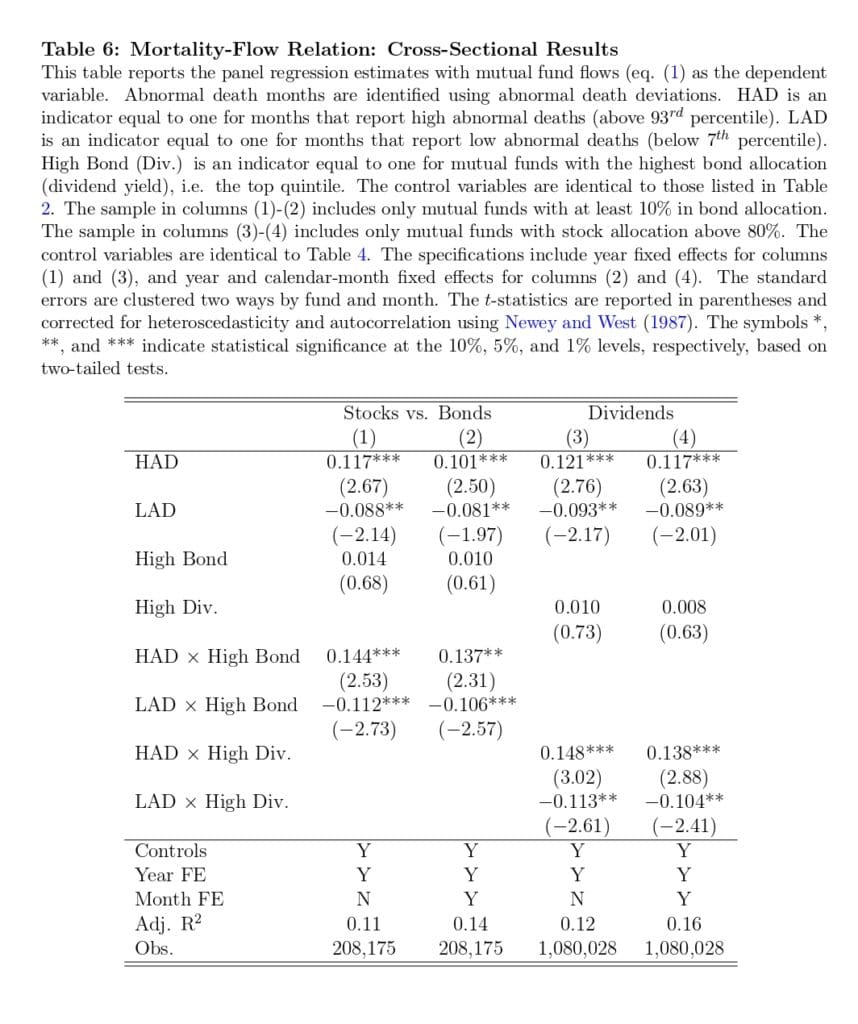

In the cross-section, we find that funds with characteristics that are favored by older investors are particularly sensitive to mortality. We interact the HAD and LAD dummies separately with an indicator dummy for funds with high bond allocation and for funds with high dividend yield. The HAD interaction terms are positive and statistically significant and the LAD indicators are negative and statistically significant. Time-series regressions at the mutual fund level also provide evidence that high dividend yield and high bond allocation funds are more sensitive to mortality.

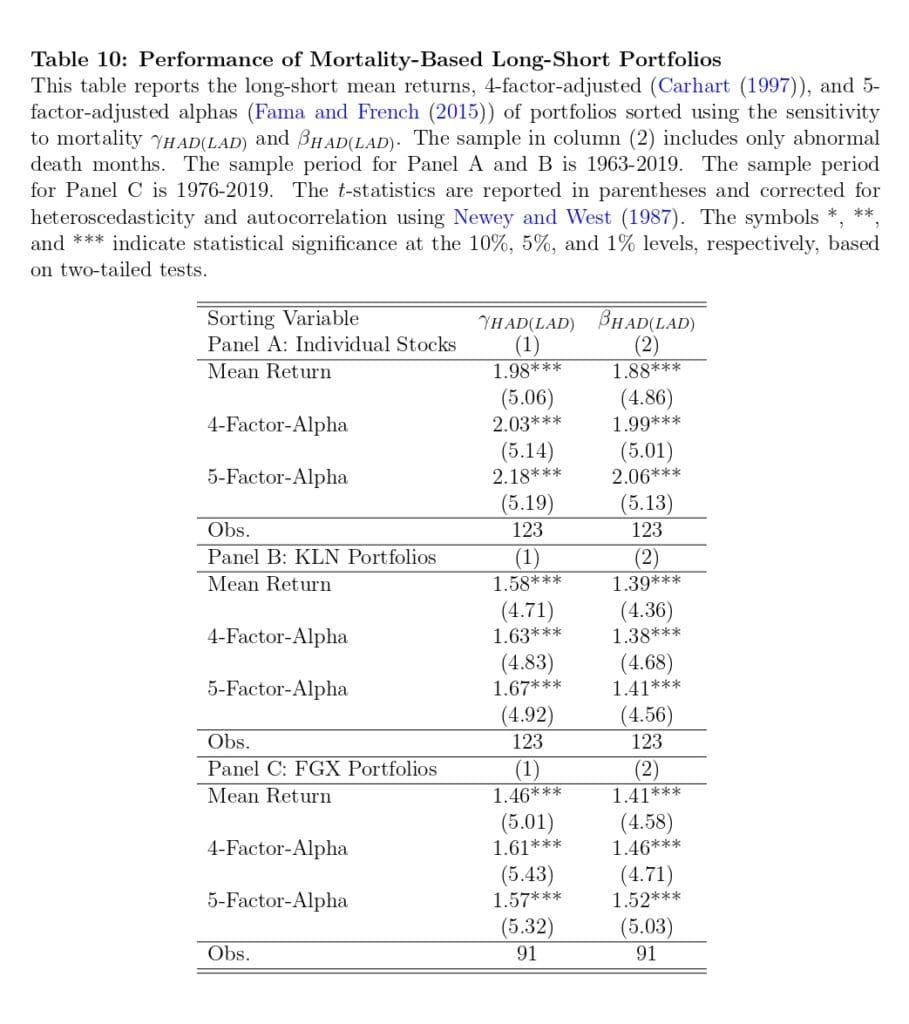

Finally, we construct a Long−Short portfolio strategy that exploits the abnormal mortality effect in stock returns. We first measure individual stocks’ historical return sensitivities to mortality based on the their previous returns during HAD and LAD months. Specifically, we estimate monthly regressions where we explain a stock’s return over the risk-free rate with market beta and dummy variables for HAD and LAD months. The coefficients on the HAD and LAD indicators capture the stocks’ return sensitivity to mortality during HAD and LAD months, respectively.

During a HAD (LAD) month, we invest in a long portfolio consisting of stocks in the top decile of HAD (LAD) sensitivity coefficients and take a short position in a portfolio consisting of the bottom decile of stocks based on their HAD (LAD) sensitivity. Both portfolios are market value-weighted.

We test the performance of this strategy during HAD and LAD months, and we find that the Long−Short strategy has a monthly four-factor alpha of 2.03% for individual stocks and 1.4%-1.6% for the test portfolios. Monthly mortality is only known ex-post, so this strategy is not tradable without a mortality prediction model, but the results provide evidence of a relation between mortality and individual stock returns. The alphas are comparable to the estimates in Hirshleifer et al. (2020).

Variation in the monthly mortality rate can affect mutual fund net inflows because the elderly who pass away typically withdraw money from mutual funds regularly and do not accumulate additional savings from labor income. All else equal, a reduction in outflows related to increased mortality will cause fund net inflows to be more positive.

Variation in the number of deaths can also impact mutual fund flows through a secondary channel related to the investment behavior of people connected to the deceased. In many situations, transactions related to inherited retirement savings can push the inheritors into a higher tax bracket, even though the inheritance of funds in itself is not a taxable event. The beneficiaries will have additional income if they decide to cash out some or all of the inherited funds during the year of death. If the deceased person is over 70 and the year-of-death RMD was not already fully taken by the account owner, the IRS requires that the remainder must be taken by the beneficiary before the end of the year. This will result in additional taxable income even without any voluntary liquidations.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend