Analysts recommendations are quite puzzling topic among both practitioners and academics as well. The most important question related to the analysts is straightforward: what is the value of their recommendations? The research paper of Azvedo and Müller (2020) brings light on this topic, but also explores the relation of analysts recommendations and market anomalies. In line with other literature, it seems that the recommendations are significantly more valuable in international markets compared to the US market. While the prediction ability of analysts is not present in the US market, less developed markets and markets with higher limits-to-arbitrage are connected with valuable recommendations. Secondly, using around 200 cross-sectional anomalies, authors show that analysts are more lined up with anomaly-based composite mispricing measures in international markets. Therefore, there is not a bias from analysts to recommend overvalued stocks in global markets compared to the well-developed US market. We highlight several results and tables, but the paper is full of impressive results, ideas and tables. Therefore, we invite you to read this blog post as well as the source research paper.

Authors: Vitor Azevedo and Sebastian Müller

Title: Analyst recommendations and anomalies across the globe

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3705141

Abstract:

We reexamine the value of analyst recommendations using a dataset of 45 countries, 3.8 million firm-month observations, and more than 200 return anomalies from 1994 to 2019. We find that analyst recommendations lead to highly significant (insignificant) abnormal returns in international markets (in the U.S.). In contrast to recent U.S.-based evidence, analysts do not seem to contribute to mispricing in international markets, as they tend to give more favorable recommendations to (anomaly-ranked) underpriced stocks, and inconsistencies between recommendations and composite anomaly ranks lead to lower, not higher, abnormal returns. Recommendations are more valuable in less developed and in less individualistic markets and during low sentiment periods. Our results support limits-to-arbitrage and behavioral explanations of global stock market inefficiencies.

As always, the results can be presented through interesting charts and tables:

Notable quotations from the academic research paper:

“In this paper, we reexamine the value of analyst recommendations and their relation to anomalies for a global stock data set consisting of 45 countries, 3.8 million firm-month observations, and more than 200 return anomaly variables from 1994 to 2019. For the U.S. stock market, we successfully replicate the main findings in earlier research: First, analyst recommendations do not predict future returns, and, second, analysts favor stocks that are overvalued according to composite mispricing scores. We also confirm the finding of Guo et al. (2020) that “inconsistent” recommendation/anomaly strategies are often more profitable than consistent ones.

Outside the U.S. stock market, analysts make profitable stock recommendations. A recommendations-based long-short strategy generates a value-weighted (equally-weighted) raw return of 0.48% (0.58%) per month with a t-statistic of 5.05 (8.51) in worldwide stock markets excluding the U.S. In contrast, the same strategy for U.S. stocks yields economically negligible and statistically insignificant valueweighted (equally-weighted) raw returns of 0.08% (-0.02%) per month.

Using the Watanabe et al. (2013) indicators for financial market development and the cultural dimensions of Hofstede (2001), we identify the underlying drivers of cross-country differences in the value of the analyst recommendations. Specifically, their recommendations are more valuable in countries with less developed financial markets, including markets with shortselling restrictions, and in less individualistic countries.

Our second main insight is that outside the U.S. market, we find no evidence that analyst recommendations contribute to stock mispricing. In international markets, analyst recommendations are not negatively but positively related to composite (anomaly-based) mispricing scores. For the U.S. market, stocks in the lowest composite mispricing quintile (i.e., those considered the most overvalued) have an average consensus buy recommendation, which is statistically significant above the consensus recommendation of stocks in the highest (i.e., most undervalued) quintile. For the standard (enlarged) CMS, the difference is -0.17 (-0.22). In contrast, for international markets, stocks in quintile 5 have an average consensus recommendation, which is slightly above that of stocks in quintile 1. Specifically, the difference amounts to 0.06 (0.08) for the standard (enlarged) CMS. These findings do not suggest that analysts provide more favorable recommendations for overvalued international stocks.

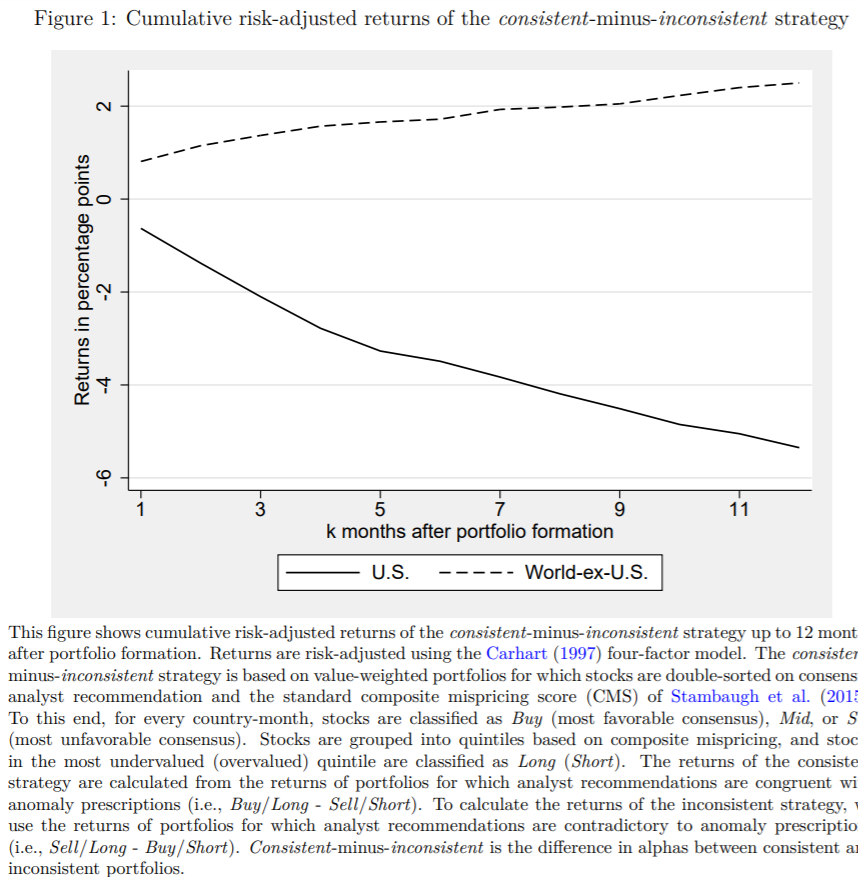

We find that consistent strategies, which are long in stocks with the highest consensus recommendation and highest mispricing score and short in stocks with the lowest consensus recommendation and lowest mispricing score, perform substantially better than inconsistent strategies in international markets. The double sort results demonstrate that the value of analyst recommendations in international markets is not subsumed by the composite mispricing score. They also suggest that analysts’ recommendations, viewed from a global perspective, may not be a source of market friction, which deters investors from efficiently correcting mispricing.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend