Carry Trade Across Fixed and Floating Currency Regimes

A new financial research paper related to:

Authors: Accominotti, Cen, Chambers, Marsh

Title: Currency Regimes and the Carry Trade

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3077029

Abstract:

Carry trade returns vary across fixed and floating currency regimes. Over the last century, outsized carry returns occur exclusively in the floating regime, being zero in the fixed regime. The absence of skewness in floating carry returns rules out a skewness-based explanation for this result. Fixed-to-floating regime shifts deliver negative return shocks to the floating carry strategy, even when controlling for volatility risk. This result explains average excess returns to the floating and therefore the unconditional carry trades over the long-run. We rationalize these findings with a model allowing risk compensation in currency markets to depend on regime.

Notable quotations from the academic research paper:

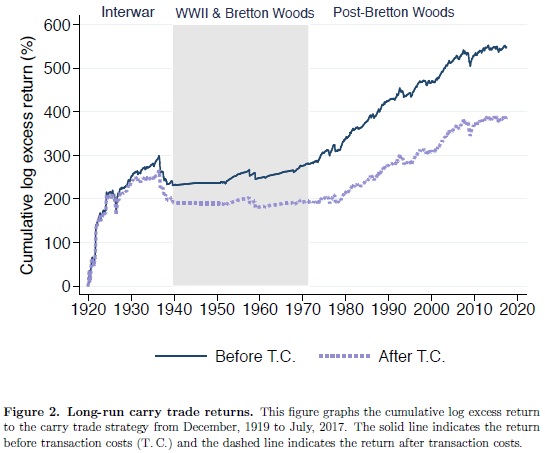

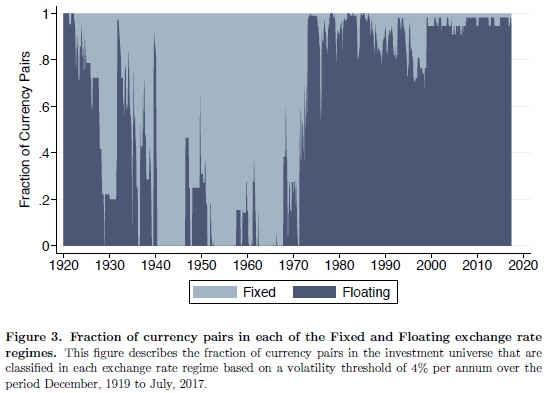

"Our empirical analysis exploits a new database of daily bid and offered exchange rates in spot and forward markets spanning the interval 1919-present. The year 1919 marks the dawn of modern currency trading with the emergence of a continuously traded forward market in London. Consistent with the post-Bretton Woods evidence, we find that the carry trade earns significant average returns over the whole sample period. Our estimated Sharpe ratio of between 0.5 and 0.6 is still substantial and only slightly lower than the 0.7 to 0.8 for the post-Bretton Woods sample. This finding of outsized carry returns across the whole period is robust to differing portfolio weights and to the inclusion of transaction costs. We further exploit our data to examine the dependence of carry trade returns on currency regimes by conditioning the return to the carry trade on the exchange rate regime of each currency pair at the beginning of each period.1 We classify any currency pair into a floating (fixed) regime based on whether its exchange rate volatility is above (below) a certain threshold.

Our first finding is that carry trade returns vary with exchange rate regimes. Average excess returns of the unconditional carry trade are entirely driven by returns to the carry strategy conditioned on the sample of currency pairs in the floating exchange rate regime. We term this strategy the floating carry trade. In comparison, the carry strategy conditioned on the sample of currency pairs in the fixed exchange rate regime (the fixed carry trade) generates zero returns on average. Moreover, the exchange rate of a floating currency pair tends to move according to a random walk without drift as the average spot return is close to zero and statistically insignificant. In contrast, the exchange rate of a fixed currency pair tends to move as predicted by the uncovered interest parity (UIP). Although the carry component of fixed carry trade returns is substantial at 2-3%, these gains are exactly offset by losses from spot rate depreciation when fixed exchange rate regimes collapse.

There are three other results related to our main finding regarding the regime-dependence of carry returns.

First, we find that the skewness of returns to the floating and fixed carry trade strategies in our long sample differ from the consensus view regarding skewness in the literature. In the post-Bretton Woods period, outsized carry returns display negative skewness and we confirm this result in our own sample. However, when we examine skewness of floating and fixed carry returns separately in our long sample, only the unprofitable fixed carry trade displays negative return skewness due to losses arising from the collapse of currency pegs. In contrast, the return skewness of the profitable floating carry trade is not significantly different from zero.

Second, we further explore the indirect relationship between floating carry returns and the fixed regime. We find that the more that either currency in a floating pair is in a pegged relationship with other currencies, the worse is the performance of the floating carry trade strategy.

Last, we ascertain that the variation of carry trade returns is not only related to the time-series but also the cross-section of exchange rate regimes across currency pairs.

Our second main finding is that the collapse of currency pegs has spill-over effects on floating currency pairs, thereby causing significant losses to carry traders. The January 2015 abandonment by the Swiss National Bank of its cap on the value of the franc against the euro is an example of such a collapse. The breakdown of this particular fixed exchange rate coincides with poor carry trade returns when investment currencies such as the Australian and New Zealand dollars depreciate against the pound sterling, while funding currencies such as the Japanese yen and Swiss franc appreciate. Our regression analysis verifies that this example is representative of the relationship between fixed-to-floating regime changes and negative returns to the floating carry trade.

"

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend