Fake Trading on Crypto Exchanges

At Quantpedia, we acknowledge that cryptocurrencies offer numerous trading opportunities and include them in the Screener. Yet, each participant should be cautious. Cryptocurrencies are not black or white; they have their pros but also cons. Perhaps now, with all the positive sentiment around cryptos, it is the right time to advert also the cons. It is not that long time ago when we published a blog about the Bitcoin´s price manipulation, where the anecdotal evidence was supported by the Benford´s law which is related to the distribution of leading digits.

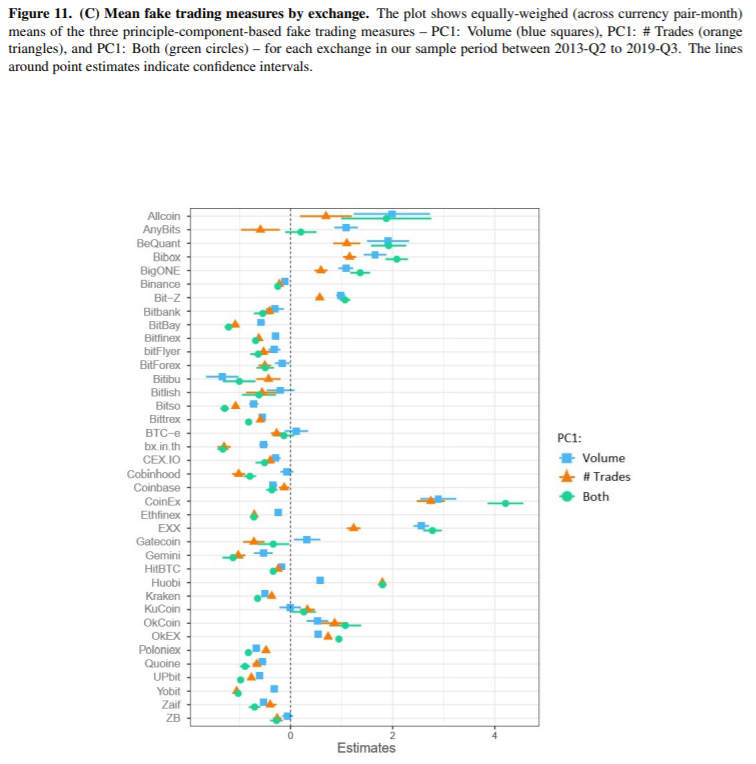

The novel research of Amiram et al. (2020) expands the previous work about the manipulation of the BTC. The authors include a tremendous amount of currencies, study various exchanges, and most importantly, they use more methods to examine the manipulations. To be more precise, the authors utilize the Benford´s law, deviations from the log-normal distribution and the novel machine-learning algorithm E-Divisive with medians that identifies structural breaks in time series. Moreover, they aggregate the measures by computing their principal components. While the results are as always best shown by the included figures, there are numerous practical suggestions. The fake trading benefits exchanges in the short term; however, it is harmful in the long term. Lastly, exchanges with the highest popularity, some regulations and the oldest ones tend to have the lowest fake trading levels.

Authors: Dan Amiram, Evgeny Lyandres and Daniel Rabetti

Title: Competition and Product Quality: Fake Trading on Crypto Exchanges

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3745617

Abstract:

We empirically examine the effects of competition among cryptographic exchanges on their trading volume inflation (fake trading) and its impact on exchanges’ operating performance. We develop statistical measures to detect fake trading, which we validate in several ways and use in analyzing determinants and consequences of volume inflation. Various competition measures increase fake trading at both the exchange and exchange-currency pair levels. Exchanges that inflate trading volume succeed in misleading investors in the short run but are punished in the long run, consistent with the tradeoff between current increases in rents and future losses due to damaged reputation.

As always the results are best presented through figures:

Notable quotations from the academic research paper:

“In this paper, we examine empirically the relation between competition and firms’ choices of their products’ quality, as well as implications of these choices for firms’ future performance. We focus on an industry that, as we argue, is well suited to an examination of this relation – cryptographic exchanges (exchanges where most of the Bitcoin and cryptocurrency trading takes place).

Crypto exchange industry is especially suitable for an examination of determinants and consequences of product quality choices in a competitive setting for a number of reasons. First, trading volume on exchanges is positively related to anticipated product quality, as trading volume is generally perceived to be associated with market depth. Exchanges have access to an easily implementable technology for misleading consumers regarding the quality of their product: artificial inflation of trading volume by means of fake (wash) trading (e.g., Cumming et al. (2011)).

The reason trading volume is an important signal to market participants of an exchange’s quality is that most aggregator websites, such as www.CoinMarketCap.com, explicitly rank exchanges on trading volume. In the absence of credible signals of exchanges’ quality, it is plausible that many investors rely on these rankings in their choice of trading venue.

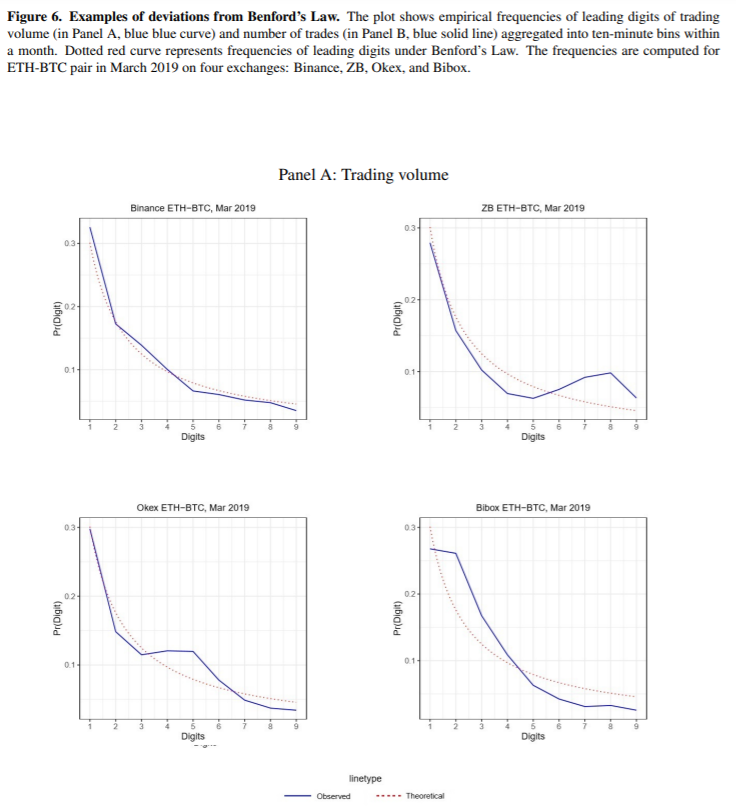

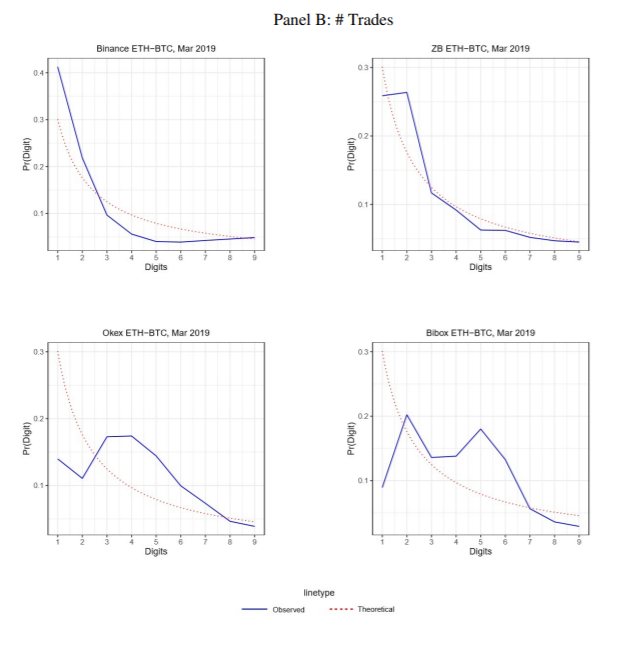

As fake trading is unobservable and not directly detectable without addresses of accounts (crypto wallets) that performed the trade, we proceed to develop statistical measures of fake trading at the exchange currency pair-month level. We estimate all the measures discussed below using both the trading volume and the number of trades series. Our first measure, also used in and Aloosh and Li (2020) and Cong et al. (2020), is the deviation of the frequencies of first digits of either the trading volume or the number of

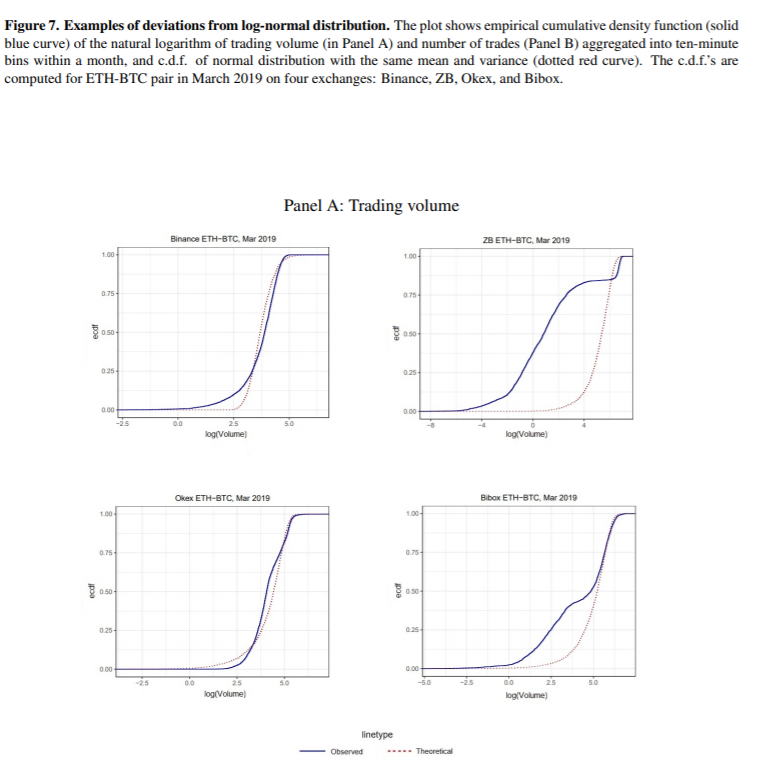

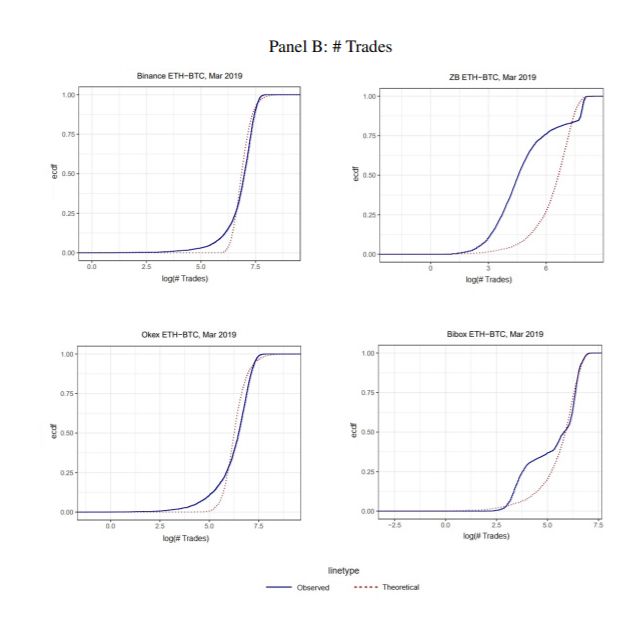

trades within short time intervals from Benford’s Law (Benford (1938)). This law describes expected frequencies of first digit equaling one through nine for naturally observed series that are not constrained to a certain range. Larger departures from Benford’s Law may indicate higher likelihood of data manipulation. Aloosh and Li (2020), who, along with Gandal et al. (2018), provide direct evidence of wash trading by using an internal book of individual trader level records from Mt.Gox exchange, show that Benford’s Law is useful in detecting fake trading. The other two measures of fake trading are novel to the literature. Our second measure is based on the deviation of the distribution of trading volume/number of trades within short intervals from log-normal distribution that tends to characterize typical trading volume series not subject to manipulation (e.g., Richardson et al. (1986) and Ajinkya and Jain (1989)). Our third measure is based on a machine-learning non-parametric algorithm called EDM (E-Divisive with medians), which identifies structural breaks in data series (e.g., James and Matteson (2015) and James et al. (2016)). The larger the number of identified structural breaks in the trading volume or the number of trades series, the higher the chance of manipulation of the data e.g., by means of trading volume inflation. This measure, while well known on the computer science literature, is new not only to the crypto exchanges literature but to finance literature in general to the best of our knowledge. Since the measures discussed above aim to identify particular deviations from normal trading patterns and none of them is likely to be capable of identifying the majority of such deviations, we aggregate these measures by computing their principal components.

We show that our estimates of fake trading tend to be the lowest for exchanges with the highest web popularity, the oldest exchanges, and the minority of exchanges that are regulated to some degree (and it’s important to find regulated exchanges when you want to employ the best way to buy crypto in Australia, the US, the EU, or any other developed market). On the contrary, exchanges with reported cases of manipulation tend to have some of the highest fake trading measures. Second, we find that fake trading measures are higher for exchanges with relatively low levels of self-imposed regulation and compliance, and those with relative low levels of transparency. Third, we estimate other, more intuitive measures of fake trading, which are based on contemporaneous correlations between either the number of trades or trading volume in a given currency pair on a given exchange with the same variable aggregated for that currency pair on all exchanges, with the idea that fake trading, which is unlikely correlated across exchanges, depresses these correlations. We find that our statistical measures of fake trading are significantly associated with alternative, more intuitive, correlation-based measures.

Our analysis of the effectiveness of fake trading, i.e. its ability to generate short-term rents, shows that exchanges are generally successful in misleading consumers in the short run. Fake trading raises future trading volume, exchange’s web popularity, and estimated trading commissions over one-to-three months horizons. However, the strategy of inflating trading volume has its long-term costs. The effects of fake trading on longer-run operating performance is negative: Both the web popularity and estimated trading commissions are significantly negatively related to fake trading over the twelve-month horizon.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend