How Global Neutral Rates Impact Currency Carry Strategies?

Market practitioners often rely on experience-based wisdom to navigate currency markets, and one such widely held belief is that low dispersion in global bond yields signals weak future returns for carry trades (and high dispersion implies high future carry returns). While this intuition makes sense—when yield differentials are compressed, the incentive to exploit them diminishes—a recent academic study provides a solid theoretical foundation for this idea. The research not only confirms this observation with rigorous empirical analysis but also explains the underlying financial mechanisms that drive the relationship. By quantifying the effect and presenting clear visualizations, the study transforms an intuitive market rule of thumb into a well-grounded principle backed by data.

The paper presented uses the relationship between currency risk premia and long-term trends in fixed income markets to estimate neutral rates. Specifically, the authors apply a bilateral bond market model across major G9 advanced economies and the United States, providing long-term estimates that account explicitly for the interconnectedness of key financial markets. The main findings are:

- Impact of Neutral Rates on Currency Carry Trade Strategies:

The authors find that periods of lower average global neutral rates are associated with reduced returns from various carry trade strategies. Conversely, when long-term interest rates are higher and more divergent, carry trade strategies tend to generate significant returns. This highlights the critical role of long-term interest rate differentials in driving carry trade profitability. - Global Trends in Interest Rates:

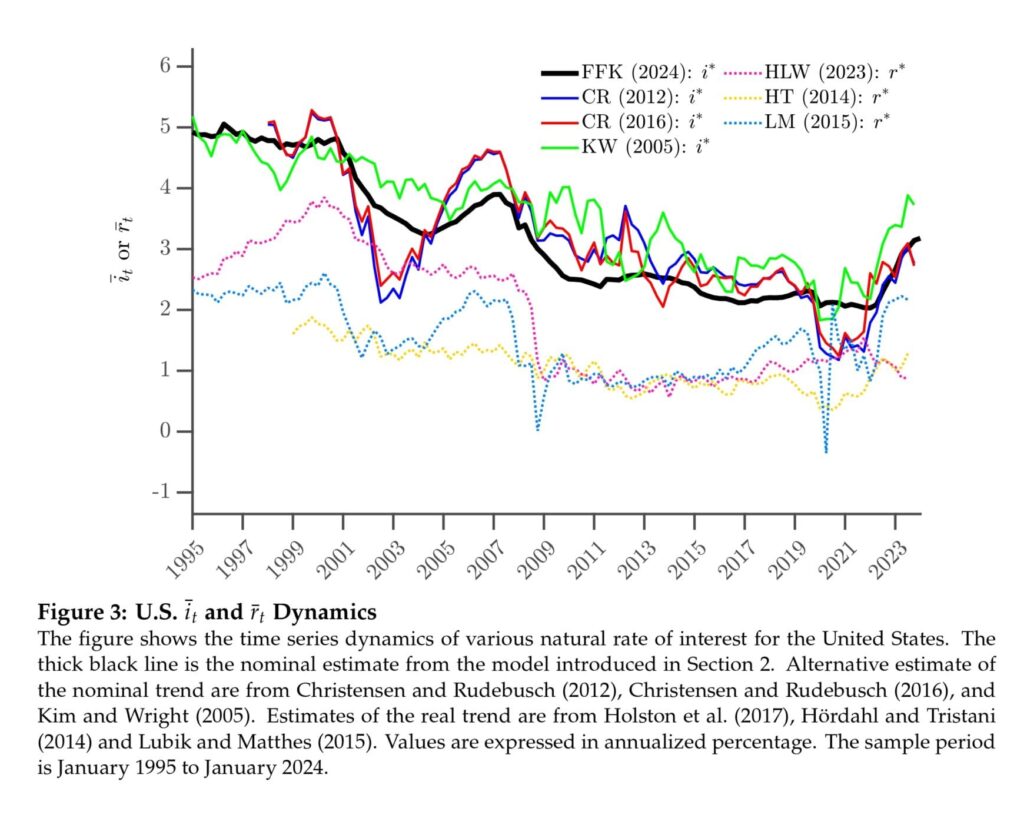

The authors document a secular decline in global neutral rates, which reversed with the onset of the recent hiking cycle in 2020. They observe strong co-movements in interest rates across foreign countries, with the U.S. neutral rate at the center of the G9 economies. The dispersion of interest rate trends across countries has gradually narrowed over time. - Interest Rate Trends and Bond Market Dynamics:

The study shows that accounting for interest rate trends across countries helps refine expected returns in dollars from holding foreign long-term bonds and from currency carry trades. The difference between interest rate trends matches the carry trade risk premia in long-term foreign bonds, providing predictive content for foreign bond returns in dollars that increases with the maturity of the bonds. - Role of Exchange Rate Dynamics:

The authors emphasize the importance of considering exchange rate dynamics when estimating neutral rates for small open economies. Traditional single-country models may lead to incomplete or inaccurate assessments of long-term neutral rates. The interconnectedness of currency dynamics plays a significant role in shaping neutral rate estimates, particularly for low-interest-rate countries.

Authors: Bruno Feunou, Jean-Sebastien Fontaine, and Ingomar Krohn

Title: Twin Stars: Neutral Rates and Currency Risk Premia

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5066288

Abstract:

Under no-arbitrage conditions, the currency risk premium connects the neutral interest rates of two countries. We implement this restriction in a two-country model of exchange rate and foreign bond markets, documenting novel empirical facts on global neutral rates and their role in currency markets: (i) global trends in interest rates exhibit strong co-movements across foreign countries, with the U.S. neutral rate in the center of the G9 economies; (ii) global neutral rates are characterized by a secular decline, which reverses with the onset of the recent hiking cycle in 2020; (iii) crosscountry global rate dispersion has gradually narrowed over time; (iv) periods of lower average global neutral rates are associated with reduced returns from various carry trade strategies; and (v) accounting for interest rate trends across countries helps to refine expected returns in dollars from holding foreign long-term bonds and from currency carry trades. Our findings provide strong evidence that global currency markets interweave foreign and domestic fixed-income markets, highlighting the strong link between these market segments.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“These results can be challenging to illustrate because the quantities involved are difficult to estimate. To further motivate our analysis, we consider a simple implication that does not rely on further identifying assumptions. We compare the sample means of the interest rate differentials relative to the U.S. with the sample means of excess returns from carry trading across all of the G9 currencies. We find that the average spreads closely line up with the average carry returns, and we find no statistical evidence against the null hypothesis.2 This unconditional finding is consistent with the results from Hassan and Mano (2018) and may help rationalizing why a static portfolio sorted on the initial level of interest produces most of the average returns from the carry strategy in the cross-section of currencies, while the dynamic portfolio that is rebalanced over time produces small average returns.

We estimate this two-country model separately for the G9 currencies. Compared to the U.S., the estimated trends are lower for Switzerland, Japan, and the Euro area, but higher for the New Zealand, Australia, Norway and Great Britain. The average difference relative to the U.S. lies between -1.5 to -1 percent for the low interest rate countries and ranges between 1 to 2 percent for the high-interest rate countries. These results align with the persistent interest rate differentials underlying carry strategies in foreign exchange markets.

Further, we build and expand on the results of Lustig, Stathopoulos, and Verdelhan (2019). Fixing the investment horizon, they show that the predictability of foreign bond returns in dollars declines with the maturity of the bonds and offset the currency risk premium at the longest maturity. Lustig et al. (2019) also translate this result into a important preference-free condition that no-arbitrage models must satisfy. We show that this condition implies that the two countries share the same interest rate trends. However, we build on their analysis and modify this condition for the case when two countries do not share the rate trends. In that case, the difference between the interest rate trends matches the carry trade risk premia in long-term foreign bonds. Consistent with this prediction, we find that the trend differences that we estimate exhibit predictive content for foreign bond returns in dollars that increases with the maturity of the bonds. This predictability is significantly larger relative to benchmark predictability using differences between short- term interest rates, or differences between the slopes of the yield curves. Therefore, accounting for the difference between trends in interest rates can help understand the properties of the carry trade risk premiums.

Figure 1 compares the sample average excess returns for each currency relative to the U.S. against the average interest rate differential for maturities of 3 months as well as 2, 5, and 10 years across Panels (a)-(d). The results show that average excess currency returns exhibit a wide dispersion across countries, as expected, ranging from 3.1 to -2.1 percent (annualized) for the Japanese yen and the New Zealand dollar, respectively. The average interest rate differentials exhibit a similar dispersion across countries for every bond maturities. For 3-month interest rates, the average differential range between -2.58 to 2.14 percent, respectively for the same two countries.6 We report the results in Figure 1.

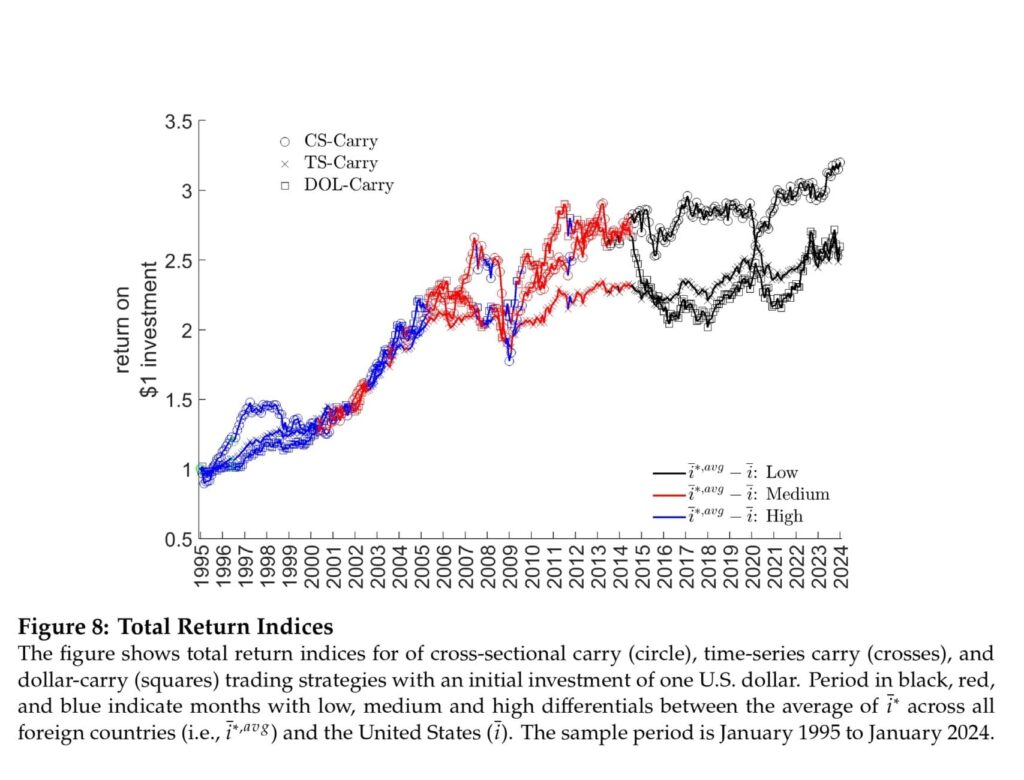

In Figure 8, we report the cumulative returns from each carry trading strategy separately, but in each case scaled with an initial $1 investment at the beginning of the sample period. We also highlight with different colors the periods when Δ𝑐 ¯𝑖𝑎𝑣 𝑔 𝑡 is either “low”, “medium” or “high”. A few key observations emerge. First, the three strategies exhibit a clear commonality, especially early in the sample. During this period, from 1995 to around the 2008 financial crisis, the strategies are visually nearly indistinguishable and earn a steep average returns. Figure 8 also shows that this period largely corresponds to the sub-sample when the cross-country average differential Δ𝑐 ¯𝑖𝑎𝑣 𝑔 𝑡 is high.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend