Hunt for Yield

Thanks to quantitative easing, we see record-low interest rates. While yields for short to intermediate maturities in the US are lower than the inflation but still positive, other developed markets such as Japan or European countries even have bond yields negative. Still, it does not implicate that investors have withdrawn from the fixed income markets. Both individual and institutional investors still participate in bond trading. However, the critical question is how these conditions influence the investors. Does their behavior change? Do they reach for yield and prefer riskier bonds in the search for (positive) real yields? In this blog post, we present three novel research papers that offer insights into this topic. The first examines the tendency of both retail and institutional investors to chase bond mutual funds with higher yields. The second research sheds more light on the behavior of institutional fund managers. If yields are falling, they transition into higher yields, higher duration and lower rating in the hunt for yield. Lastly, this post also offers insight into a similar situation in the past and presents an interesting piece of research that examines the reach for yield in the Netherlands during the 17th-18th century. It seems that there are several parallels with the present and reaching for yield is nothing new but rather something cyclical and repeating.

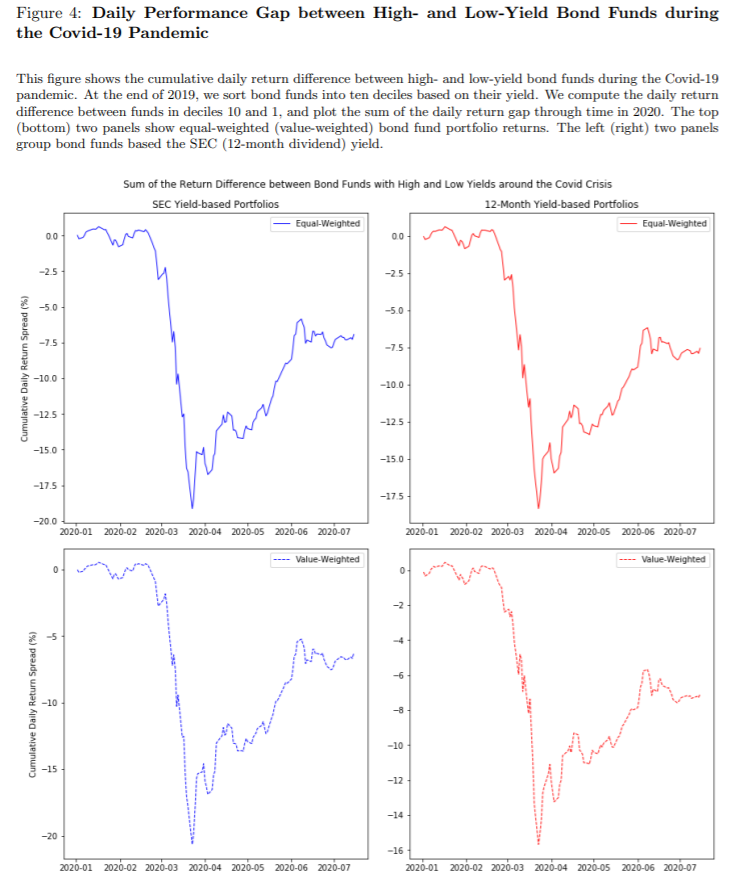

Several interesting facts are connected with bond mutual funds. There are set strict rules regarding computation and advertising of the bond yield for fixed-income oriented mutual funds. Therefore, the yield can be easily compared across various funds. The novel research of Jiang et al. (2021) investigates how investors (both individual and institutional) perceive this fund yield information. Authors use two different measures of fund yield: 30-day SEC yield and 12-month distribution yield. Both measures indicate the same result – investor tends to “hunt for yield” and chase mutual funds with higher yields. While both yields are related to fund inflows positively, it seems that the 30-day SEC yield impact is approximately three times larger. Additionally, we can dissect between individual and institutional investors. The SEC yield is attractive for both groups; however, higher distributions are mainly attractive for individual investors. Regarding the performance, funds with higher yields are connected with higher returns on average, but the difference in returns is frequently lower than half of the yield difference. Lastly, the paper also shows that higher yield funds are, as expected, riskier. Bearing higher interest and credit risk and great exposure to crises, the hunt for yield can be costly.

Authors: Hao Jiang, Lily Li and Lu Zheng

Title: Beware of Chasing Yield: Bond Fund Yield, Flows and Performance

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3804118

Abstract:

This paper studies the role of mutual fund yield in driving investor flows and performance of bond funds. Using two common measures, the SEC yield and 12-month distribution yield, we find strong evidence that investors tend to chase bond funds with higher yields, even after controlling for total fund returns and fund ratings. Although bond funds with higher yields achieve higher average total returns, the return spread is less than one half of the yield spread, and is attributable to higher fund risk. We also show that high yield bond funds suffer sharp losses during crisis periods, which trigger large outflows.

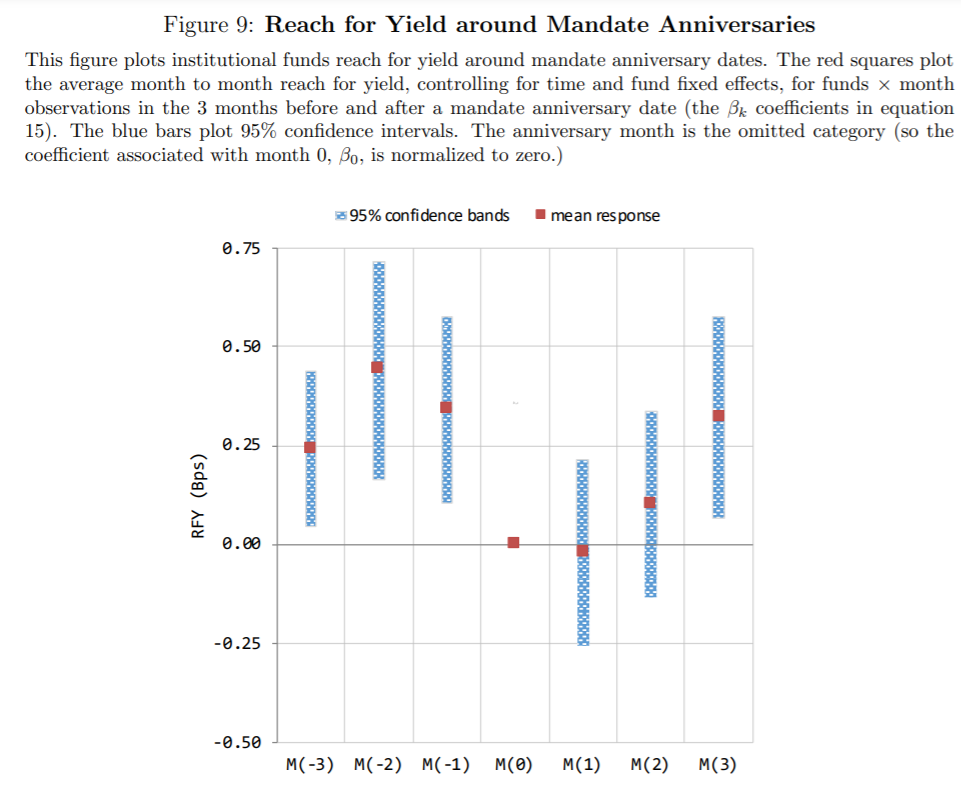

The novel research of Barbu et al. (2021) using a dataset from Germany examines the behavior of institutional funds. The results are particularly interesting since Germany is one of the largest asset management markets. Additionally, the bonds have a significant share in institutional funds since 77% of funds are allocated into bonds. As we have previously mentioned, the interest rate decline is even more profound in the European markets. How do the institutional investors react to these declining rates? The research shows that there is a reach for yield too. Investors opt for riskier bonds with a lower rating or higher duration and interest rate risk in the search for the yield. There is a strong procyclicality. Funds actively move into higher yields, longer durations and lower ratings as yields decline and spreads compress, and vice versa if rates are rising. Additionally, the hunt for yield is even stronger when the interest rate falls below zero. The risk-taking magnifies, particularly when clients have capital guarantees. The key question is why there is this behavior since the institutional funds are connected with small and infrequent outflows, and fund managers do not chase yields to attract inflows. The authors suggest that this effect is rather connected with career concerns. The probability of the fund´s termination by the asset management company is lower for funds that invested into bonds with higher yields in the recent past. Therefore, it seems that fund managers hunt for yield to prolong their mandates. However, there is a catch, higher-yielding bonds are riskier. The high yield truly is connected with lower termination rates during regular times, but this reverse during crises. In such situations, higher-yielding bonds have lower returns, and thus, the termination probability rises. To sum it up, the hunt for yield can backfire in stressful times.

Authors: Alexandru Barbu, Christoph Fricke and Emanuel Moench

Title: Procyclical Asset Management and Bond Risk Premia

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3804831

Abstract:

We use unique institutional securities holdings data to examine the trading behaviour of delegated institutional capital and its impact on bond risk premia. We show that institutional fund managers trade strongly procyclically: they actively move into higher yielding, longer duration and lower rated securities as yields fall and spreads compress, and vice versa. Funds more exposed to negative yields increase their risk-taking more strongly, and this effect is particularly pronounced for those offering explicit minimum return guarantees. Institutional funds’ investments have large and persistent price impact in both corporate and sovereign bond markets. We provide evidence that this procyclical behaviour is driven by career concerns among institutional fund managers.

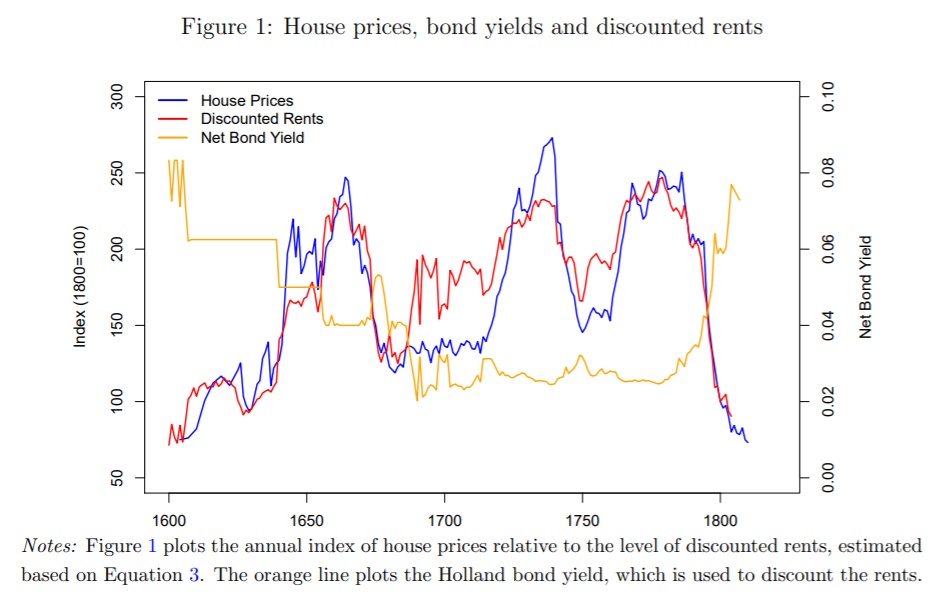

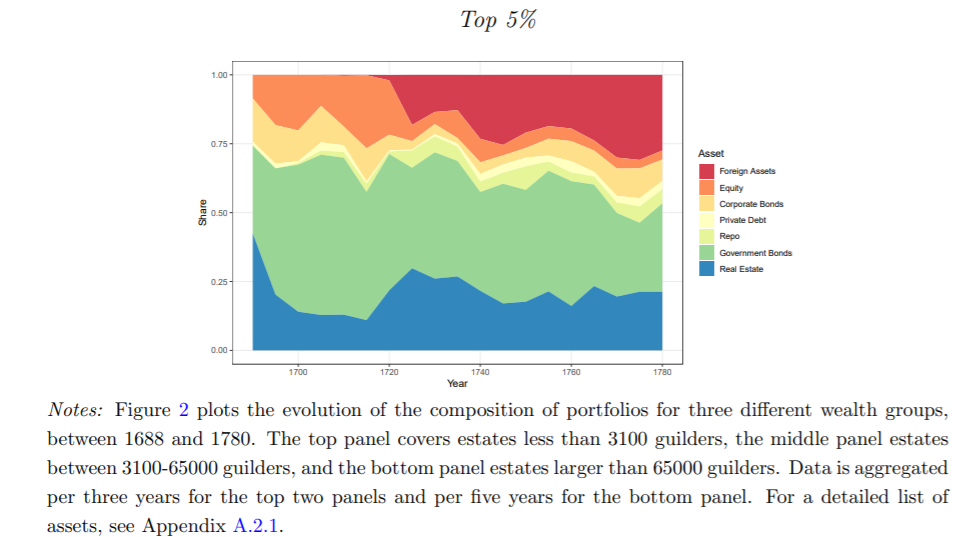

Many wealthy investors in historical Amsterdam relied on safe government bonds. Surely, we have to account for the availability of investments during the 17th and 18th century, but when yields fell, did investor reached for it? As novel research of Korevaar (2021) shows, using a unique dataset, these investors also sought “better” opportunities elsewhere. They could not opt for bonds with longer duration or lower rating, so they looked for the yield elsewhere. In the periods of falling interest rates, real estate was the place to be. Moreover, the author offers an explanation of why this reach for yield occurred. During wars, Holland was forced to issue large amounts of bonds, which rentiers were happy to buy for a safe income. On the other hand, during times of peace, the yields fell, and the opportunities had to be sought elsewhere. Low rates motivated wealthy investors to move into the real estate market since they relied on capital returns as their source of income. However, this is completely understandable since they only had two options: expense less or look for the yield. Lastly, also this hunt for yield had it is own negative effects. As the author shows, the reach for yield had several detrimental effects on the real estate market.

Authors: Matthijs Korevaar

Title: Reaching for Yield: How Investors Amplify Housing Booms and Busts

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3794782

Abstract:

Do investors reach for yield when interest rates are low, and how does this behavior influence house prices? This paper uses the unique setting of 17th-18th century Amsterdam to answer this question, using newly-collected archival data on investment portfolios and the universe of property transactions in this period. Exploiting exogenous shocks in the supply of safe government bonds, I show that wealthy investors shifted their wealth towards higher-yielding assets such as real estate when bond yields were decreasing. This behavior exacerbated booms and busts in house prices and resulted in a persistent increase in housing wealth inequality. Reach for yield behavior was not limited to real estate assets and contributed to the development of international financial markets.

As always we present several interesting figures:

Hao Jiang, Lily Li and Lu Zheng: Beware of Chasing Yield: Bond Fund Yield, Flows and Performance

Alexandru Barbu, Christoph Fricke and Emanuel Moench: Procyclical Asset Management and Bond Risk Premia

Matthijs Korevaar: Reaching for Yield: How Investors Amplify Housing Booms and Busts

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend