ESG Investing during Calm and Crisis Periods

Over the last decade, investing responsibly and deploying capital for “ethically” correct and sustainable growth has been quite a theme. We dedicated a few blogs to this theme and have a separate ESG category for trading strategies in our database. It is often easy to commit financial resources to noble ideas during liquidity abundance. However, how do these methodologies fare during crisis times, such as when the GFC (Global Financial Crisis) or COVID-19 hit? That’s the question that a new paper by Henk Berkman and Mihir Tirodkar tries to answer.

University of Auckland Business School academics examine two research questions:

- First, how does ESG investing affect expected returns in general?

- Second, how does ESG investing affect expected returns during crisis periods?

Option-implied expected returns (from derivatives) have to say something about it all. Novel and forward-looking measures of expected returns derived from contemporaneous stock option prices were used to answer both. The main finding is that stocks with higher ESG scores have lower expected returns. However, this is only observed during the Global Financial Crisis and the COVID-19 pandemic.

The ESG risk premium term structure positively relates to ESG scores during crises, indicating that investors expect a reversion to normality within a year. The results are robust to various specifications and controls.

This research contributes to the literature on ESG investing by challenging the popular opinion that portfolios with higher ESG scores have higher expected returns. Instead, the notion that the theoretical prediction that ESG investing lowers expected returns is partially supported. This prediction holds during the GFC and the COVID-19 pandemic, when trust in firms and markets has sharply declined, but not outside of crises.

Implications for investors, managers, and policymakers are further brought:

- The paper suggests that ESG investing may not be a source of systematically superior returns for investors but rather a way of expressing ethical preferences and temporarily reducing risk during unexpected crises.

- For managers, the study implies that improving ESG performance may not be a value-enhancing strategy but rather a value-preserving strategy during crises.

- For policymakers, it indicates that ESG investing, especially during ‘normal’ times, may be insufficient to address the world’s challenges through a cost-of-capital framework and that more direct interventions may be needed.

Authors: Henk Berkman and Mihir Tirodkar

Title: ESG Investing During Calm and Crisis: Implied Expected Returns

Link: ESG Investing During Calm and Crisis: Implied Expected Returns

Abstract:

We examine the impact of ESG performance on option-implied expected returns. For a sample of S&P500 constituents over January 2007 to December 2021, we find that stocks with higher ESG scores have lower expected returns, but only during the Global Financial Crisis and the COVID-19 pandemic. We also find evidence of a positive, steeper ESG risk premium term structure during these crises, suggesting that investors expect a reversion to normal times within a year. Our results support the view that ESG investing reduces downside risk during crises, but contrast with the popular opinion that ESG investing increases expected stock returns over long periods.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“Figure 1 plots the ESG risk premium time series and provides an initial glimpse at the answers to our research questions. The plotted ESG coefficients give the difference in annualized 30-day expected returns for stocks in ESG decile 1 relative to stocks in ESG decile 10, on a monthly basis.5

Figure 1 shows that the annualized ESG premium is close to zero in normal periods and drops sharply during the GFC and COVID-19 crises, reaching a minimum of -12% in March 2020. Hence, investors only require lower returns for firms with relatively high ESG scores during crisis periods.

In summary, we find a negative cross-sectional relation between required returns and ESG scores which is only statistically significant during crisis periods. We also find that crisis periods are characterized by an upward sloping ESG risk premium term structure, reflecting an expectation of a reversion to normality within a year. Our contribution to the literature is threefold. First, we add to the debate on the impact of ESG investing on financial performance. In contrast to popular opinion (see footnote 1), we find no evidence that stocks with higher ESG scores have higher expected returns. On the contrary, our findings support the theoretical model of Pastor et al. (2021), which shows that in equilibrium stocks with higher ESG scores should have lower expected returns. However, we find that support for this prediction is restricted to crisis periods.

We run [TS on MSCI ESG decile ranks from 0 to 1, along with the Fama-French 5-factor betas and a set of firm characteristic] regression every month and plot the monthly timeseries of coefficients on the ESG score in Figure 3.

Figure 3 shows that the ESG premium term structure is typically flat but becomes much steeper during both the GFC and the COVID-19 crises. In times of turmoil, investors increase their short term required risk premium for low ESG stocks relative to high ESG stocks more than they do for their long term required ESG risk premiums. This result suggests that during both crises investors expect a reversion to normality relatively soon.

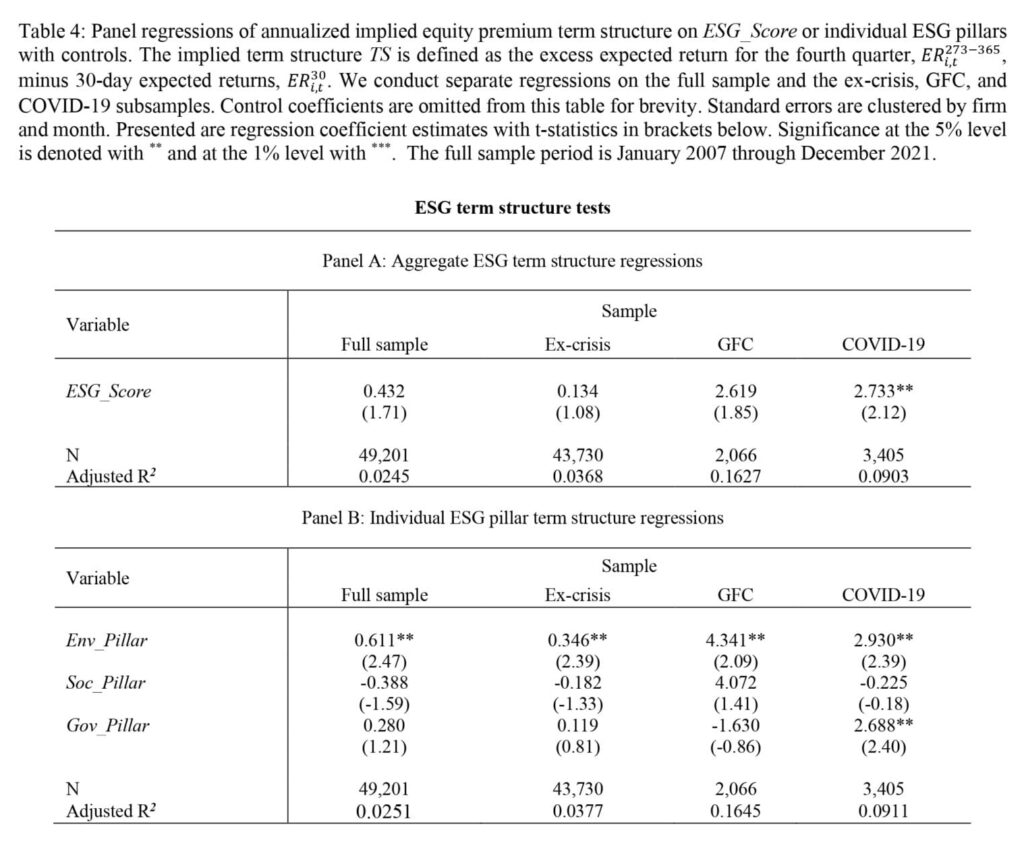

We present results from regression (3) in Table 4, which shows that during stable periods, all three individual ESG pillars generate insignificant risk premia. During the GFC, the only statistically significant premium is that of the environmental pillar, equalling 5.7% annualized. During the COVID-19 crisis, both the environmental and governance premia equal about 3.8% annualized, with significance at the 1% level.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend