Impact of US Inflation on Global Asset Returns

Frequently, inflation or the decline of purchasing power is one of the main reasons to invest – nobody likes lower purchasing power. Moreover, inflation is one of the crucial macroeconomic drivers of a variety of asset returns. Therefore, a lot of attention is centred around inflation in the academic literature.

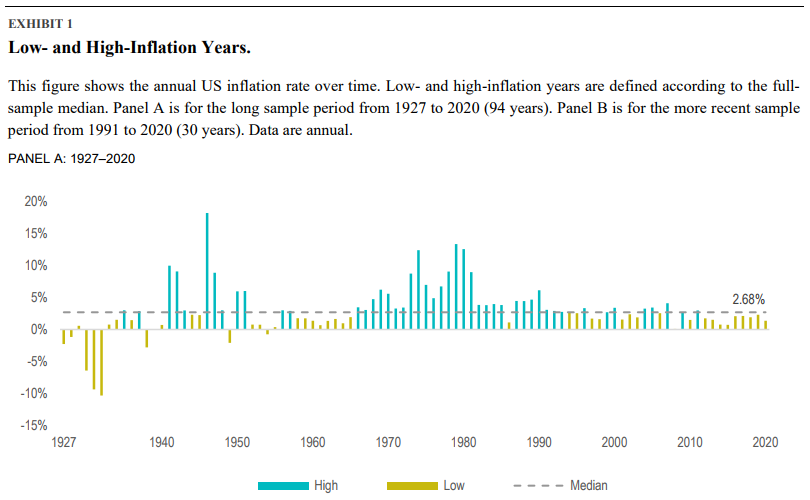

If the inflation is low and oscillates around central banks’ targets, there is not a big fuss around it. However, when inflation gets high, it becomes a hot topic among investors. Although the coronavirus crisis has not passed away yet, at least from the epidemiological point of view, financial markets recovered pretty well and sharply.

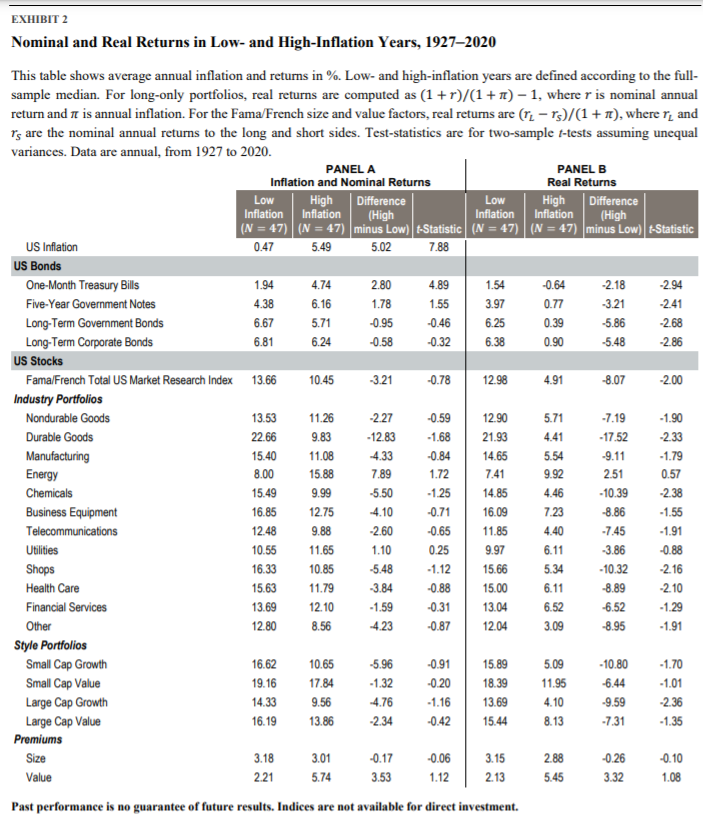

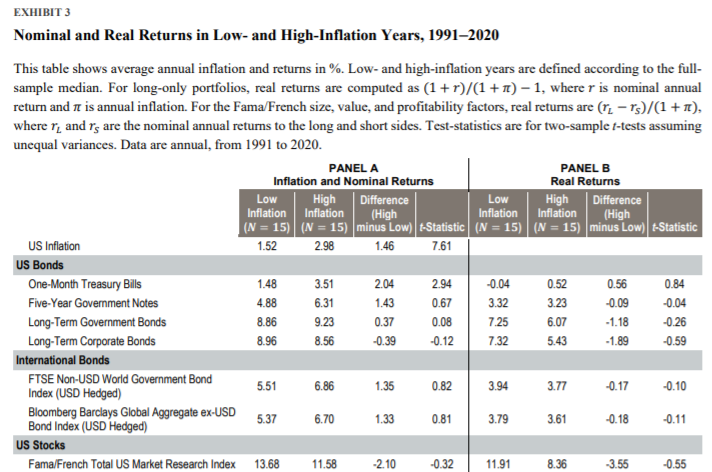

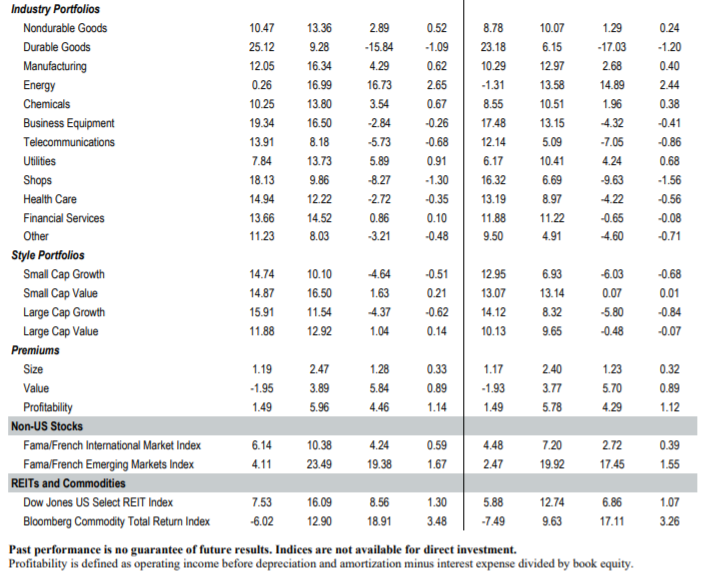

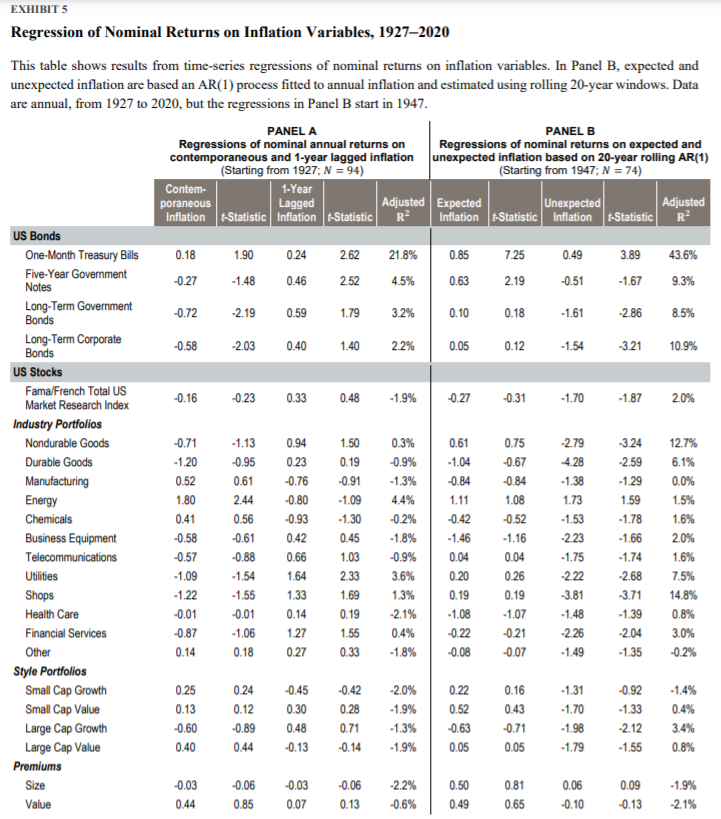

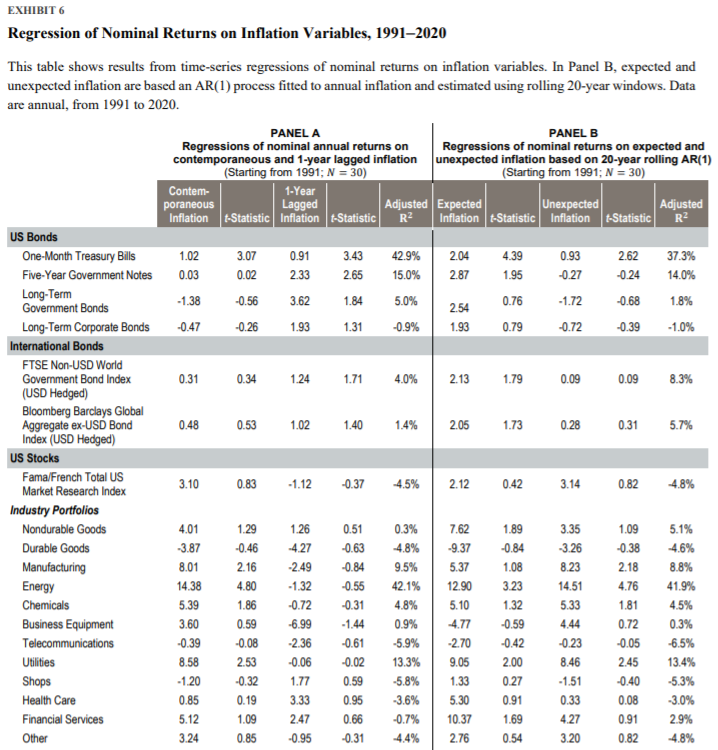

The sharp recovery is also accompanied by high inflation, and as we have previously mentioned, it has become a hot topic among practitioners. But is it truly that bad? Dai and Medhat (2021) show that inflation is not as big a problem as it may seem in the long term. The authors have examined the relationship between US inflation and the performance of global assets such as stocks, bonds, commodities, REITs, factors or industry portfolios. Based on an analysis of both long-term and the most recent sample periods, the results suggest that most assets had positive real returns during high-inflation periods (and low-inflation as well). The real returns tend to be lower during high-inflation times, but the differences between high and low periods are frequently statistically insignificant. Additionally, the authors also show a positive correlation between inflation and commodities or energy stocks, but both tend to be highly volatile. As a result, hedging high inflation might not be easy; for example, energy stocks or commodities are volatile, and TIPS do not offer high returns compared to equities. However, the paper suggests that inflation might not be that problematic in the long run and that a long investment horizon is sufficient to hedge inflation.

Authors: Wei Dai and Mamdouh Medhat

Title: US Inflation and Global Asset Returns

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3882899

Abstract:

We study the relation between US inflation and the performance of global asset classes (including bonds, stocks, industry portfolios, factor premiums, commodities, and REITs), both over a long sample period (1927–2020) and over the most recent 30 years (1991–2020). We find that most assets had positive average real returns in both low- and high-inflation years. While average real returns were lower in years with higher inflation for most assets, many of the differences are not statistically reliable, especially among non-bond assets and in more recent times. We also find mostly weak correlations over time between nominal returns and inflation, including contemporaneous, lagged, expected, and unexpected inflation. The notable exceptions are energy stocks and commodities, where there are reliably positive correlations with both expected and unexpected inflation, but our results also suggest both assets are too volatile to be an effective inflation hedge. Our results confirm the potential of most asset classes to outpace inflation over the long term and suggest that, for investors prioritizing the preservation of purchasing power, inflation-indexed securities may be a more appropriate inflation hedge than commonly suggested alternatives.

As always we present several interesting figures:

Notable quotations from the academic research paper:

“To outpace inflation over the long term, one can build an asset allocation that emphasizes assets with high expected real returns (i.e., net of inflation), such as equities. This may not be appropriate for all investors, however, if outpacing inflation means taking on more market risk than an investor is

comfortable with. For investors with greater sensitivity to inflation and lower risk tolerance, it might make sense to hedge against inflation by investing in assets that move closely with it. Inflationindexed securities—such as Treasury Inflation-Protected Securities (TIPS) and inflation swaps— are natural candidates, but some have argued that commodities, real estate investment trusts (REITs), stocks in “inflation-sensitive” industries, and value stocks may also be a good hedge against inflation.

We study the empirical relation between inflation and the performance of different asset classes. We take the viewpoint of a US investor with a global investment-opportunity set and analyze how the returns to government securities, corporate bonds, stocks, industry portfolios, size/value/profitability factors, REITs, and commodities have varied with inflation, including expected and unexpected inflation.

Our results are reassuring with regard to which assets have been able to outpace inflation over the long term. We find that most assets we study had positive average real returns in both low- and highinflation years. This is true over the longest sample period we consider, from 1927 to 2020, as well as the most recent 30-year period (1991–2020), where US inflation has been relatively benign and stable.

With regard to which assets have been an effective hedge against inflation, our results suggest that investors considering alternatives to inflation-indexed securities should do so while exercising caution. We find mostly weak correlations over time between nominal returns and inflation, including contemporaneous, lagged, expected, and unexpected inflation. In the few cases where the correlations were reliably positive, such as for energy stocks and commodities over 1991–2020, the assets’ returns were around 20 times as volatile as inflation and more than half of their nominal return variance was unexplained by inflation. Hence, if an investor is seeking inflation protection to reduce the uncertainty around the real value of future wealth, these assets may not accomplish this objective, because their relatively high volatility can lead to large dispersion in future consumption outcomes.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend