An Index of Commodity Futures Returns Since 1871

Authors: Rajkumar Janardanan, Xiao Qiao, and K. Geert Rouwenhorst

Title: An Index of Commodity Futures Returns Since 1871

Link: https://ssrn.com/abstract=6276738

Abstract:

This paper documents the returns to a broadly diversified index of commodity futures over more than 150 years of U.S. market history, that accounts for survivorship bias. We find that commodity futures have earned an average annual risk premium of 5.4% over the risk-free rate and a premium over US inflation of more than 6% per annum. Commodity futures have outperformed equities in roughly 43% of years and in two out of every five decades, suggesting distinct return drivers and meaningful diversification benefits. Futures returns have exceeded spot price returns on an interest-adjusted basis, consistent with the presence of a risk premium beyond spot price appreciation.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“[…] documents the returns to a broadly diversified index of commodity futures, covering

more than 150 years of economic, financial, and institutional development. The analysis is based

on a uniquely constructed dataset that draws from exchange yearbooks when available and relies

extensively on newspaper archives to fill gaps in coverage. By including both active and obsolete

contracts, the resulting index reflects the evolving structure of futures markets and captures the

performance of a broad array of commodities, many of which are no longer traded today.2

The main findings are that over the past 155 years:

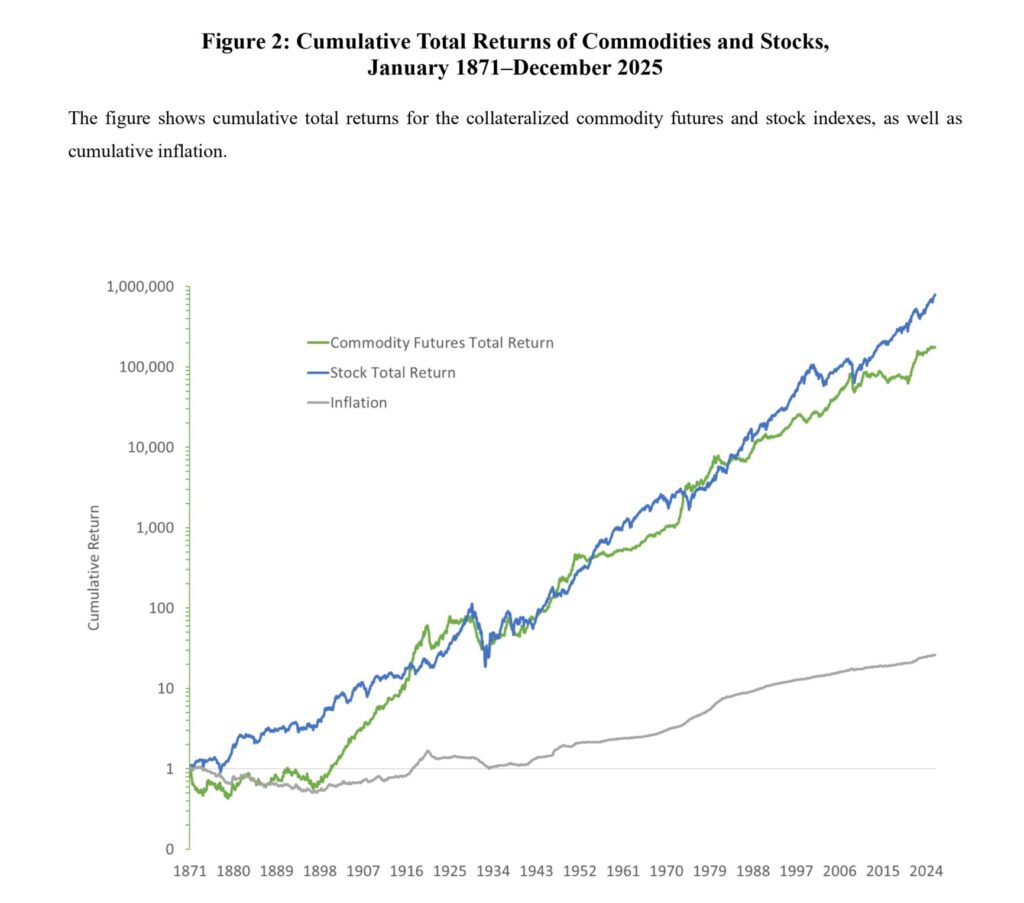

- Commodity futures have earned a risk premium over the risk-free rate of 5.5%.

- Commodity futures have outperformed U.S. stocks in two out of every five years.

- The return to commodity futures has exceeded an index of U.S. inflation by more than

6% per annum.

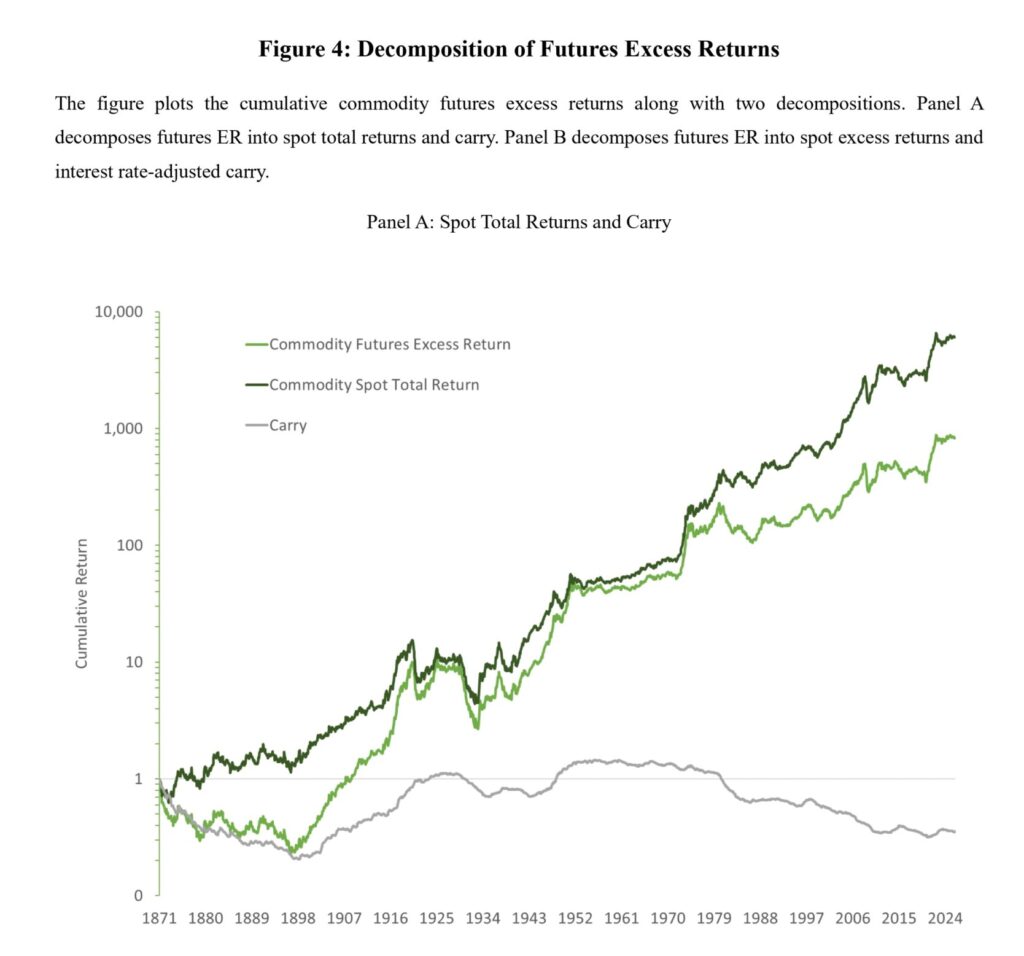

Finally, we highlight the distinction between futures and spot returns through a decomposition of futures excess returns into spot returns and the roll yield.

We quantitatively summarize our results in Table 1, which provides average returns, volatility, and Sharpe ratios of collateralized commodity futures, stocks, Treasury bills, and inflation over the 1871-2025 period. The top panel shows that the equally-weighted commodity futures index has earned a risk premium of 5.5%, with annualized volatility of 14.3%, and a Sharpe ratio of 0.38. For comparison, the stock index has a risk premium of 6.6% and a volatility of 16.2%, which results in a Sharpe ratio of 0.41. The commodity spot index has the same volatility as the commodity futures index, but a markedly lower Sharpe ratio (0.22). The risk-adjusted returns are similar for commodity futures and stocks, and exceed the risk-adjusted performance of the commodity spot index.

Long-term returns provide critical input to inform investors about the properties of an asset class, especially when the underlying asset class constituents are volatile. This chapter presents a 155- year history of commodity futures markets. Leveraging a unique hand-collected dataset, we present annual returns and cumulative returns to an index of commodity futures, and compare its performance to the aggregate stock market, inflation, and spot returns. Like stocks, commodity futures have a positive risk premium. Returns to commodity futures deviate from stocks in ways that provide periodic outperformance, likely due to different fundamental drivers of returns. While volatile over shorter investment horizons, the index performance has shown consistent performance over long horizons – a critical requirement for any asset class.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend