Oh My! I Bought A Wrong Stock! – Investigation of Lead-Lag Effect in Easily-Mistyped Tickers

Introduction

Our new study aims to investigate the lead-lag effect between prominent, widely recognized stocks and smaller, less-known stocks with similar ticker symbols (for example, TSLA / TLSA), a phenomenon that has received limited attention in financial literature. The motivation behind this exploration stems from the hypothesis that investors, especially retail investors, may inadvertently trade on less-known stocks due to ticker symbol confusion, thereby impacting their price movements in a manner that correlates with the leading stocks. By examining this potential misidentification effect, our research seeks to shed some light on this interesting factor.

Investigating misspellings between stock tickers is an intriguing area of research that intersects finance, linguistics, psychology, and economics. Understanding this effect could provide valuable insights and translate into strategies that exploit such inefficiencies.

Background and related literature

A ticker symbol (also known as a stock symbol) is a unique abbreviation used to identify publicly traded shares of a specific company on a particular stock market. These symbols serve as shorthand for investors to identify and trade stocks. While the U.S. Securities and Exchange Commission (S.E.C.) grants companies reasonable discretion in selecting their ticker symbols, there are guidelines to follow. The chosen symbol must be original (not replicating another company’s ticker) and appropriate.

Companies try to come up with tickers that are easy to remember and unique. However, due to the high number of companies listed in the U.S., many companies have tickers that may be easy to confuse.

Existing Literature

The first concise article behind the development of our research was Typo Trading Analysis from Unusual Whales (section of “Typo Trading,” a.k.a. the Levenshtein Basket):

- They begin by stating that the advent of zero-commission trading and unprecedented accessibility to market knowledge through social media transformed the world of trading and investing, which especially “exploded” in 2020-2021 with the COVID crash and the first meme rally.

- But they further move into the topic of our interest today: “typo trading.”

- They also widely refer to Levenshtein distance, a string metric measuring the differences between two sequences; between two words, it is the minimum number of single-character edits (insertions, deletions, or substitutions) required to change one word into another.

- They provide plausible explanations for which this may work from fundamental PoV (point-of-view):

- Once the news that pushes the retail stock higher is released, this buying pressure leaks into stocks within the Levenshtein basket that is typically and otherwise uncorrelated.

- Smartphone trading encourages risky behavior, unintentionally involving trading different securities (e.g., relatively big fingers on a small keyboard).

The other possible things to take up for consideration are:

- Asian investors may also have difficulty differentiating between tickers, as their markets rely on numbers instead of the US market’s custom of letters for their stock tickers.

- Name and ticker confusion is more common than the “fat finger trades” issue when the wrong shares are bought due to an accidentally mistyped key. This is a recurring theme in popular financial outlets that try to inform about bombastic topics and sensations.

There are also many popular finance articles, but under the cover, there might be some applicable and testable things. The summary of the paper from two professors at the Rutgers School of Business-Camden, in a forthcoming issue of the Journal of Financial Markets, found that more than half of listed US companies share a “meaningful part” of their names or tickers with another firm, often in a separate industry and with a dramatically different market capitalization.

Of that group, there are around 250 company pairs where the possibility of confusion is particularly high, and a quarter of these showed statistically significant similarities in trading patterns that can only be explained by cases of mistaken identity. By their estimates, the trades made by mistake, on average, cost investors $1.1M per pair per year in transaction costs.

However, our goal is not to study intraday or daily drifts in stocks caused by typo trading in case there is some notable event in the leading stocks. We are more interested in studying whether there is a long-term drift in the mistyped stocks (for example, TLSA) if the leading stocks (for example, TSLA) perform well. Therefore, our study is more akin to papers that discuss linkages among related stocks.

One such related paper is by Hulley, Liu, and Phua, 2024, who in their Investor Search and Asset Prices demonstrates that a momentum portfolio strategy based on firm relatedness, identified through EDGAR co-searches, predicts future returns. These results are robust to controls for firm characteristics, returns from other spillover momentum factors, and known asset pricing anomalies. This robustness suggests that the EDGAR Co-search (EC) factor reveals unique information not captured by traditional relatedness measures. Importantly, EC factor returns can explain those based on shared analyst coverage, implying that EC encompasses the information contained within analyst networks.

It works since firms can have fundamental similarities and relatedness, such as operating in the same geographic area and industries, being customers/suppliers, etc. Understanding these relatedness has implications for cross-asset return predictability because information can flow through these linkages sluggishly.

We can mention more examples from a family of rich lead-lag relationships and effects. To list some more to keep track of, we can point you to our earlier in-house study Evaluating Long-Term Performance of Equities, Bonds, and Commodities Relative to Strength of the US Dollar, where we performed the cross-asset analysis to study the impact of the US Dollar’s strength or weakness on the performance of other asset classes, notably US equities, US treasury bonds, and commodities.

And at last, a few more examples:

- Lead-lag relationship between analyst-connected stocks, represented by Shared Analyst Coverage: Unifying Momentum Spillover Effects (Ali and Hirshleifer, 2019):

- By identifying firm connections through shared analyst coverage, the authors find that a connected-firm (CF) momentum factor generates a monthly alpha of 1.68% (t = 9.67).

- Corporate Equity Ownership and Expected Stock Returns from (Li, Tang, Yan, 2016):

- They investigate the cross-sectional predictive relations between stock returns of two public firms, with one firm, the parent, owning partial equity of the other, the subsidiary, and find that high past returns of the subsidiary (parent) predict high future returns of the parent (subsidiary)

Conceptualization of Our Study

So, our goal is to explore pairs data of some selected, often mistakenly bought and sold stock and investigate if there is a lead-lag effect. All inspirations for tickers, their initial feasibility testing, and either inclusion or exclusion are from the articles mentioned in the previous chapter.

The list of potential candidates collected using previous articles and papers was then evaluated for suitability for inclusion (Common name/ticker mix-ups from Quartz).

Many of our candidates were discarded (“kicked out”) because they

- were only newly created ETFs (with few traded days, hence the almost non-existent data sample),

- ones brought out,

- taken private or

- relegated to pink sheets (OTC) [did not meet regulatory requirements from NASDAQ, for example, such as a price of $1 at least),

- penny stocks.

- Some of the proposed alternatives (for example, ES [stock] / ES [futures]) were scrapped (possibly because it is a cross-asset relationship that we did not want to pursue and endure further at the moment).

Data

The data sample is 31.5.2019 – 31.3.2024, as the first date is of the union from the dates of all data available for all stocks.

We checked most of the stocks through Yahoo Finance with syntax https://finance.yahoo.com/lookup?s={{TICKER}} (where {{TICKER}} is, of course, replaced with the real-world candidate).

After feasibility due diligence, we gather historical stock ticker daily data from YF and filter and sample it for EOM (end of month) afterward.

Recently, Yahoo Finance discontinued free end-of-day data downloads. As a result, we recommend sourcing data from our preferred provider, EODHD.com – the sponsor of our blog. EODHD offers seamless access to +30 years of historical prices and fundamental data for stocks, ETFs, forex, and cryptocurrencies across 60+ exchanges, available via API or no-code add-ons for Excel and Google Sheets. As a special offer, our blog readers can enjoy an exclusive 30% discount on premium EODHD plans.

Our hypothesis is that larger companies (bigger market-cap) lead smaller companies (smaller market-cap).

| TSLA | Tesla, Inc. |

| F |

Ford Motor Company

|

| AAPL | Apple Inc. |

| HPE |

Hewlett Packard Enterprise Company

|

| RCM | R1 RCM Inc. |

| AMSWA |

American Software, Inc.

|

| SNAP | Snap Inc. |

| ZM |

Zoom Video Communications, Inc.

|

lead(s [stocks])

(Just wonder how many you know … and let’s compare this list to the second selection.)

| TLSA |

Tiziana Life Sciences Ltd

|

| FORD |

Forward Industries, Inc.

|

| AAP |

Advance Auto Parts, Inc.

|

| HP | Helmerich & Payne, Inc. |

| RCMT |

RCM Technologies, Inc.

|

| AMS |

American Shared Hospital Services

|

| SNA |

Snap-on Incorporated

|

| ZI |

ZoomInfo Technologies Inc.

|

lag[gards; lagging stocks]

And complimentary for comparison purposes, we downloaded data also for: SPY (SPDR S&P 500 ETF).

Lead-Lag Relationship

So, let’s take a closer look at whether it is also financially profitable to implement some kind of trading strategy that might benefit from these (costly) mistakes, often left unrecognized.

As explained a little bit earlier before, we take “more well known” (quantified by large market-cap) stock and compare it to “not so well known” (smaller market-cap) stock, with the assumption of lead-lag relationship: so when the “larger, bigger” stock moves (for the sake of simplicity, now either up or down, regardless of the amplitude of move) the move will be later also propagated in “less known, often mistakenly typed” stock.

We use EOM data about stocks and study the performance of leading stocks on 1M, 3M, 6M, and 12M period. If leading stock has a positive X-month performance (momentum) at the end of the month, we buy lagging stock into the portfolio for the subsequent month. Alternatively, if leading stock has a negative X-month performance (momentum) at the end of the month, we sell short lagging stock into the portfolio for the subsequent month.

We have two types of weighting:

1/ proportional (fractions) – where you take a portion of lagging stocks n that should be in the long leg of the portfolio (because their leading stocks have a positive performance) and weight it proportionally as 1/n (so you might have no stocks occurring in some months, or exactly 1/8 for each stock). Afterward, you take a portion of lagging stocks m that should be in the short leg of the portfolio (because their leading stocks have a negative performance) and weight it proportionally as 1/m.

2/ fixed – always 1/8 for each and every lagging stock in the portfolio, no matter if it’s in the long or short leg of the portfolio

Results

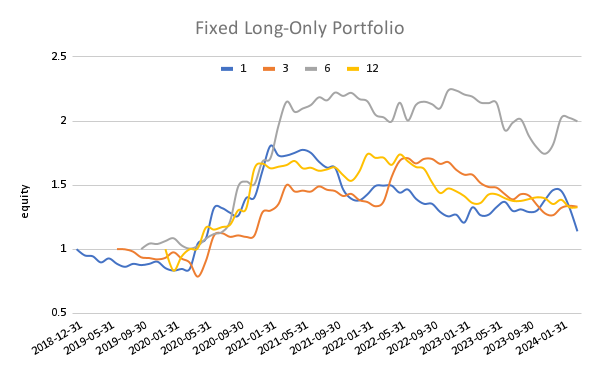

Firstly, let’s focus on long-only strategies, which is more convenient for interested retail investors. Later, we will also have a bit of a look into the long-short strategy variants.

Following are equity curves graphs and our quasi-standard table reporting of most important performance metrics:

The fixed long-only portfolio (1/8 weight allocated to each lagging stock when leader stock has a positive X-month performance) performs satisfactorily, except for a 6-month lag. Unfortunately, even though the performance of the long-only strategy is positive, it doesn’t beat SPY’s performance on a risk-adjusted basis over the same period.

Proportional weighting produces results that beat index investing, although with higher volatility, unfavorable Sharpe ratios, and maximal drawdown.

Now, in comparison to the list: SPY gained almost 20% annually during the aforementioned period, with favorable risk parameters beating out our proposed variants. Long-only strategies don’t look like a path to outperform the passive market (at least in this limited sample).

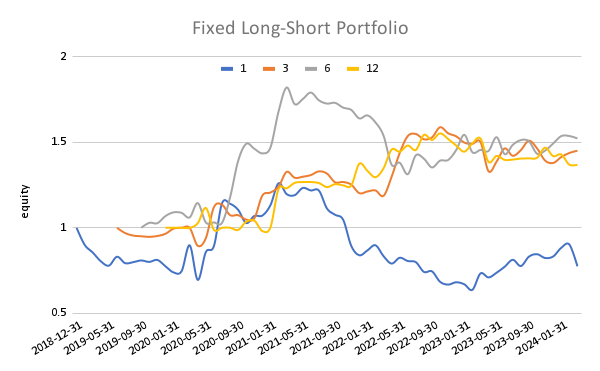

Now, let’s review the performance of long-short strategies, that use the fixed and also proportional weighting scheme.

Long-short strategies that use proportional weighting are quite volatile as, in some cases, only 1 or 2 stocks are in a short (or long) leg of the portfolio in any particular month. Therefore, their risk contribution is substantial. Long-short strategies that use fixed weighting are significantly less risky. Additionally, all medium to long-term sorting periods (3M, 6M, 12M) offer an interesting performance and Sharpe ratio for a market-neutral equity long-short factor strategy.

Conclusion

As mentioned, this article should serve just as a high-level overview of the lead-lag effect in misspelled (mistyped) stocks. Unfortunately, the disadvantage is that we have a small sample (8 pairs), which was arbitrarily chosen, and there might be significant subjectivity in the process. Our backtest period is also somewhat limited.

What should be the next steps? Our interest will be turned towards extending the sample of the pairs by systematizing the selection of pairs. Additionally, we will be looking for a way to extend the backtest period to see the effect’s performance over a longer history. However, even in this small universe, our article shows that there definitely is a potential to exploit the proposed lead-lag relationships, and this effect justifies further study.

Author: Cyril Dujava, Quant Analyst, Quantpedia

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend