Stock-Bond Correlation, an In-Depth Look

The recent surge in global inflation sent shock waves across financial markets and affected the complicated relationship between stocks and bonds. Today, we would like to present you with a review of two interesting papers, which provide both a deep and easy-to-understand examination of the correlation structure of those two main asset classes. The first paper reviews specifics in various parts of the world, and the second one summarizes known information about the macroeconomic drivers of the US stock-bond correlation.

Stock-Bond Correlation: A Global Perspective

The first paper reiterates the crucial statement that stock-bond correlation is considered one of the most, if not the most important input for multi-asset portfolio construction. Negative stock-bond correlation, which is present in Developed Markets (DMs), provides an implicit hedge of one asset to the other, dampening overall portfolio risk. Noah Weisberger and Xiang Xu (June 2021) investigate the specifics of these effects in other parts of the world, especially Emerging Markets (EMs). In the case of a local stock-bond correlation regime change from negative to positive, there is a need to alter the expected risk-reward characteristics of a portfolio of local assets and change the parameters of hedging. They advise CIOs and asset allocators to look through the findings thoughtfully, which can provide significant inputs and possible ideas for models that can help to assess possible global risk.

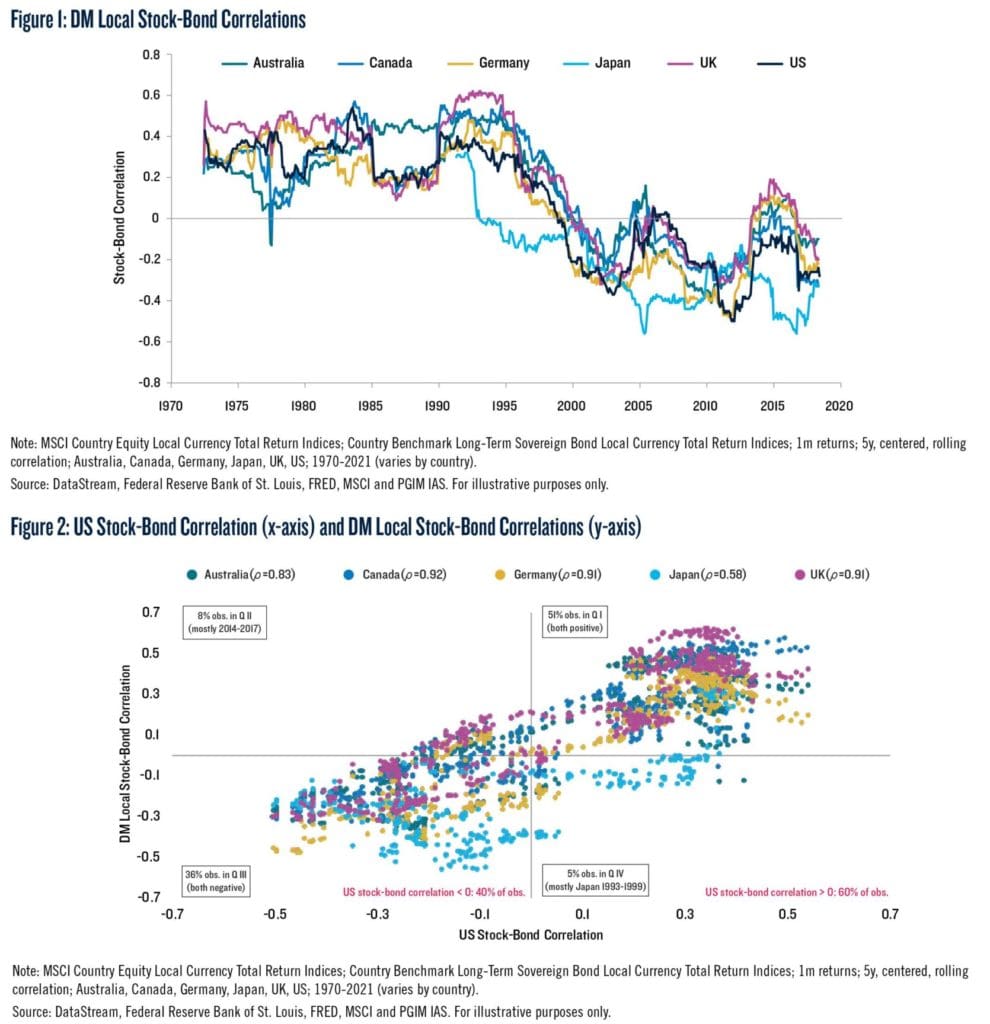

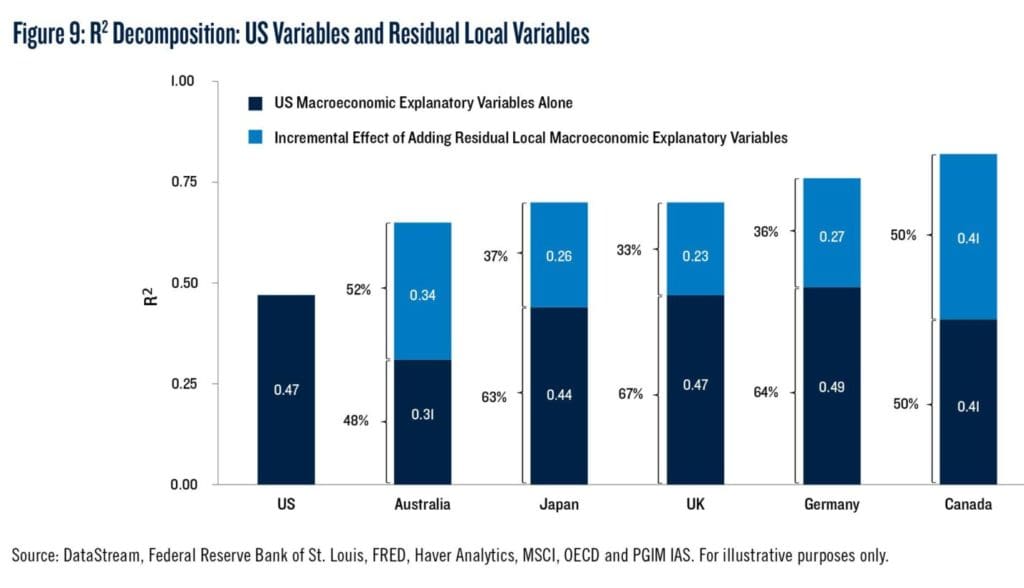

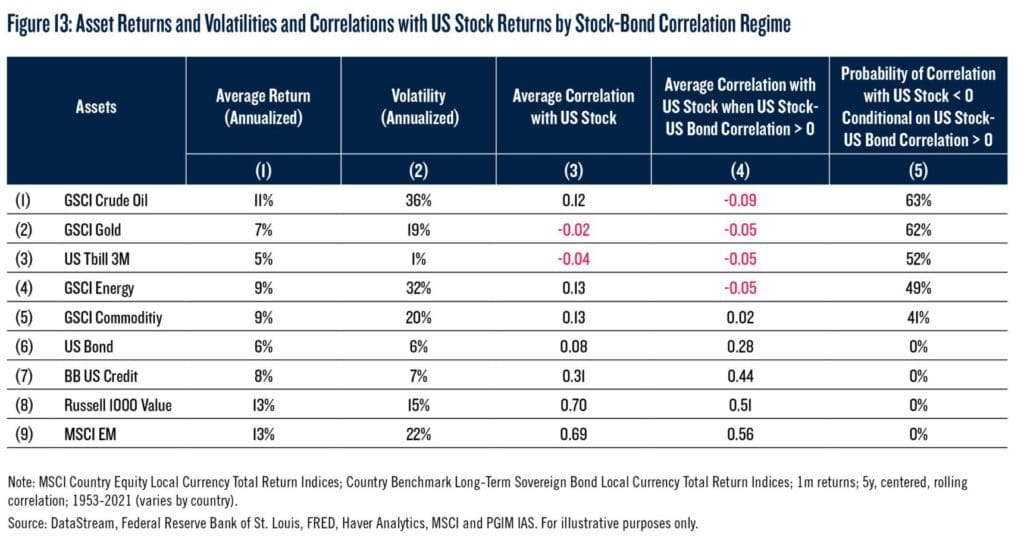

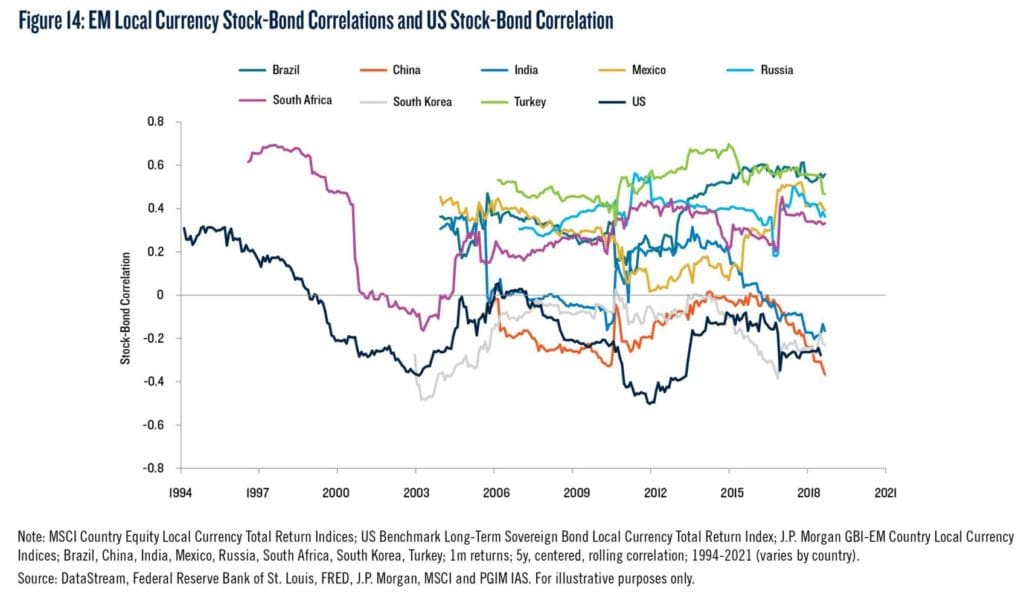

Looking across six DMs (Australia, Canada, Germany, Japan, the UK, and the US), the authors observed that changes in local currency stock-bond correlations are synchronized (Figure 1). Indeed, the correlation of DM local currency stock-bond correlations with US stock-bond correlation is different and ranges from a high of 0.92 for Canada to 0.58 for Japan (Figure 2). They found the most interesting and useful results from using Model 3, which combines both sources of variation in local stock-bond correlation and apportions explanatory power to US variables (as the global proxy) and to local effects (net of US influence). Its R² is in Figure 9. Beyond DM sovereign fixed income, when the US stock-bond correlation is positive, Oil, Gold, and Energy total returns are negatively correlated with US stock returns. Figure 13 summarizes this finding: negative correlations are, however, relatively small, and hedging comes at the cost of higher volatility.

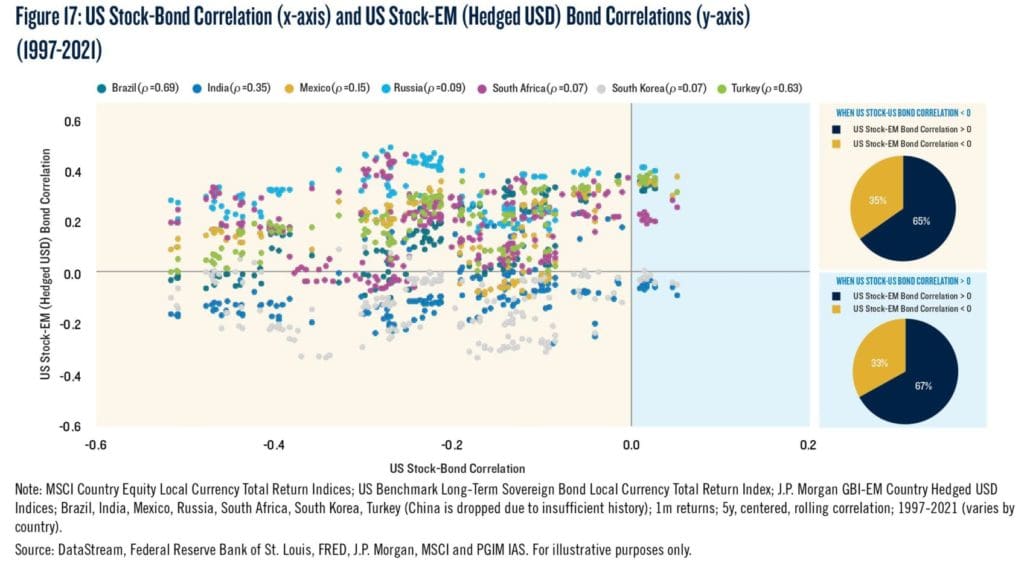

Unlike DMs, where stock-bond correlation has been persistently negative for the last 20 years, EM (local currency) stock-bond correlations have been mostly positive since 2000 but not uniformly so, as can be seen from Figure 14. In Figure 17, we can see EM (hedged USD) bond returns have generally been positively correlated with US stock returns, even when the US stock-bond correlation was negative.

US Stock-Bond Correlation: What are the Macroeconomic Drivers?

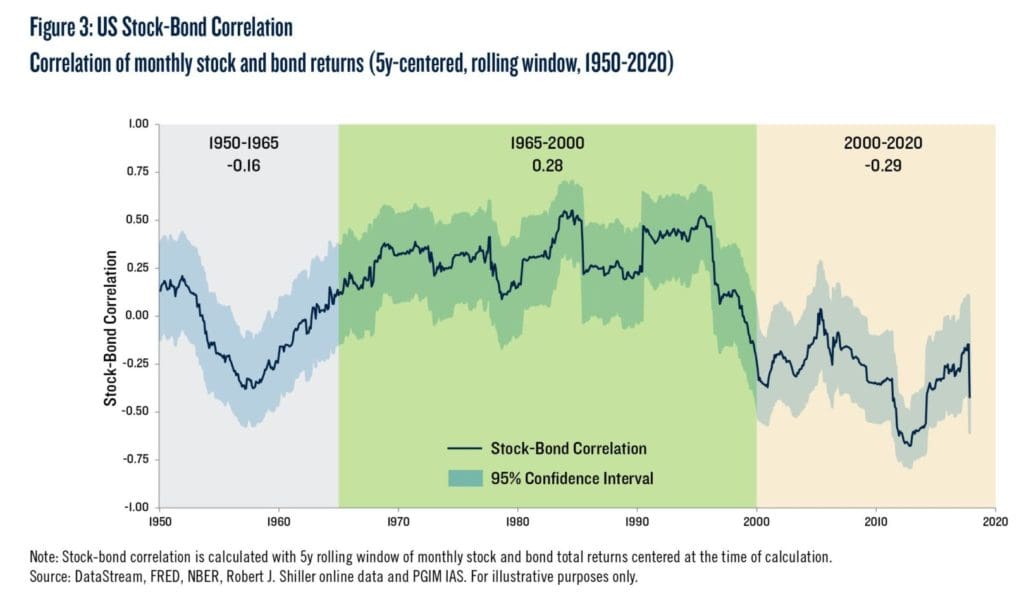

Building on previous themes, Junying Shen and Noah Weisberger (June 2021) 2nd paper provided interesting perspectives into various important macroeconomic conditions which drive both negative and positive correlations, such as monetary and fiscal policy. US stock-bond correlation, which plays an important role in institutional portfolio construction, has been persistently negative for the last 20 years. This negative correlation allows stocks and bonds to serve as a hedge for each other, enabling CIOs to increase stock allocations while still satisfying a portfolio risk budget. However, the stock-bond correlation is not immutable. In fact, it was consistently positive for more than 30 years prior to 2000. A return to positively correlated stock and bond returns may require hedge fund managers to rethink their asset allocation.

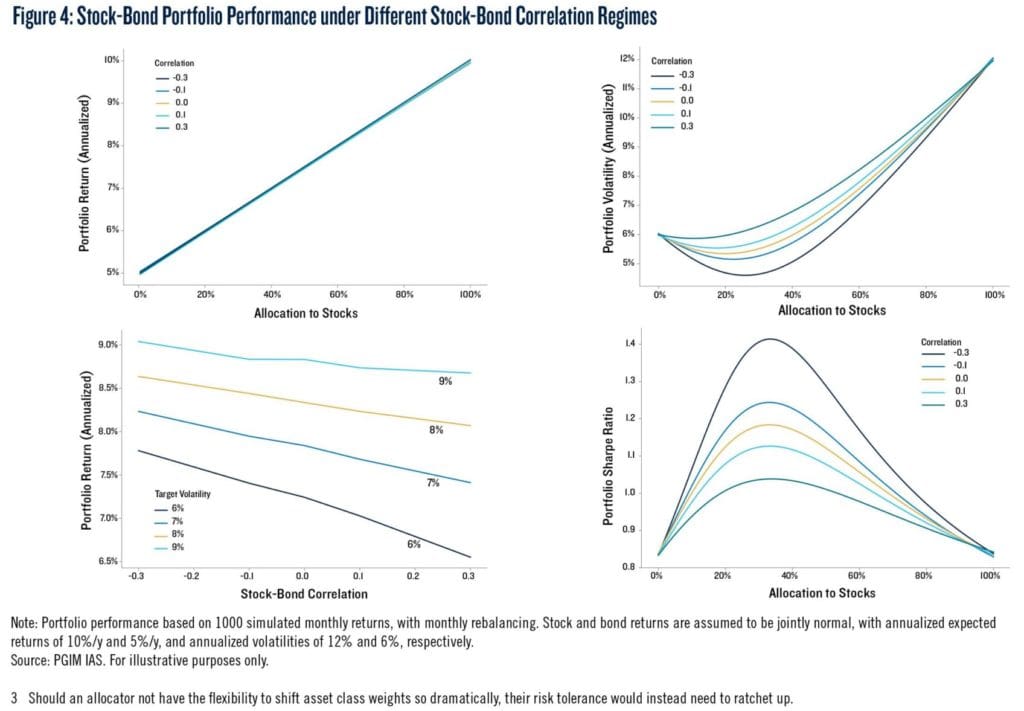

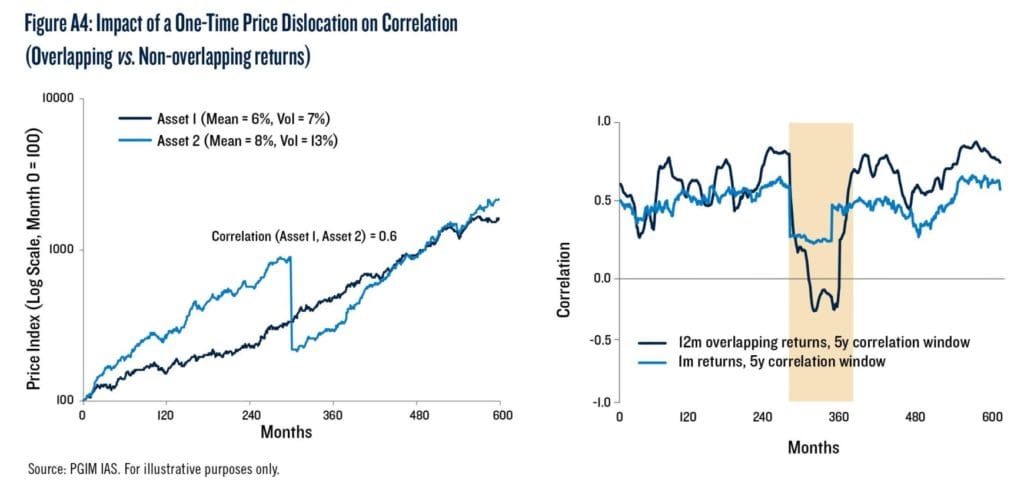

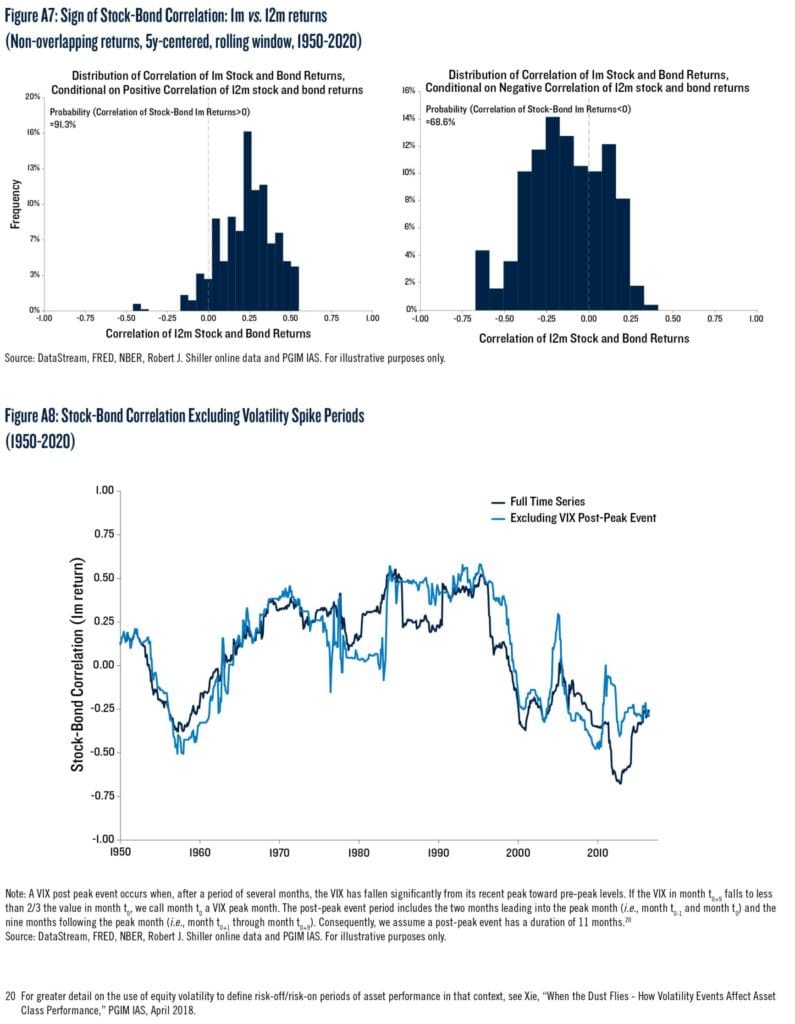

Authors estimated stock (S&P 500) – bond (10y Treasury) correlation using monthly total returns over a centered, rolling 5y window from 1950 to 2020 and compiled nice Figure 3. Portfolio returns vary little as correlation change, as shown in Figure 4, but it discusses other important aspects of CIOs’ portfolio volatility and Sharpe ratios which needs to be managed as well. The fact that the correlation of overlapping long-term returns will absorb and amplify (i.e., by increasing the number of observations where the two asset returns are of opposite sign) the one-off disconnect and will remain negative for a protracted period can be seen from Figure A4. Figures A7 and A8 confirm that short-term return and long-term return regimes are consistent, and negative correlation regimes are not just due to “risk-off” dynamics.

Conclusion

Institutional investors whose work is to form well-suited portfolios need to choose the right asset allocation to achieve firm returns for their clients. The analyzed articles provide help asset managers and CIOs evaluate the potential for a change in both US and global stock-bond correlation, identify the underlying macroeconomic components of the correlation, and show how changes in these components have been linked to changes in monetary and fiscal policy over the last 70 years. It is important to realize that neither theory nor history points to a single factor that determines the correlation regime, and there are many, sometimes even contradictory, indicators that signal regime change. Persistently continuing falling and low-interest rates we have been used to in recent years alone may not be enough to support a negative correlation. Today’s challenging environment with the unprecedented rise of inflation competes with different aspects and characteristics of widening ranges in different parts of both DM and EM, and there is a need to be aware of possible implications.

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend