As of the first half of August, the year 2021 seems to be a phenomenal year for equities. World equities have earned more than +16% and US equities even more, topping +20% gains. Is there even any better strategy this year, than just holding US equities? Well, yes, there are actually several of them. Are they all tied to US equities? Many of them are, but many of them are not. Some of them are not even tied to equities at all.

Note: This blog is Part 1 of a series. Part 2 and Part 3 are now available.

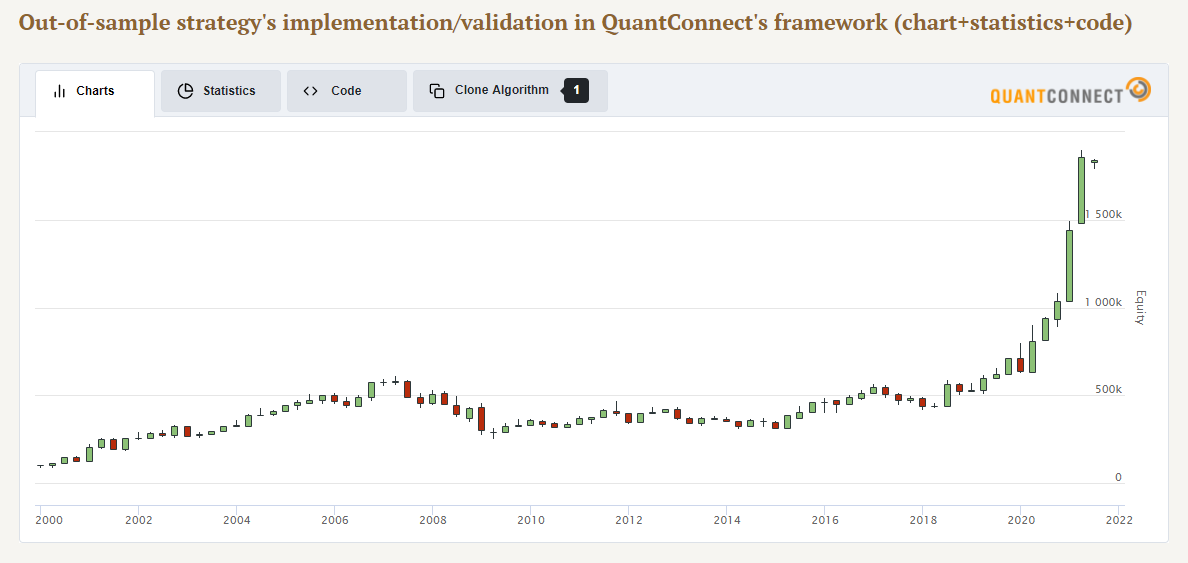

As a little teaser to start with, this is the equity curve of #3 best quantitative strategy of 2021 so far:

How to find best performing strategies in 2021

When asked “What was the best strategy so far in 2021?” many would reply “just hold US equities“. Some of them would reply “hold Commodities“. Yet, none of these answers is entirely correct. We may use Quantpedia Pro Screener and answer this question in a matter of seconds.

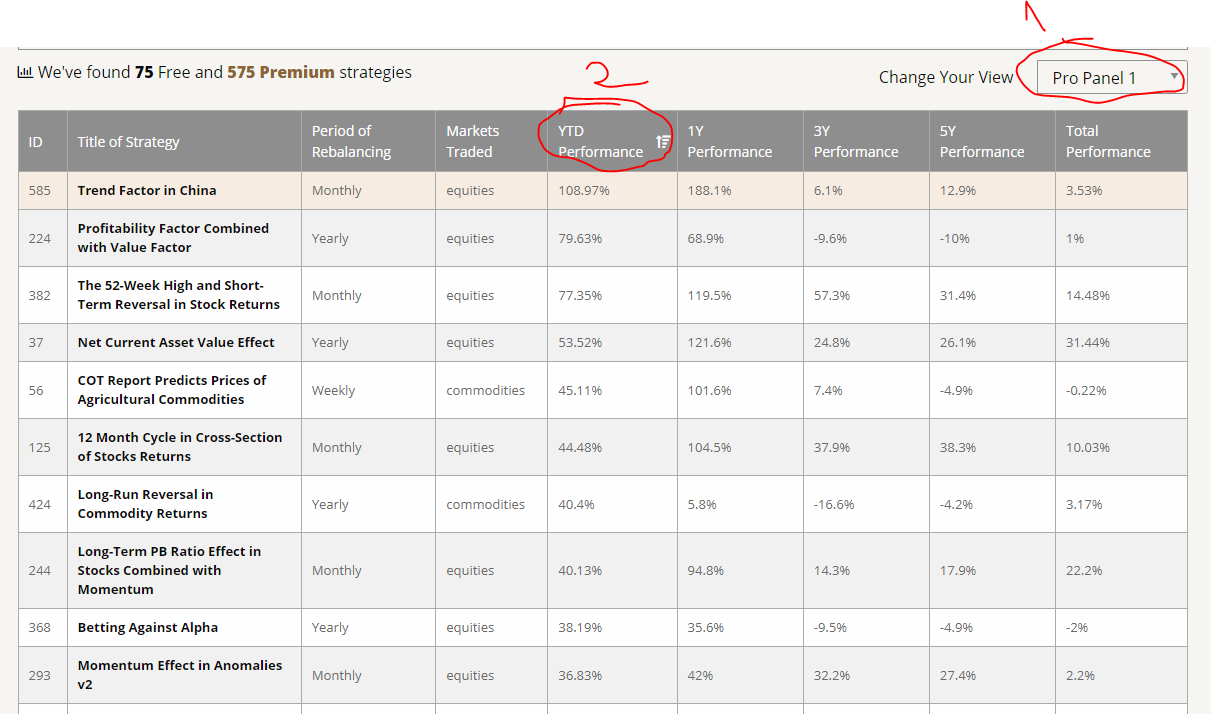

So let’s firstly pick a Pro Panel view and let’s secondly sort 350+ Quantpedia’s backtested strategies with live performance. This is what we’ll get:

The respondents were indeed somewhat right in their answers. Among the top 10 quantitative strategies of 2021 we can observe 8 strategies tied to equities and 2 strategies tied to commodities. Were these strategies just passively holding these asset classes, though? Not at all. Just looking at their performance range of +36.8% to +109% tells us that these strategies needed to be active to achieve such returns.

Are best strategies correlated with US equities?

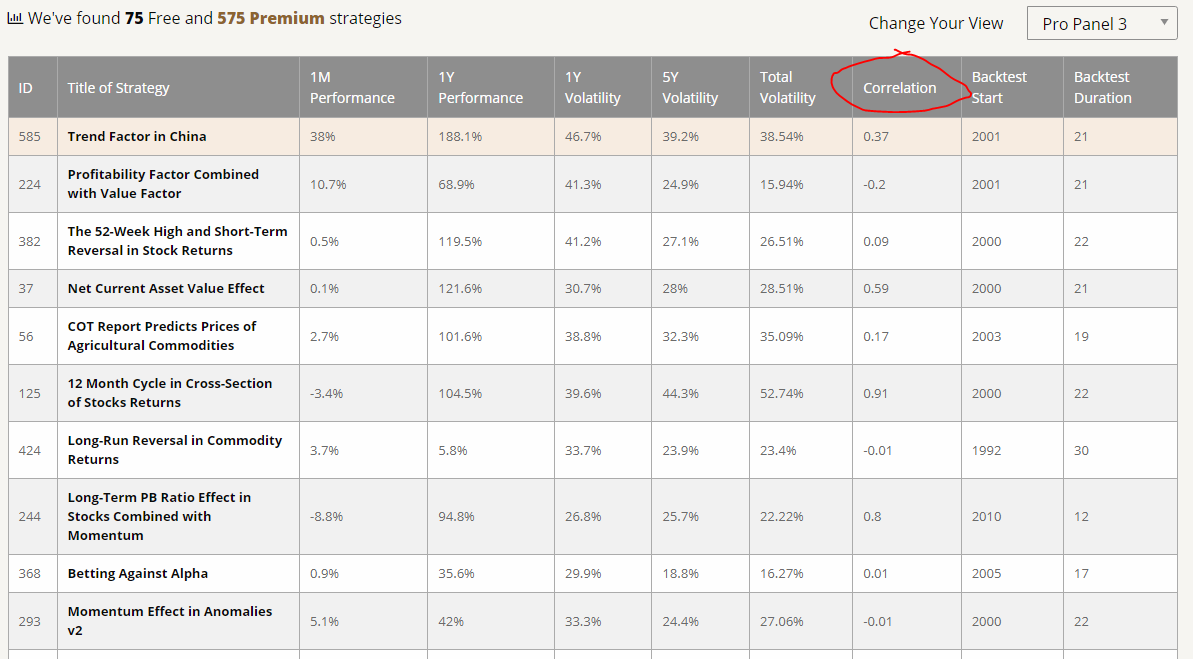

Another nice feature of Quantpedia’s Pro Screener can easily show us how correlated these strategies are to simply “holding US equities”. Let’s observe a Correlation column of Pro Panel 3:

As we can see, actually only 2 of the strategies are highly correlated to US equities, the “12 Month Cycle in Cross-Section of Stocks Returns” strategy and the “Long-Term PB Ratio Effect in Stocks Combined with Momentum” strategy. The 6 out of 10 best performing strategies even have a correlation to US equities close to zero!

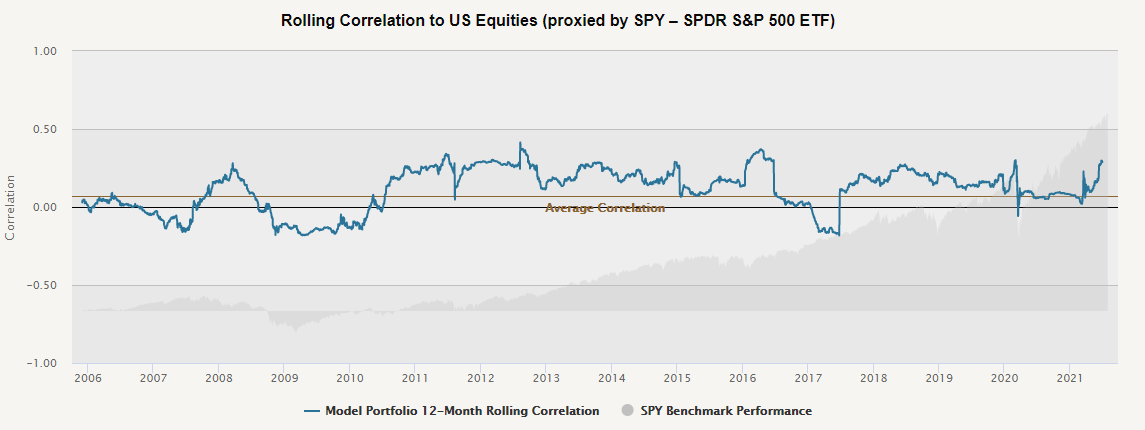

These are long term correlations, which is good on the one hand (we have enough data points), but may be too long, on the other hand, to assess the current development of the strategies. Is it possible to dynamically assess short-term correlation developments in time? Of course it is – Quantpedia Pro has another ready-made tool for that, which is a Correlation report in Quantpedia Pro’s Portfolio Analysis section:

Return and risk of the top strategies

Another 2 interesting insights into top performing strategies of 2021 are available straight away thanks to Quantpedia Screener’s Pro Panel 2. This time they are related to the risk of the strategies and persistence of their returns.

We may observe in the Pro Panel 2 that the long-term risk of all this year’s winning strategies is high. Historical maximum drawdown exceeded -50% in all of the cases. This signals that high returns achieved by the strategies do not come as a free lunch and one must endure a substantial amount of risk.

The second interesting observation is persistence of strategies’ returns. Long story short – their return persistence doesn’t seem to be very high. Previous year performance is often negative and even a 5-year performance may be negative.

This only underlines the importance of constantly adapting to contemporary market conditions and not relying on only one type of strategies.

Are the best performing strategies similar?

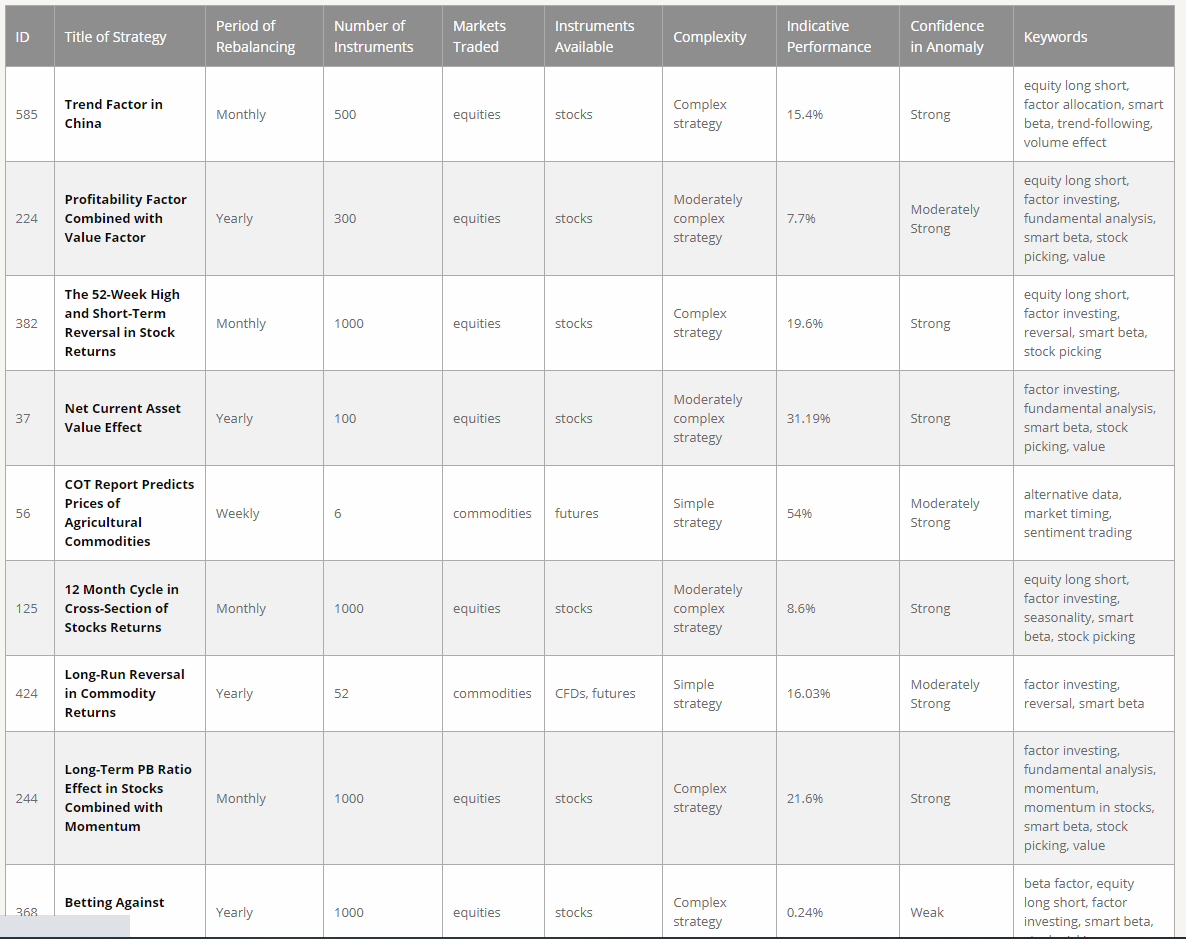

Short answer would be no. The more detailed analysis can be performed by Quantpedia Premium screener view labeled Descriptive.

We may easily observe that strategies significantly differ in their:

- trading frequency

- number of assets traded

- actual instruments traded

- type of the strategies

What exactly are the best strategies in 2021?

Now we know that the best performing strategies Year-To-Date are mostly tied to equities, but not exclusively. We also know that, although the strategies are mostly tied to risky assets, their correlation to US equities is, in most cases, very low.

We have successfully analyzed multiple patterns across the top quantitative strategies of 2021. However, the question everyone surely remains curious about is – what exactly are the best performing strategies? No worries, we will come to it in Part 2 of our blog series at the end of the week. Stay tuned.

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend