The Best Systematic Trading Strategies in 2021: Part 2

The year 2021 has been an incredible year for passive equity investors so far. However, in the first part of our article, we talked about quantitative strategies which achieved even better results in 2021 than passive US equity investors. Indeed, there do exist such strategies, at least definitely in Quantpedia’s database of 650+ trading strategies.

We focused the first part of the article more on tendencies and trends among the best quantitative investment strategies of 2021. We found out, thanks to Quantpedia Pro’s screener abilities, several interesting insights, for example among others also:

- The top 10 strategies are (unsurprisingly) tied to equities and commodities

- Best strategies are generally NOT highly correlated to US equities, though

- Top-performing strategies of the year tend to be the riskier ones

- Best strategies do fluctuate. One needs to adapt constantly

- Some of the past year’s losers became this year’s winners

- Top 2021 strategies differ substantially in the universe they trade, trading frequency and strategy type

Today we will talk more in deep about specific top-performing strategies of 2021 (as of August 2021). So, let’s go straight to the thing! Transaction costs and bid-ask spreads are included in all of the charts below.

So, the top-performing strategies of 2021 are …

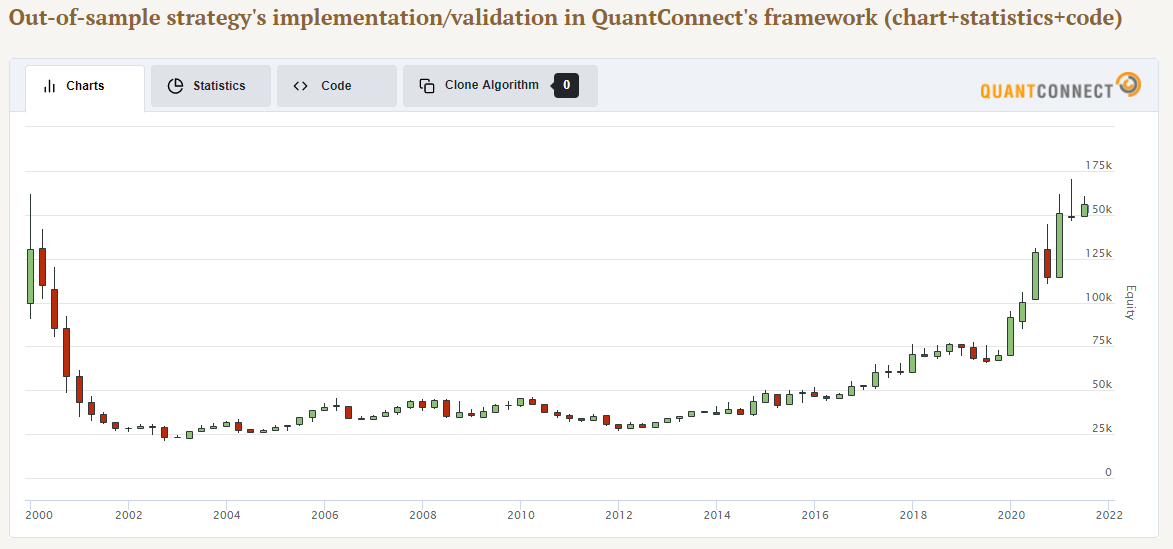

#10 Momentum Effect in Anomalies

YTD performance: +36.83%

Assets: US stocks

# Instruments: 1000+ NYSE, AMEX and NASDAQ stocks

Frequency: Monthly

Max Drawdown: -43.1%

Strategy idea: long-short best-worst performing factors/anomalies

As we all know, anomalies don’t work all of the time. One needs to constantly adapt, evolve and adjust their exposure towards specific factors to become successful. One of the ways to adjust the exposure towards anomalies is to use their momentum, a.k.a. recent performance.

Factor momentum is a well known phenomenon in academia. Despite being risky, the momentum effect in anomalies is thriving in 2021 and belongs to the group of 10 best performing strategies.

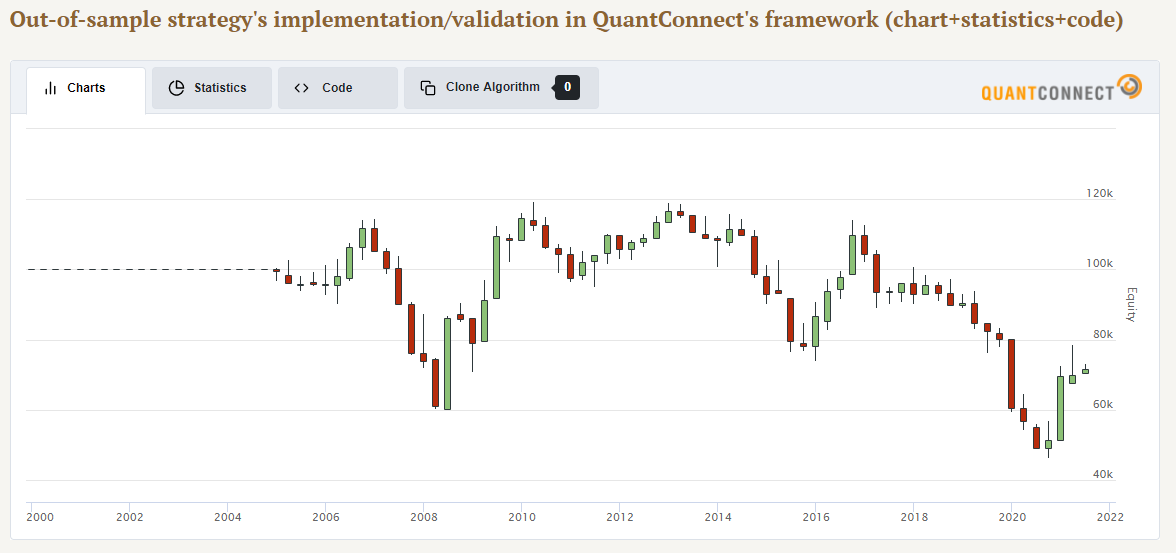

#9 Betting Against Alpha

YTD performance: +38.19%

Assets: US stocks

# Instruments: 1000+ NYSE, AMEX and NASDAQ stocks

Frequency: Yearly

Max Drawdown: -61.2%

Strategy idea: long-short low-high CAPM alphas

As we can see, not only momentum has worked so far in 2021. Reversal strategy, when used cleverly, has achieved even higher performance. We have to note that it’s hard to achieve long-term, stable outperformance with this version of reversal strategy. However, when timed correctly, it can significantly enhance one’s portfolio.

Stock reversal can be measured and defined in an endless number of ways. One of them is an alpha from the cross-sectional regression. And exactly this is what the Betting against alpha strategy does.

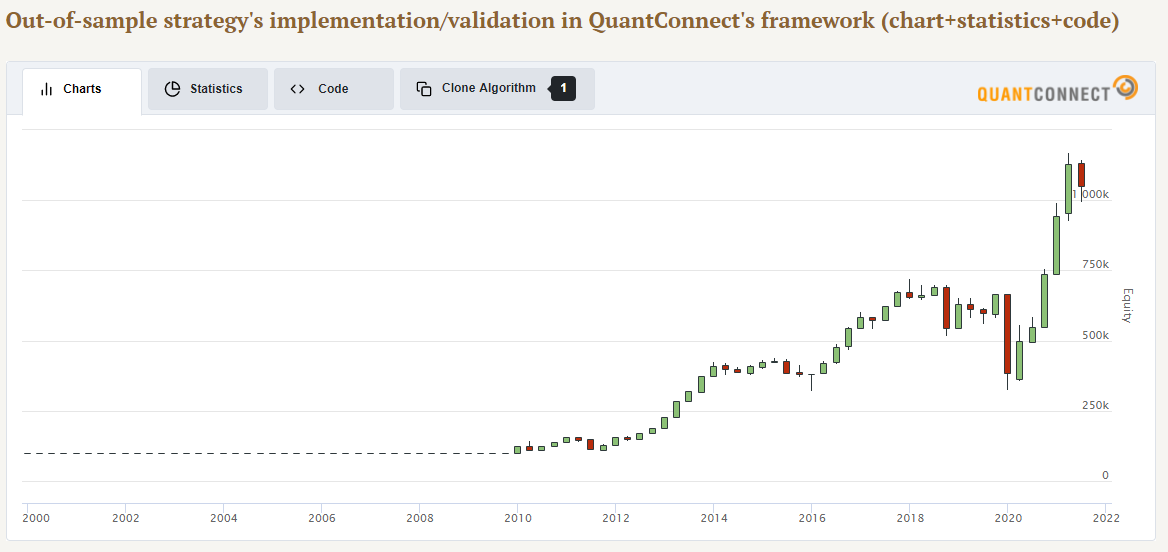

#8 Long-Term PB Ratio Effect in Stocks Combined with Momentum

YTD performance: +40.13%

Assets: US stocks

# Instruments: 1000+ NYSE, AMEX and NASDAQ stocks

Frequency: Monthly

Max Drawdown: -54.8%

Strategy idea: long high adjusted P/B, high momentum stocks

Not all Value strategies have underperformed in 2021. We actually even have 2 value-related strategies among our list of top 10 performing strategies. One of them combines momentum with an old-school P/B ratio.

P/B ratio may still serve as a very simple value measure and help on specific occasions, in spite of being condemned by many professionals. When combined with momentum, this strategy performed well in 2021.

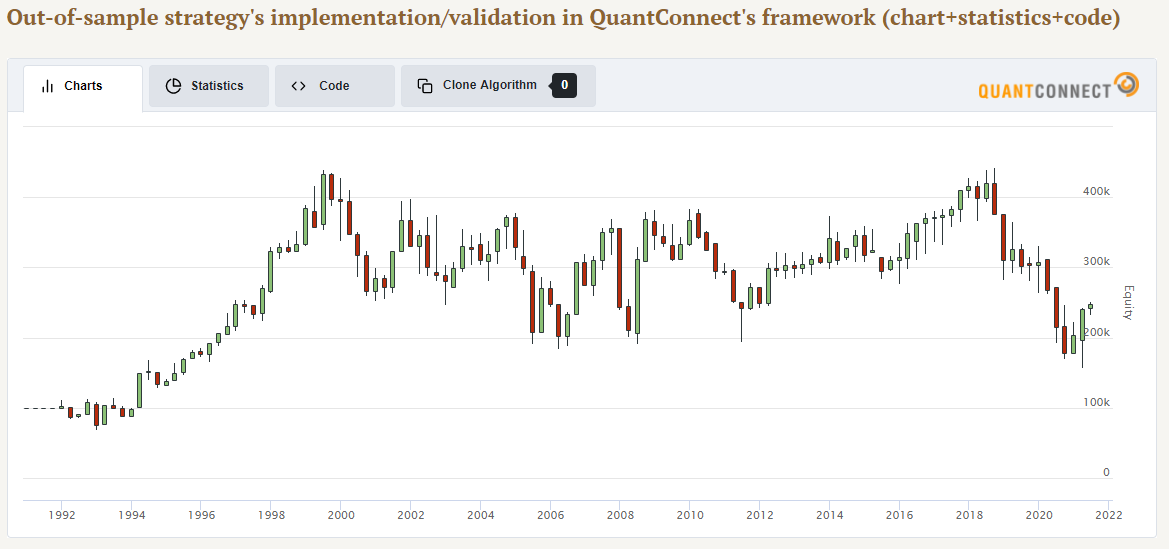

#7 Long-Run Reversal in Commodity Returns

YTD performance: 40.4%

Assets: Commodity futures

# Instruments: 52

Frequency: Yearly

Max Drawdown: -64.4%

Strategy idea: long-short worst-best long-term performing commodities

Another reversal strategy has made it into our list of best-performing strategies of 2021. This time it’s applied to a broad commodity futures’ universe. Similarly to stock reversal strategies, it’s not easy to achieve a long-term stable outperformance with this systematic commodity factor strategy. It seems that reversal-based signals do not have the high predictive ability in commodities in the long term and momentum or skewness based strategies perform better.

However, since 2021 has been a reversal year for several commodities, the strategy earned significantly positive returns and participated in many strong commodity moves.

#6 12 Month Cycle in Cross-Section of Stocks Returns

YTD performance: +44.48%

Assets: US stocks

# Instruments: 1000+ NYSE and AMEX stocks

Frequency: Monthly

Max Drawdown: -91.5%

Strategy idea: long-short stocks based on their recent seasonality

Specific seasonality-based strategies have been very successful in 2021 as well. One such example is the 12-month cross-sectional stock cycle strategy.

Although being risky in the long-term, the strategy performs astonishingly well in recent years, even when applied to larger stocks, which is not the case very often with many strategies.

Conclusion

We may observe that the top-performing strategies of 2021 are quite diverse and not that much related to each other. Some of them are performing really well already for a longer period, while others had started performing strongly only recently.

In today’s article, we looked at number #10 to number #6 best quantitative strategies of 2021 from Quantpedia’s database. We leave the Best 5 Trading Strategies for the next time. Stay tuned!

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend