The foreign exchange market (FOREX) is opened 24 hours a day, but traders from different parts of the world tend to prefer different trading hours, including weekend day trading. However, various dominant trading sessions around the globe can lead to time-dependent market characteristics. Novel research by Doman and Doman (2020) has studied how does the daily volatility of FX rates depend on the time of day of calculation. The volatility changes through the day, and the underlying dynamics depend on the time of the estimate. The results can have important implication for practitioners since the volatility differences are large enough so they can influence trading/risk management decisions.

Authors: Małgorzata Doman and Ryszard Doman

Title: How Does the Daily Volatility of Foreign Exchange Rates Depend on the Time of Day at Which the Daily Returns Are Calculated?

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3651344

Abstract:

In the paper, we show how the estimates of the daily volatility of major exchange rates, EUR/USD, AUD/USD, GBP/USD, and NZD/USD, depend on the hour at which the daily returns are calculated. FOREX market is open 24 hours a day, but traders from different parts of the world, if some local time is fixed, are most active in different times of a day. This is the reason why the dynamics of volatility changes during a trading day. To analyze this feature, we consider daily returns calculated using the exchange rates quoted at each full hour of a day. Volatility (the square root of the conditional variance) is described by means of GARCH models. The approach used enables us to scrutinize changes in the volatility, depending on the hour of a day, which can be useful in risk management. We investigate separately bid and ask prices, so we obtain some results concerning microstructure of the FOREX market as well.

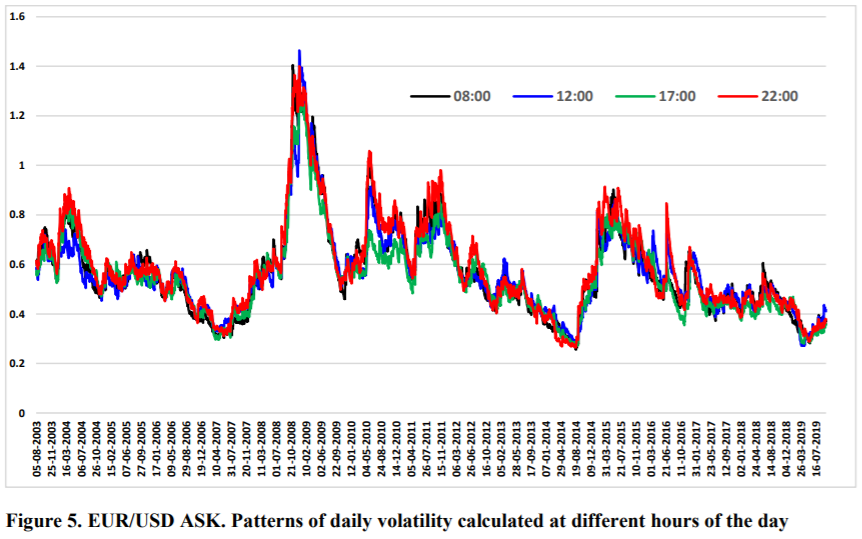

The differences are evident from the following chart (an example for EUR/USD pair):

Notable quotations from the academic research paper:

“The FOREX market is open 24 hours a day, with the exception of weekends (Table 1). More precisely, it works from Sunday around 20:00 LDN to Friday around 22:00 LDN (Donnelly 2019). Trading between the FOREX participants is conducted through electronic communication networks in various markets around the world. Decentralization implies that currencies are quoted almost continuously. The level of daily FOREX activity, however, varies, depending on the time of day. Extensive research literature exists, which studies the subject from the perspective of the market microstructure of FOREX markets, using high frequency data (e.g. Andersen and Bollerslev 1998, Baillie and Bollerslev 1991, Breedon and Ranaldo 2013, Ranaldo 2009). Our interests are somewhat different. We are going to examine how the diversity in FOREX activity during a day can impact on estimation of daily volatility of foreign exchange rates, which could be usable in risk management. For instance, a question appears if the choice of daily volatility estimates calculated using exchange rates observed at some specific time of day could produce desirable Value-at-Risk (VaR) estimates.

| Algo Trading Promo Codes are available exclusively for Quantpedia’s readers. |

The differences between the volatility estimates corresponding to different hours are visible. For daily returns calculated at some hours of the day (mostly corresponding to the opening or closing of national markets) they are quite clear. Usually, the differences are large enough to impact VaR estimates. This means that the portfolio managers from different parts of the world can perceive exactly the same position as more or less risky since they usually use the daily data quoted at the hours when their local market is active. They are also able to affect VaR estimates, choosing the hour at which they collect the data. Moreover, significant differences in the behavior of the volatilities for bid and ask prices that we

discovered for daily returns calculated at some hours, may reflect temporal imbalances between demand and supply side of the markets.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you interested in forex trading? Then you may check Admiral Markets review.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend