The Risk in Equity Risk Factors

The bear markets were and surely would be present in the equities in the future. While many fear them, experienced investors accept that the growth of the equity market cannot be constant and that inherent equity risk often manifests as a painful market drawdown. When someone designs a strategy, it is a general practice to check its performance during such downturns. Therefore, we can recommend an interesting novel research paper by Paul Geertsema and Helen Lu. The selected paper analyzes the risk of the most common equity factors and plots their over- or under-performance during multiple crisis periods since the Vietnam war until the COVID-19.

Authors: Paul Geertsema, Helen Lu

Title: Where Is the Risk in Risk Factors? Evidence from the Vietnam War to the COVID-19 Pandemic.

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3609007

Abstract:

During the COVID-19 pandemic (Jan 2020 – Mar 2020) all of the Fama and French (2018) factors except momentum lost money. Negative payoffs in a bad state would appear to justify the positive premia generated by these risk factors. But this is atypical – historically the value, profitability, investment and momentum factors are all more profitable in bear markets. The five non-market factors exhibit their own bull and bear market phases, but these do not correlate with the economic cycle. Factor profitability in bear markets arise primarily from the short side. Biased expectations corrected around earnings announcement offer only a partial explanation.

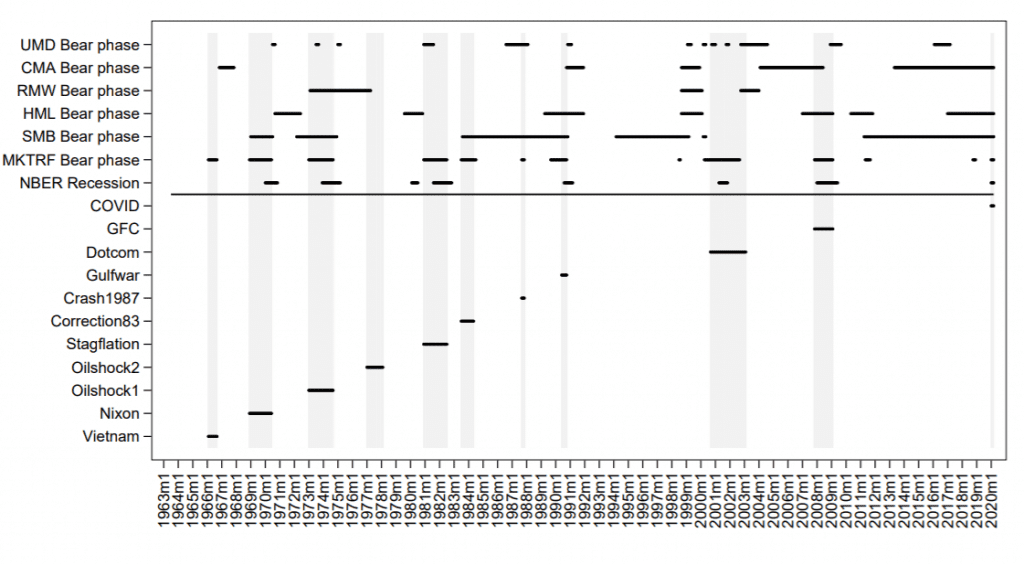

The risk or to be more precise, drawdowns, can be best understand from a simple chart, where drawdowns are plotted along with known bear markets.

“The figure below plots bear market states for the factors of the Fama and French (2018) six-factor model, along with 11 individual bear markets (see Table 1). The factor bear markets are indicator variables identified by applying the approach of Lunde and Timmermann (2004) to the cumulated returns of the individual factors.”

Notable quotations from the academic research paper:

“Factor performance during the COVID-19 pandemic is not representative of the previous 10 bear markets from the Vietnam War to the Global Financial Crisis (GFC). Of the five non-market factors in the Fama and French (2018) six-factor model none generate statistically lower returns during bear markets than during bull markets. The SMB size factor is the only factor with lower returns in bear markets than bull markets, but the difference is not statistically significant. Instead, in bear markets all non-market factors in the six-factor model of Fama and French (2018), aside from the size factor, generate large and significant returns on average. These bear market returns are an order of magnitude larger than in bull markets. Clearly this is difficult to reconcile with models based around risks to consumption or wealth.

When we consider all 11 bear markets individually, COVID-19 stands out because five of the six Fama and French (2018) factors generate highly significant and negative average monthly returns. During the COVID-19 period CMA incurs the smallest average monthly loss (−1.22%) and HML incurs the largest average monthly loss (−8.13%) among the non-market factors. UMD is the only profitable factor during COVID-19, with an average monthly return of 4.59%. In each of the 10 prior bear markets, profitable non-market factors outnumbered loss-making non-market factors.

The individual factors bear markets do not exhibit any commonality among themselves or with our state variables. Instead factor bear markets appear to reflect the unique circumstances of each factor at the time, instead of systematic risk across business cycles.

We find that all non-market factors (except SMB) generate substantially higher average monthly returns in bear markets than in bull markets. Such bear market profitability can not be readily explained by consumption based risk because high payoffs in bad states should be associated with negative risk premia. This inconsistency with risk based explanations might be related to limits to arbitrage since the bear market profitability of factors primarily comes from the short side.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend