The Tranching Dilemma

What if a meaningful part of a usual trading strategy’s performance has nothing to do with your signal—but simply when you rebalance? A recent paper written by Carlo Zarattini & Alberto Pagani highlights a largely underestimated risk in systematic investing: rebalance timing luck (RTL). For practitioners running rotation or factor strategies, this is not noise—it’s a structural source of dispersion. Using a concentrated U.S. equity momentum strategy, the authors show that identical portfolios differing only by rebalance day can diverge by as much as ~350 bps in annual returns, compounding into dramatically different terminal wealth outcomes.

From a portfolio manager’s perspective, this is critical: two funds with the same process can produce materially different track records purely due to implementation timing. This complicates manager selection, backtest validation, and even internal performance attribution. In practice, RTL behaves like an uncompensated risk—unforecastable, persistent, and difficult to hedge.

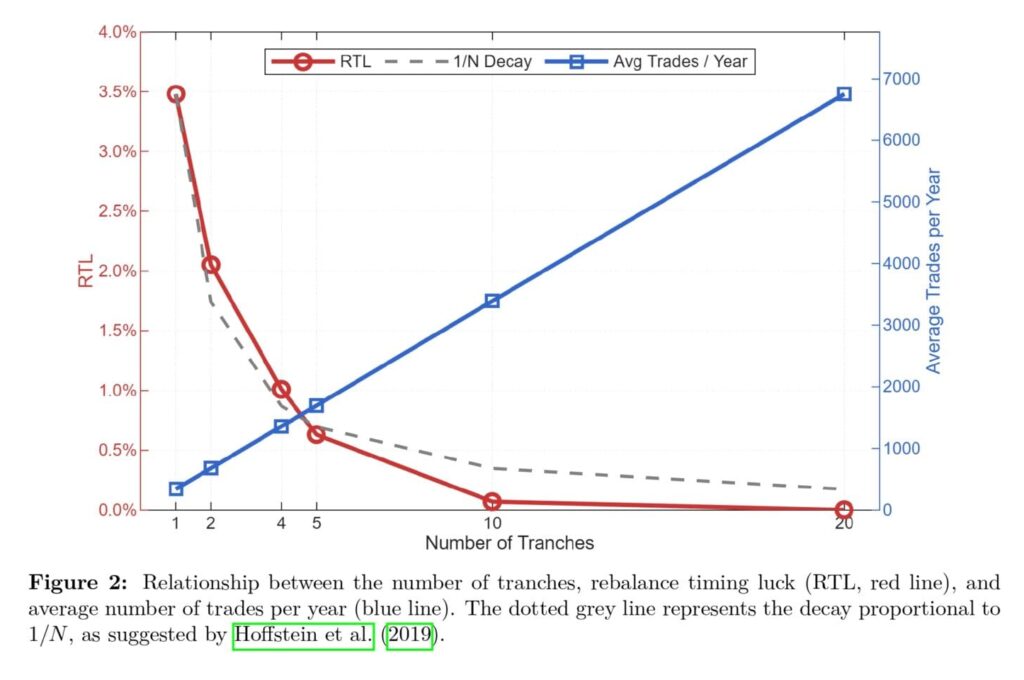

The proposed solution—portfolio tranching—is operationally simple but conceptually powerful. By splitting the portfolio into multiple sub-portfolios rebalanced on staggered schedules, you effectively diversify your timing risk. The paper confirms that RTL declines roughly with 1/N (number of tranches), while average returns remain unchanged. For practitioners, this reframes tranching not as alpha generation, but as variance reduction in realized outcomes—particularly relevant for high-turnover strategies like momentum where signal decay and ranking instability amplify timing sensitivity.

However, the key practical insight is cost-awareness. Once transaction costs and market impact are introduced, the optimal number of tranches becomes AUM-dependent. Small portfolios (e.g., $25K) are better off with minimal tranching (≈2 tranches), as trading frictions dominate benefits, while institutional portfolios benefit from aggressive tranching due to reduced market impact. The takeaway is clear: tranching is not a free lunch—it’s a design choice that must be calibrated to portfolio size, turnover, and execution constraints. For practitioners, this paper provides a concrete framework to align implementation with scale, rather than blindly adopting academic best practices.

Title: The Tranching Dilemma. A Cost-Aware Approach to Mitigate Rebalance Timing Luck in Factor Portfolios

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5747964

Abstract:

Rebalance Timing Luck (RTL) refers to the performance dispersion that arises between otherwise identical strategies differing only in their rebalancing dates. Although often overlooked, RTL can reach substantial magnitudes in high-turnover strategies, and compounding effects may amplify its long-term impact. Portfolio tranching is a well-established method to mitigate RTL exposure, yet its real benefit is likely to depend on the investor’s assets under management (AUM). In this paper we empirically examine RTL in a U.S. equity momentum portfolio rebalanced monthly. Between 1991 and 2024, the gap in compound annual growth rate (CAGR) between the most and least favorable rebalancing schedules reached almost 350 basis points. We then develop a framework to determine the optimal degree of tranching under realistic assumptions about transaction costs. Results show that while tranching consistently reduces RTL, its net advantage is primarily confined to highly capitalized investors or those involved in the design of factor-based investment vehicles, whereas for smaller investors the additional trading costs often outweigh the benefits. Retail investors must therefore accept being exposed to RTL risk as an inherent and largely unavoidable aspect of rotation-based investing.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“In the context of constructing and managing investment portfolios, the term rebalance timing luck (RTL) describes the “potential performance dispersion between two identically managed strategies with different rebalance schedules” (Hoffstein et al., 2020).

Although the rebalancing policy of an investment strategy may seem superficial or inconsequential at first glance, research beginning with Blitz et al. (2010) has shown otherwise. Several academics have since quantified the impact of rebalance timing luck in factor portfolios (also known as smart beta portfolios), concluding that its effects are material and cannot be overlooked.

For instance, Hoffstein et al. (2020) build long-only indices that replicate exposure to well-known U.S. equity factors (size, value, momentum, low volatility and quality) and change their rebalance calendars to measure rebalance timing luck. They find that RTL effects are meaningful, frequently surpassing 100 basis points annualized, and highly sensitive to the “frequency of rebalancing, portfolio concentration, and the nature of the underlying strategy”. Their results indicate that RTL is effectively an “uncompensated source of risk”, complicating evaluation of strategies, peer groups, and their benchmarking.

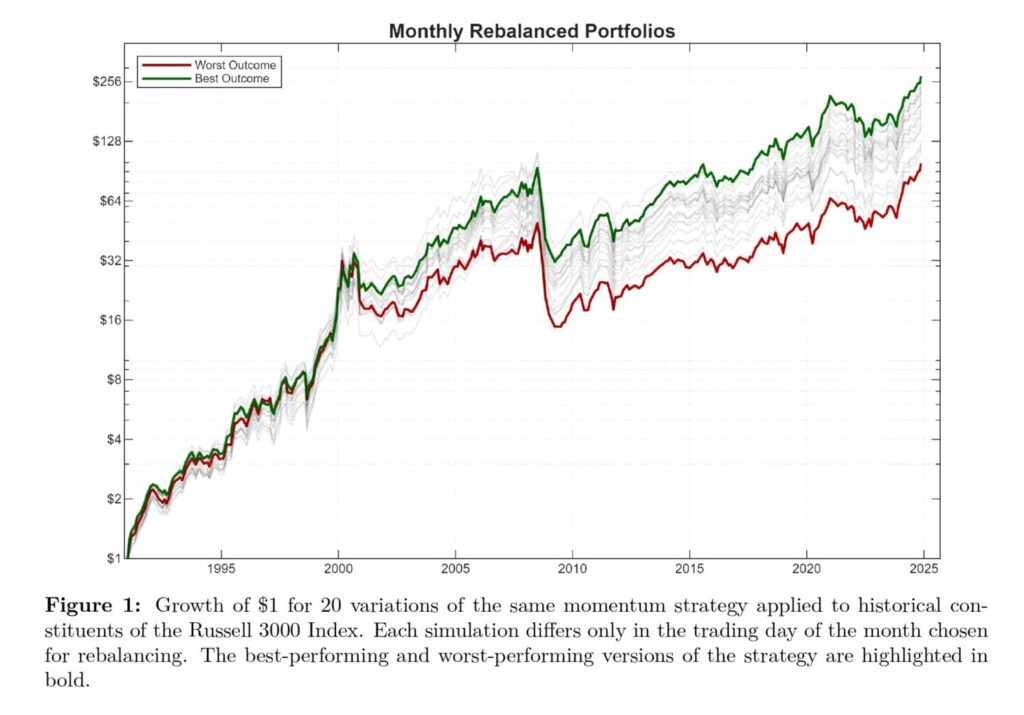

Our tests reveal a pronounced effect of rebalance timing luck (RTL), with the difference in CAGR between the most and least favorable rebalancing dates amounting to 348 basis points. Given that this dispersion effectively compounds over time, we can see how in the least favorable run an initial investment of $1 grows to $99, whereas in the most favorable run it grows to $272, a difference of almost threefold.

This illustrates how a seemingly innocent decision (the choice of rebalancing date in a rotational stock selection strategy) can result in massive divergences in realized wealth over extended time horizons.

All simulations exhibit positive alphas, with only two reaching marginal significance at the 5% level.5 Trading activity remains elevated, with annual turnover around 1,060% and roughly 340 executed trades per year. Since no rebalancing threshold is imposed to restrict minor position adjustments, this figure also includes micro-rebalancing trades that, in a real-world setting, a portfolio manager might decide to skip. In this study, we deliberately omit such a constraint to ensure that rebalance timing luck (RTL) is not affected by anything beyond the variation in rebalancing days.

Figure 2 illustrates how rebalance timing luck (RTL) and the number of trades scale with the number of tranches. An interesting observation is that our results seem to confirm the findings of Hoffstein et al. (2019), who conclude that tranching reduces RTL by a factor of 1/N .

Building upon the existing literature, this study confirms that rebalance timing luck can be a highly impactful source of performance dispersion, with meaningful implications for realized wealth over time. In the context of the concentrated momentum strategy analyzed in our tests, the effects of rebalance timing luck (RTL) can be documented at intra-month resolution, with dispersion reaching almost 350 basis points in compound annual growth rate (CAGR).”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend