Phenomenal innovation, new technologies, growth of social media, and e-commerce have been characteristics of the last decades. BigTech companies such as Google, Facebook (Meta), Amazon, Apple, and Microsoft are becoming so increasingly popular. So now, in connection to the actual carnage on the financial markets, the question arises: are BigTech firms the new “Too Big to Fail”?

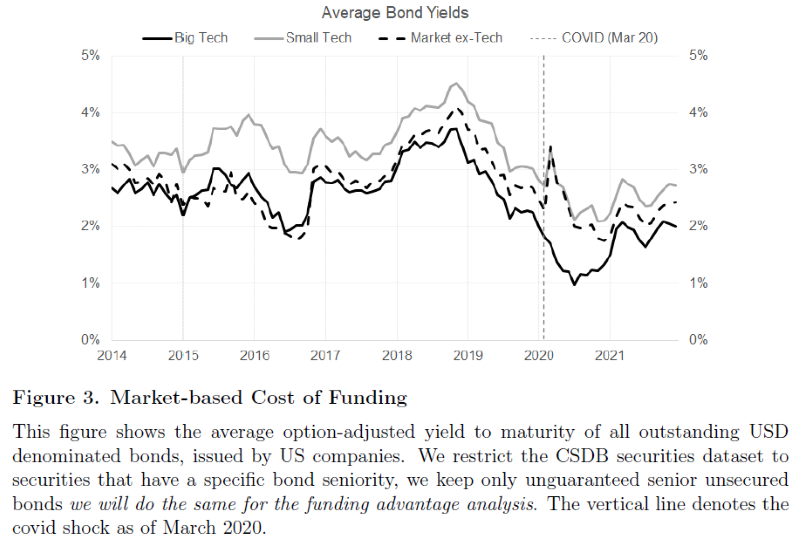

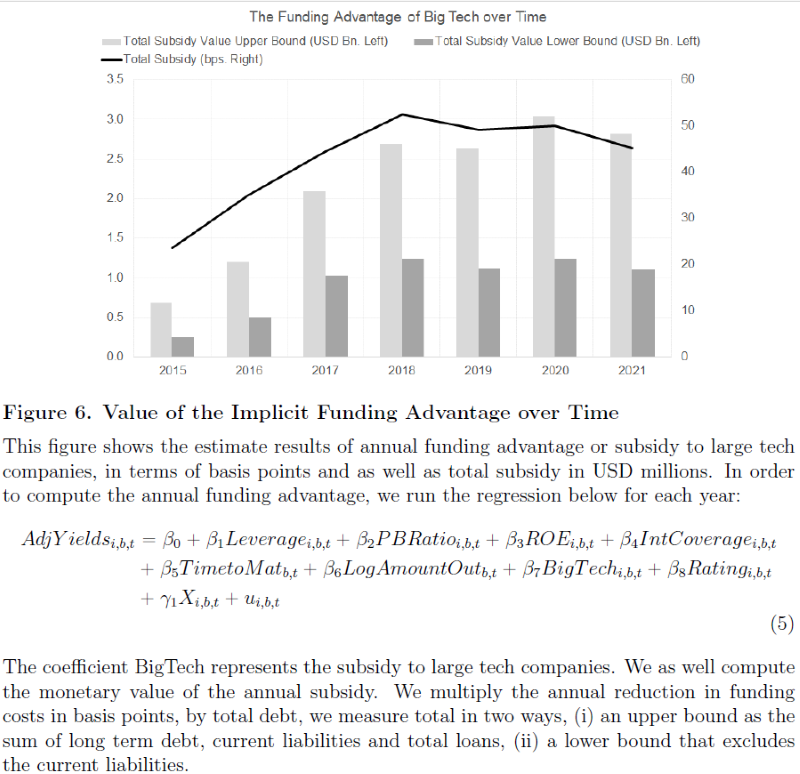

The authors of a recent academic paper answered this question from two perspectives – macro and finance. Firstly, they examined that, from 2014 to 2021, the largest tech companies benefited from a funding advantage of about 30bps., on average. Investors expect that the government will support these firms and consequently do not correctly price risk. Secondly, the paper shows that investors prefer BigTech investments during turbulent times, as we could observe throughout the Covid-19 crisis. In other words, investors see BigTech bonds as safe assets.

Finally, the authors confirm that BigTech companies are predisposed to be the new “Too Big to Fail” firms because of their unique position. However, the question remains on how to regulate these companies in the future.

Authors: Nordine Abidi and Ixart Miquel-Flores

Title: Too Tech to Fail?

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4149787

Abstract: Do the biggest tech companies have a bond funding edge? Are they the new “Too-Big-to-Fail” (TBTF)? TBTF represents, among other things, the idea that the biggest firms (usually banks) receive an unfair funding advantage over smaller ones in the bond market. By investigating the tech financial world, our empirical work reveals two important findings. First, within the universe of bond-issuing U.S. firms, the largest tech companies did experience a funding advantage – of about 30bps. on average – from 2014 to 2021. Our estimates suggest that the (implicit) subsidy is in the range of 1 to 2 USD billion per year and that this has been steadily rising over the last years, especially during the Covid-19 period. Second, using a unique dataset of security-level portfolio holdings by sector in each euro area country, we investigate portfolio choices during times of financial distress. We find evidence of a sharp relative increase in portfolio holdings of Big Tech securities during times of market turbulence suggesting that Big Tech bonds act as safe assets. Overall, while the magnitudes of our estimates remain small from a macroeconomic perspective, we find that Big Tech companies are slowly converging towards what we call the “Too-Tech-to-Fail” (TTTF) paradigm. In other words, the unique position they have in the new economy, seems to artificially boost their credit profiles and lower their bond funding costs, potentially creating an uneven playing field.

As always we present several interesting figures:

Notable quotations from the academic research paper:

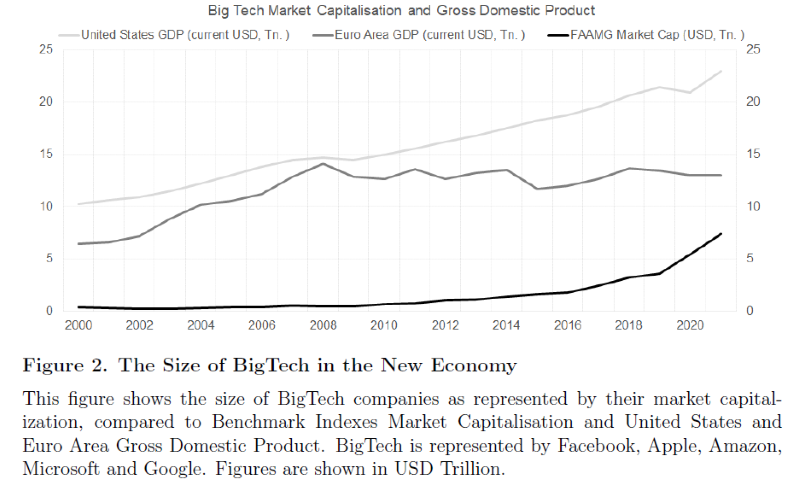

„Over the past two decades, technological change has brought about a sociocultural evolution and revolution in terms of who controls information and knowledge. Today, the biggest five tech companies in the US make up to about a quarter of the value of the S&P 500 by market capitalization. Google and Facebook receive 90% of the world’s news ad-spending, Amazon controls half of all e-commerce in the US, and BigTech operating systems run 99% of cell phones globally (Foroohar, 2021). The Covid-19 crisis has expedited global reliance on these companies.

Although ”too big to fail” (TBTF) has been a long-standing policy issue, it was highlighted by the global financial crisis, when governments around the world intervened to prevent the near-collapse of several large financial firms in 2008 and 2009. Financial firms were said to be TBTF because policymakers judged that their failure would cause unacceptable disruptions to the overall economic system. Since then, researchers have mainly defined TBTF financial institutions based on their size, complexity or interconnectedness (Gorton and Tallman, 2016, Cetorelli and Traina, 2018).

In addition to equity considerations, economic theory suggests that expectations that a firm will not be allowed to fail create moral hazard—if the creditors and counterparties of a TBTF firm believe that the government will protect them from losses, they have less incentive to monitor the firm riskiness because they are shielded from the negative consequences of those risks (Mishkin, 2007). On the one hand, TBTF firms could have a funding advantage compared with other companies, which some call an implicit subsidy (Li et al., 2013; Ueda et al., 2013; Beyhaghi et al., 2014; Acharya et al, 2016). On the other hand, some researchers and market participants have found weak evidence that large financial institutions are the beneficiaries of implicit TBTF government policies and became riskier as a result (Beck et al., 2006; Goldman Sachs, 2013). Nevertheless, TBTF remains controversial.

Our analysis has two readings, a macro and a finance one: the macro view concerns BigTech corporates and the estimation of the ”Too-Tech-to-Fail” (TTTF) implicit subsidy, while the finance view focuses on risks and decisions of portfolio investors.

On the macro side, the paper suggests that largest tech companies experience a funding advantage – of about 30bps. on average – from 2014 to 2021. Our estimates suggest that the (implicit) subsidy amounts to around 2 USD billion per year and has been steadily increasing for most of the observed time covered, especially in the wake of the COVID-19 pandemic. Although the magnitudes of the estimates remain contained, we find that expectations of government support seem to be embedded in the option-adjusted yields of bonds issued by large US tech institutions. In other words, we find that bondholders of BigTech institutions appear to have an expectation that the government will (possibly) shield them from losses in the event of a ”tech failure” and, as a result, they do not accurately price risk. This expectation of government support constitutes an implicit discount of large tech institutions, allowing them to borrow at subsidized rates.

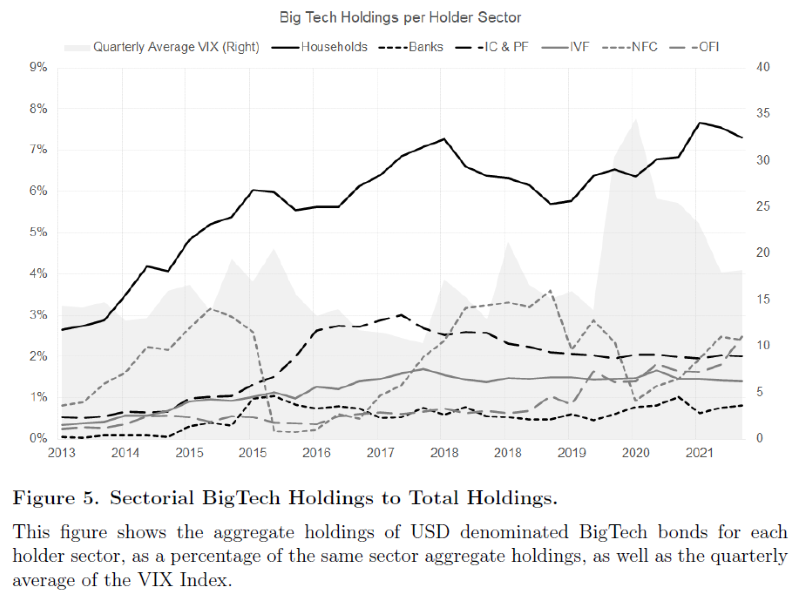

On the finance side, our analysis teaches us about what investors do when they are confronted to global uncertainty. The paper shows that, they prioritize BigTech investments over other investments in turbulent times. We provide strong evidence that investors tend to increase their large tech exposures at times of financial stress. We prove that the identified change in tech holdings does not reflect price fluctuations of individual securities, but real investments in this group of firms.

All in all, our paper suggests that BigTech companies are likely to be the new TBTF firms – BigTechs are converging slowly towards what we call the ”Too-Tech-to-Fail” paradigm. In other words, the unique position of these companies in the new economy seem to artificially boost their credit profiles and lower their bond funding costs, possibly creating an uneven playing field. Future research must assess whether the current Bigtech’ regulations that seek to address ”the too-big” problem would have a significant impact in eliminating expectations of government support.“

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend